The effectiveness of the alignment through fund investments

The UN Sustainable Development Goals (SDGs) require financing of $ 5-7 trillion annually in order to be met by 2030 (UNCTAD, 2014). This can be seen as both a need and an investment opportunity. The opportunity is the result of transforming a challenge into an investable solution. Many of these solutions still need to be created, especially in emerging markets which by some estimations still require 96% of global financing needs to achieve the UN SDG’s (UNEP Finance Initiative, 2018). A good example of the need and opportunity from the past is the contribution of microfinance solutions to reach the Millennium Development Goals. Similarly, financing the SDGs requires collaboration between private capital and public capital, as public funding alone is not enough to reach the goals. For the private capital to meet its ‘part of the bargain’, global sustainability challenges need to be presented as financially attractive solutions to institutional investors, the biggest capital providers. Emerging markets face additional hurdles as capital markets and investment industry are less developed.

Many institutional investors are busy with creating frameworks which would allow them to recognize financially attractive investment opportunities that also contribute to the SDGs. One such framework is becoming an industry standard and is described in more detail in the first two parts of the article.

Many institutional investors are busy with creating frameworks which would allow them to recognize financially attractive investment opportunities that also contribute to the SDGs. One such framework is becoming an industry standard and is described in more detail in the first two parts of the article.

However, a more active approach than a mere framework development is needed if investments are expected to deliver joint financial and social and environmental returns by 2030. The remainder of the article therefore outlines how institutional asset owners can speed up the process of sustainable development in emerging markets by investing in investment funds specifically targeting one or more social and/or environmental topics and market-rate financial returns.

Creating a common understanding

Since the UN Sustainable Development Goals were introduced in 2015, many institutional asset owners have pledged their commitment to them.2 However, these commitments have so far not been translated into tangible investments on a large scale. Instead, asset owners have embarked on a long journey of mapping their contribution to the SDGs within their current portfolios. This has resulted in a growing number of different methodologies to report and explain different ways institutional asset owners support the SDGs.

APG and PGGM provide a clear guidance on investments into SDGs

One such methodology is taxonomies, or “classifications of solutions for each SDG” (PGGM, 2017), introduced by Dutch pension fund fiduciary managers APG and PGGM. This methodology is by far the most cited methodology on how asset owners can contribute to the SDGs, and it has been used by many initiatives since its conception.3 While recognizing these are far from perfect, with taxonomies, APG and PGGM provide clear guidance on which investments count as Sustainable Development Investments (SDIs), i.e. investments that “meet investors financial risk and return requirements and support the generation of positive social and environmental impact through their products and services, or at times through acknowledged transformational leadership” (PGGM, APG, 2017). In practice, they connect the SDG targets4 to the current investment solutions they come across on a daily basis. For example, in SDG #12 (Responsible Consumption and Production), identified potential areas of investment include “Packaging for spoilage prevention, recycling of food waste” and “Biochemicals”. Therefore, a company with the majority of its revenues coming from recycling of food waste or with an industry unique recycling of food waste business line (making it a transformational leader) would qualify as an SDI as long as it meets investors financial risk and return requirements.

These taxonomies have also been endorsed by four main Swedish buffer funds, alongside Australia’s Construction and Building Unions Superannuation fund. However, they present only one of the approaches taken by the investment industry to describe its contribution to the SDGs. Other approaches, including those developed by DWS (DWS, 2018) or TruValue Labs (TruValue Labs, 2017), use different methodologies, making it more difficult to pile individualistic approaches together and compare them. Most approaches do not have a clear pathway from investment activities to SDG indicators, which is most likely one of the reasons why taxonomies are endorsed by so many investors. Clearly, a big push by international organizations such as the UN or European Commission is still needed to align the SDG investment practices of a diverse set of investment market participants.

Current alignment of investments towards the SDGs

Next to mapping how the portfolio is currently aligning to the SDGs, it is important to establish ways investors can increase investments in SDGs. And, equally important, how these can be channelled to the most deprived areas.

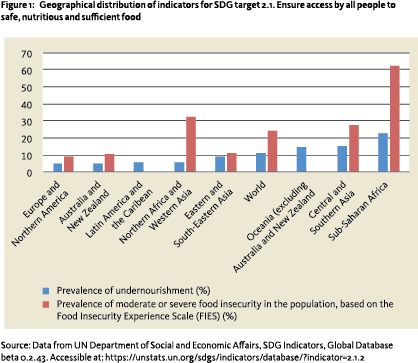

For example, APG and PGGM have recognized SDG target 2.1: Ensure access by all to safe, nutritious and sufficient food all year round as an investable SDG target. This target can be addressed by businesses providing access to fresh food (e.g. Sprouts Farmer Market), food packaging (e.g. SIG Combibloc) and food testing businesses (e.g. Intertek) or businesses producing basic food, healthy food ingredients and healthy and natural food sustainably (e.g. Hain Celestial). In either case, the most effective way to reach this target from the global perspective would be to invest in those areas where access to safe, nutritious and sufficient food all year round is the most limited.

Inter-Agency and Expert Group on SDG Indicators developed a global indicator framework to track progress on the SDGs (UN Statistics Division, 2018). Indicators to track progress on target 2.1 are prevalence of undernourishment & prevalence of moderate or severe food insecurity in the population. Their geographical breakdown reveals that investments would need to take place in geographies traditionally labelled as emerging and frontier markets by the investment community in order to reach target 2.1 most effectively5 (see Figure 1).

Targeted investor contribution to the SDGs

The analysis of PGGM’s Investment in Solutions (BiO)6 portfolio (PGGM, 2018) reveals that portfolio investees do not directly, i.e. through their products and services, address the most deprived areas (as indicated by Figure 1). This fact, however, does not mean that investors are not putting in their best effort to address a specific SDG. However, after defining the investable universe that fits investment requirements, will the investor select those companies that impact social and environmental development the most? Or, are there ways through which the investor can ensure that their investments have a more targeted contribution to the SDGs?

To answer these questions the portfolios of 3 investment funds that manage capital from institutional asset owners are analysed. By comparing portfolio characteristics with the broader progress on SDGs within a fund’s target market, it is possible to study if a fund contributes to sustainable development most effectively. In the analysis the focus has been put on positive solutions rather than risk mitigating solutions. Positive solutions are supported by thematic impact investment funds which invest in opportunities focusing on specific impact themes. Phenix Capital’s proprietary database consists of 600+ such funds across all asset classes, that focus on at least one impact theme/SDG, target market rate returns, and manage at least $100 million in assets.

SDG investment effectiveness = highest possible impact for expected risk/return

Recurring impact themes that institutional asset owners search for are: access to finance, education, renewable energy and energy efficiency. In the language of the SDGs these translate to: SDG 1 (No poverty), SDG 10 (Reduced Inequalities), SDG 4 (Quality Education) and SDG 7 (Affordable and Clean Energy). In each of these impact themes/SDGs, the portfolio of one investment fund per theme will be analysed against broader development in SDG indicators in the fund’s target market. All three funds7 have been cherry-picked from the database because they:

Recurring impact themes that institutional asset owners search for are: access to finance, education, renewable energy and energy efficiency. In the language of the SDGs these translate to: SDG 1 (No poverty), SDG 10 (Reduced Inequalities), SDG 4 (Quality Education) and SDG 7 (Affordable and Clean Energy). In each of these impact themes/SDGs, the portfolio of one investment fund per theme will be analysed against broader development in SDG indicators in the fund’s target market. All three funds7 have been cherry-picked from the database because they:

- Consistently report on impact they are achieving

- Manage capital on behalf of institutional asset owners (pension funds and/or insurance companies)

- Target market-rate financial returns

- Focus their investments on themes directly related to the SDGs

- Focus their investments on emerging markets

Moreover, all three funds are private market funds. Two of them, the one focusing on microfinance and the one focusing on renewable energy and energy efficiency, invest in debt instruments. The third, focusing on education, makes equity investments in early growth and growth stage companies. The rest of fund characteristics such as costs and liquidity, are comparable to market standards for their specific asset classes and fund sizes.

Portfolio characteristics that have been analysed against broader development in SDG indicators are country weight portfolio allocation (in %) for funds investing in access to finance and education and growth in assets under management (AuM) (in %) for a fund investing in renewable energy and energy efficiency. Country weight portfolio allocation can indicate whether a fund targets most deprived areas, while comparing growth in AuM to broader development in SDG indicators can indicate whether fund’s investments translate into sustainable development in the fund’s target market.

The SDGs present a convenient framework for comparisons because they enable assessment of a fund’s contribution to financing the most deprived regions and whether the fund’s existence leads to improvements according to the SDG indicators. However, it should be noted that the mere presence of a fund in a certain market does not mean that the SDG indicators should improve. The SDG indicators are assessing progress on a much broader area than a single fund could address alone.

Moreover, these areas are not only influenced by the fund’s activity but also by political, cultural and economic factors as well. As the analysis is based solely on simple correlations and comparisons, there should be no causal relationship inferred from it. Nevertheless, it is worthwhile to compare business activity and private investment flows with social and environmental conditions in a certain market.

Access to finance

Access to finance in emerging and developing markets entails deployment of micro loans and other microfinance activities such as micro insurance and micro savings to poor communities (Karlan & Morduch, 2009). Taking out a loan in order to buy a sewing machine to start a sewing business is just one example how improved access to finance can bring people out of poverty. Having access to a saving account to smooth consumption and guard yourself against risky situations, such as floods or hurricanes is another one (Armendáriz de Aghion & Morduch, 2009). The same literature portrays a theory in which incomes of the poor should experience much faster growth because it is expected that a much lower baseline level of income ensures higher returns to capital.

Access to finance in emerging and developing markets entails deployment of micro loans and other microfinance activities such as micro insurance and micro savings to poor communities (Karlan & Morduch, 2009). Taking out a loan in order to buy a sewing machine to start a sewing business is just one example how improved access to finance can bring people out of poverty. Having access to a saving account to smooth consumption and guard yourself against risky situations, such as floods or hurricanes is another one (Armendáriz de Aghion & Morduch, 2009). The same literature portrays a theory in which incomes of the poor should experience much faster growth because it is expected that a much lower baseline level of income ensures higher returns to capital.

Investments into SDGs are not a silver bullet for sustainable development

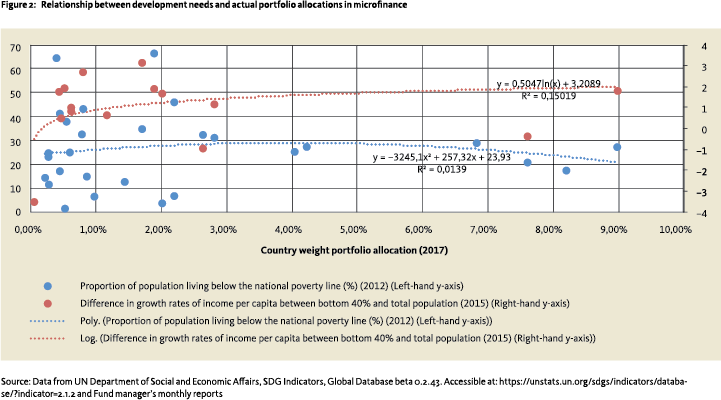

There are currently 113 microfinance investment vehicles (MIV), with the estimated total size of private and public investments in 2015 at $ 15.1 billion (Symbiotics, CGAP, 2016) that provide one or more services improving access to finance (micro loans, micro insurance, micro savings).9 The following analysis therefore focuses on an MIV that is in both Phenix Capital’s database and Symbiotics, CGAP survey of MIVs and shows how related investments into microfinance institutions are to eradicating poverty and reducing inequality.

Microfinance portfolios are usually diversified across many emerging and developing markets. In order to manage such diversified portfolios, portfolio managers need to possess expertise across all these markets. Investment decisions should, therefore, not be guided by familiarity and individual sympathy for the markets, but by the attractiveness of the investment opportunity itself. The question is whether opportunities, as indicated by the geographical breakdown of a portfolio, match the needs, as indicated by the deprivation level of countries.

A portfolio snapshot of a fund investing in microfinance institutions from 2017 reveals that investment opportunities do not match the SDG needs.10 SDG Indicator 1.2.1 Proportion of population living below the national poverty line (%) and SDG Indicator 10.1.1 Difference in growth rates of household expenditure or income per capita among the bottom 40 per cent of the population and the total population do not show any statistically significant relationship with the geographical breakdown of one of the biggest microfinance funds in the world (Figure 2).

The analysis implies that current opportunities with a market rate return might not be available in the most deprived areas. The portfolio therefore tilts towards more profitable but less deprived areas. On the other hand, it might be that profitable opportunities in the most deprived areas are not on the radar of the manager or that the manager is not optimizing for delivering the highest possible impact within its investment universe. However, the benefit of microfinance funds attracting private capital is that they relieve pressure on public funds from unnecessary funding of profitable investment opportunities, as microfinance institutions switch from public and donor-based financing to private financing.

Education

Education has been recognized as one of the most popular impact themes among institutional asset owners reaching out to inquire about impact investments. However, there are only 4 thematic impact investment funds in the researched universe that focus only on education services and whose goal is to deliver market-rate returns. Two of them target emerging markets exclusively. A study of the one that satisfied all five points raised above makes an analysis whether the fund targets the areas where education is needed the most.

Education has been recognized as one of the most popular impact themes among institutional asset owners reaching out to inquire about impact investments. However, there are only 4 thematic impact investment funds in the researched universe that focus only on education services and whose goal is to deliver market-rate returns. Two of them target emerging markets exclusively. A study of the one that satisfied all five points raised above makes an analysis whether the fund targets the areas where education is needed the most.

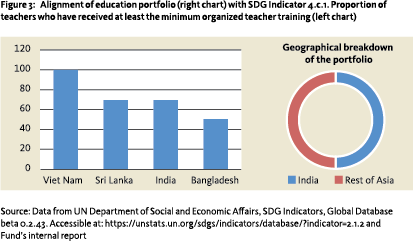

The researched private equity manager focusing on investing in education services in emerging markets, specifically in South and South-East Asia, claims that the fund contributes to the SDG 4. However, there is only a slight match between the fund’s impact indicators and SDG 4 indicators. The rationale behind it is that SDG 4 indicators relate to the bottom of the pyramid (BoP) population, i.e. the most deprived, whereas the fund targets lower-middle and middle income market.

Funds should optimize for SDGs within their target geographies

Nevertheless, the comparison of the geographical breakdown of the portfolio and SDG 4.c.1 indicator (Proportion of teachers who have received at least the minimum organized teacher training) needs reveals that investments are geographically relatively better placed within fund’s target market compared to the microfinance fund discussed earlier. For example, the fact that most of the portfolio is invested in India when specifically India faces a shortage of qualified teachers11 suggests that the fund invests, at least partially, in opportunities where financing of education is needed most. Within its target market, the fund seems to be focusing its impact on SDG 4.c.1. Nevertheless, South and South-East Asia show much stronger performance on SDG 4 indicators than most other areas (UN Statistics Division, 2018) and the fund’s portfolio would therefore not optimize for SDG 4 indicators on a global scale.

This case is a strong example of how focusing on impact should be done on the target market level. In other words, managers can add value only in the areas their expertise lies, therewith generating better contribution to the SDGs. The case also shows that there is still a large need for additional investment funds in education as the current universe comprises of only 4 funds specialized on education.

Renewable energy and energy efficiency

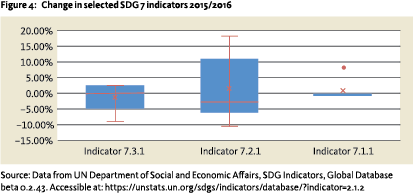

Currently, our data sets includes 32 impact investment funds across asset classes that focus solely on investments contributing to the SDG 7 Affordable and Clean Energy (this doesn’t include funds focusing on investments in other SDGs next to the SDG 7). The focus of the analysis has been put on one of the largest funds among them. It focuses solely on emerging markets and, to the knowledge of Phenix Capital, manages institutional asset owners’ capital. The fund provides energy finance (via financial institutions) and invests directly in renewable energy companies in South-East Europe, Eastern Europe, Central Asia, Middle East and Northern Africa. This fund’s contribution to the SDGs is measured by comparing its asset size progression with the improvement in the SDG 7 indicators in the fund’s target market. Indicators 7.2.1 Renewable energy share in the total final energy consumption and 7.3.1. Energy intensity measured in terms of primary energy and GDP are directly related to fund’s sector focus. Investments in renewable energy projects are expected to increase the amount of renewable energy available for consumption. On the other hand, “Energy efficiency simply means using less energy to perform the same task” (Environmental and Energy Study Institute, 2018) and can be measured by the energy intensity, i.e. the amount of energy needed to create one unit of output. Energy efficiency investments are therefore expected to decrease the energy intensity level.

Between 2014 and 2017, the fund’s assets under management (AuM) grew 22%, 18% and 9% yearon-year, respectively. SDG indicator data availability permitted the analysis on changes happening between 2015 and 2016 only. Thus, the referencing change in AuM is 18%. The graph below indicates that changes in different SDG 7 indicators in the fund’s target market are very spread out over the range between –5% and +15%. However, changes in every indicator are in the expected direction. The change in the Indicator 7.1.1. Proportion of population with access to electricity is negligible as markets in which the fund invests have relatively high proportion of population with access to electricity.

Between 2014 and 2017, the fund’s assets under management (AuM) grew 22%, 18% and 9% yearon-year, respectively. SDG indicator data availability permitted the analysis on changes happening between 2015 and 2016 only. Thus, the referencing change in AuM is 18%. The graph below indicates that changes in different SDG 7 indicators in the fund’s target market are very spread out over the range between –5% and +15%. However, changes in every indicator are in the expected direction. The change in the Indicator 7.1.1. Proportion of population with access to electricity is negligible as markets in which the fund invests have relatively high proportion of population with access to electricity.

The results suggest that areas in which the fund invests still show positive movements towards reaching the SDG 7. It still remains to be analysed whether these positive movements arise from fund’s investment activity, or can be accounted for by a general trend or a broader political and cultural movement. It would also be informative to explore the relationship between the fund’s asset size progression and Renewable Electricity Output (% of total electricity output) which is directly related to the SDG target 7.2 (By 2030, increase substantially the share of renewable energy in the global energy mix). This target directly relates to fund’s main investment activity but the lack of data constrained the further research.

Long road ahead

The investment industry is starting to adopt a common understanding of how it can align investments to globally accepted SDGs. PGGM’s and APG’s taxonomies have been pivotal in the creation of this common understanding. However, it is still not clear how the mainstream investment industry can funnel capital towards emerging markets, i.e. areas where capital is needed the most.

Current institutional asset owner portfolios will not yet be sufficiently aligned with the SDGs as long as investees do not clearly articulate how their products and services are addressing areas where challenges are most severe. Dedicated impact funds that have been analysed in this article do not show perfect alignment of their investments to the SDGs neither. Within their investable universe, they do not or they partially optimize for areas with most SDG needs, as indicated by the SDG indicators. Nonetheless, a thematic approach enables an investor to clearly identify and communicate what type of impact its investment is achieving. It makes a comparison between portfolio companies’ impact and SDG indicators more straightforward. This holds funds more accountable for the impact their investees are creating. However, it also requires specific expertise which asset owners can gain by building teams themselves or by employing external fund managers.

The analysis suggests that impact investment funds can be at least partially credited for improvements in SDG indicators in emerging markets they invest in. As a result, asset owners can increasingly rely on these funds to align their investments with the SDGs, maximize their impact on the realization of the UN SDG’s and achieve competitive financial returns in the same time.

References

- Armendáriz de Aghion, B., & Morduch, J., 2009, The Economics of Microfinance. Cambridge, MA: The MIT Press.

- DWS, 2018, Integrating the UN Sustainable Development Goals into Investment Portfolios. DWS Global Research Institute.

- Environmental and Energy Study Institute, 2018, July 26, Energy Efficiency: EESI. Retrieved from Environmental and Energy Study Institute: http://www.eesi.org/topics/ energy-efficiency/description.

- Karlan, D., & Morduch, J., 2009, Access to Finance. In D. Rodrik, & M. Rosenzweig, Handbook of Development Economics (pp. 4703-4777). Amsterdam: North Holand.

- PGGM, 2017, Annual Responsible Investment Report 2017.

- PGGM, 2018, Overview Investments in Solutions – Food Security. Retrieved from https://www.pggm.nl/english/what-we-do/ Documents/BiO-Food_2017.pdf.

- PGGM, 2018, July 24, What We Do – Criteria: PGGM. Retrieved from PGGM Website: https://www.pggm.nl/english/what-we-do/ Pages/BiO_Criteria.aspx.

- PGGM, APG, 2017, July 07, APG: Sustainable Development Investments. Retrieved from APG Web Site: https://www.apg.nl/en/ publication/SDI%20Taxonomies/918.

- Symbiotics, CGAP, 2016, Microfinance Funds: 10 Years of Research and Practice.

- TruValue Labs, 2017, Investing with the Sustainable Development Goals.

- UN Statistics Division, 2018, July 30, SDG Indicators Global Database: UNSD. Retrieved from UNSD website: https://unstats.un.org/ sdgs/indicators/database/.

- UNCTAD, 2014, World Investment Report 2014: Investing in the SDGs: An Action Plan. New York and Geneva.

- UNEP Finance Initiative, 2018, Rethinking impact to finance the SDGs. Retrieved from http://www.unepfi.org/positive-impact/ rethinking-impact/.

Notes

- Bruno Besek is Associate, Phenix Capital

- Rust, S., 2016, Major European pension investors commit to UN development goals. Article on https://www.ipe.com/news/ esg/major-european-pension-investorscommit-to-un-development-goals/10015051. fullarticle Baker S., 2018, 6 Danish pension funds commit to fund focused on UN Sustainable Development Goals. Article on http:// www.pionline.com/article/20180607/ ONLINE/180609902/6-danish-pensionfunds-commit-to-fund-focused-on-unsustainable-development-goals Diamond, R., 2018, CalPERS examines adopting SDGs. Article on https:// www.top1000funds.com/2018/01/ calpers-examines-adopting-sdgs/

- One such initiative is a report SDG Impact Indicators (2017) by 19 Dutch financial institutions that proposed indicators which translate SDG indicators to investors investment activity. With these indicators it is possible to track and compare sustainable development investments.

- Each Sustainable Development Goal consists of multiple targets. The progress on every target can be traced by referring to specific SDG indicators.

- In other words, investments in emerging and frontier markets would have the highest marginal benefit for SDG target 2.1.

- PGGM regards all Investments in Solutions (BiO) as Sustainable Development Investments (SDI). However, the reverse is not true as SDIs include many more sectors, as defined by the SDGs. The criteria for a company to be eligible as an SDI are specified on PGGM’s website: www.pggm.nl

- The data has been acquired on a proprietary basis from all three fund managers. Therefore, the fund names cannot be disclosed.

- Managers bear the cost of impact due diligence and management so there is no increase in cost when controlled for the fund’s respective asset class and fund size. With regards to liquidity, the microfinance fund is different from other two funds. It doesn’t have a lock-up period but instead provides monthly liquidity which is due to the underlying investments (microfinance institutions provide short-term micro loans).

- Not all of these investment vehicles qualify for Phenix Capital’s database as some don’t satisfy the minimum requirements (e.g. minimum size).

- It should be noted that the most comprehensive data for SDG Indicator 1.2.1 dated from 2012, for SDG Indicator 10.1.1 from 2015 and the country allocation of the fund dated from Q2 2017. Analysis was done on 71.91% of the fund’s portfolio for SDG Indicator 1.2.1 and 36.08% of the fund’s portfolio for SDG Indicator 10.1.1 due to lack of data for SDG Indicators.

- One of the sub-topics the fund invests in is the education of teachers.

in VBA Journaal door Bruno Besek