Introduction

A changing geo-political landscape, low interest rates, and changing pension deals challenge investors in navigating their asset base through uncertain financial markets. The question is how unconventional monetary policy of the major central banks around the world unfolds and how financial market dynamics evolve from here, especially when interest rates rise. Also, international trade relationships and the potential impact on economic growth are being discussed after the recent election outcomes in the US and Europe and with the United Kingdom leaving the European Union. On top of that, tensions from terrorism, changing demographics and falling oil prices provide enough reason to think about the unthinkable. This is exactly what a Global Macro investor is doing all the time.

While there is no universally accepted definition for Global Macro investing, the approach has always centered on top-down macroeconomic developments, global imbalances and changing growth opportunities. The strategy dates back to the seventies. It was put further on the map after George Soros successfully positioned against the British Pound in 1992.

While there is no universally accepted definition for Global Macro investing, the approach has always centered on top-down macroeconomic developments, global imbalances and changing growth opportunities. The strategy dates back to the seventies. It was put further on the map after George Soros successfully positioned against the British Pound in 1992.

Although macroeconomics is at the forefront of most investment discussions, there is a large diversity in the translation into investment decisions. Traditionally, strategic asset allocations were complemented by a tactical asset allocation (TAA) program to shift the asset mix towards macro views. Classical TAA programs usually lead to active overor underweights in stocks and bonds or active changes to the strategic currency hedge policy. Over time, the experience learned several limitations of TAA. The breadth was often limited to the asset classes and opportunities cannot always be optimally exploited via cash instruments. Also the decision frequency of tactical decisions was typically low. Furthermore, the new portfolio may not be balanced from a risk perspective. It may load on concentrated risk factor exposures or it may use a disproportionate active risk budget versus the risk usage elsewhere in the asset mix such as the bottom-up security selection.

In our view, Global Macro is the successor of classical TAA in embracing macro views and thinking about the unthinkable. Global Macro employs the same investment universe as TAA programs. However, as we will argue below, the Global Macro space is much broader and more diversified. Not only under- and overweights of the stock and bond allocation are considered, but also relative positions are taken into consideration. Examples include European versus US equities, sector spreads or term structure positions. Such positions are also taken in a portfolio context and in a risk-controlled way. It is the daily job of Global Macro investors to take advantage of macro events. As such they are always thinking about the unthinkable in stress tests and scenario analysis when constructing their overall portfolio.

“Look at market fluctuations as your friend rather than your enemy; profit from folly rather than participate in it”.

Warren Buffett

What all Global Macro strategies have in common is that they cover all asset markets, ranging from equities, fixed income, credits, inflation, currencies, commodities and volatility without having a bias to any of these markets. Global Macro strategies usually have a global coverage and only operate in the most liquid market segments. Typically, the goal is absolute return and the aim is to be net neutral to markets over the longer term. Therefore it has the ability to do well in markets where almost all asset class returns turn negative.

This article explores how insights from Global Macro investing can be translated to a broader investment portfolio when thinking about the unthinkable, and when constructing a portfolio to take advantage of opportunities in a robust and risk-controlled way. We first describe why we think that the opportunity set for diversification has changed in the asset allocation landscape with interest rates so low. Next, we discuss the Global Macro approach and its elements that help to position for unlikely and unthinkable scenarios in building a balanced portfolio. Finally, we summarize the relevant insights of Global Macro hedge funds regarding investment beliefs and portfolio construction when building a robust portfolio towards the unthinkable.

Ever lower yields have increased the risk of the unthinkable

In asset allocation, the main question has always been how to moderate the pro-cyclicality and stress sensitivity of the dominant equity exposure. After all, equities can have serious downside, especially if the “unthinkable” happens. A downturn in equity markets almost always coincides with economic headwinds or geopolitical stress. On top, most assets that are thought to be diversifying under normal market circumstances display positive exposure to equities during the above stress events when diversification is most needed. This tailexposure to stress events also holds true for illiquid assets, like real estate and infrastructure as the illiquidity premium rises quickly when capitulation flows start in earnest.

For a long time bonds have been the perfect match to equities as they generated solid returns while offering protection in difficult times. The risk parity solution of levering safe-haven bonds up to equity-like risk levels fared very well in the shift from the high yields from the early 1980s stagflation to current negative yields. However, at this point in time, expecting further decreases in interest rates makes less sense. Consequently a continuation of the “happy” correlation structure between bonds and equities is less likely. This poses the compelling question to pro-active asset allocators: what will offer protection in the next bear market? In the rebound from the depths of the 2008 global financial market crisis, balanced portfolios have posted positive returns for a long time, thereby decreasing the ex-post need to diversify. Furthermore, investors are prone to extrapolation, herd behavior, peer pressure, short-termism and procyclical risk appetite. As a result, calm and balanced markets can suddenly swing from complacency to capitulation as new information arrives. Despite this constant turbulence, there is today an increasing preference for passive investing, ignoring the opportunities that dynamics in markets offer. However, as valuations of traditional assets get more and more stretched and yields have largely disappeared, the need for alternatives has quietly grown. We argue that dynamic, tactical or Global Macro investing has the potential to diversify, protect and generate positive performance in uncertain times.

A Global Macro Perspective

The spectrum of Global Macro hedge fund managers is heterogeneous when it comes to the investment style and actual returns. Distinctions typically are in the investment process (systematic vs discretionary and top-down vs bottom-up); the asset class focus; the degree of directionality; the degree of concentration and the investment horizon.

Dynamic market opportunities may be captured in different ways, thereby enabling diversification benefits over many layers. One can diversify over various investment horizons and balance shortterm sentiment-driven dynamics with cyclical medium-term trends and long-term valuation dislocations. To bolster the return-to-risk level, the approach may include both concentrated directional discretionary and diversified systematic approaches. Additionally, the investment universe can be expanded by including more liquid asset classes, factors, sectors and curves.

Dynamic market opportunities may be captured in different ways, thereby enabling diversification benefits over many layers. One can diversify over various investment horizons and balance shortterm sentiment-driven dynamics with cyclical medium-term trends and long-term valuation dislocations. To bolster the return-to-risk level, the approach may include both concentrated directional discretionary and diversified systematic approaches. Additionally, the investment universe can be expanded by including more liquid asset classes, factors, sectors and curves.

Global Macro investors can at times be net short markets. Their returns may even be negatively correlated to equity markets. As long as Global Macro investors can be net short, there will be ample diversification potential with respect to a long-only portfolio. Unlike the current threat of disappearing diversification between stocks and bonds, this type of diversification potential will continue to exist for Global Macro strategies. Furthermore, while in traditional portfolio management the focus is often compartmentalized in single asset classes, for a Global Macro investor there are ample cross-asset opportunities which are often neglected by traditional investors.

We argue that all these arguments explain why a properly designed Global Macro mandate may consistently show low structural exposure to equities and bonds. It is by those elements that Global Macro is one of the few liquid engines that can provide a distinct source of return when equities and bonds disappoint. Its ability to go short, dynamics and the broader universe of liquid markets delivers true diversification.

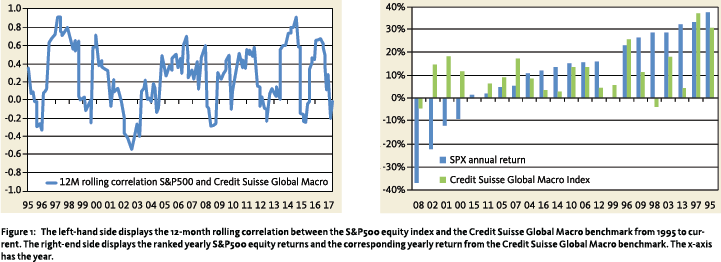

This theoretical claim is supported by the empirical data as displayed in Figure 1 where we compare the returns of the Credit-Suisse Global Macro index, which is one of the most widely used peer group based benchmarks for Global Macro and the S&P500 equity market index. From the left-hand side graph we find that the correlation between Global Macro and Equity markets fluctuates over time and turns even negative during previous down markets in equities (2001-2003 and 2008). On the right-hand side we ranked the yearly equity returns (in blue) and plot the corresponding Global Macro return (in green). It is clear that during 3 out of 4 negative equity years Global Macro as a group delivered positive returns and in the fourth event (2008) Global Macro as a group rendered a very modest negative return whereas the S&P500 had a horrible yearly return (–37%).

How can lessons from Global Macro investing help building a robust portfolio?

First, Global Macro investors profit from long-term mean-reversion and regime shifts. Theory suggests that markets are efficient, but history shows that market equilibria can shift from one extreme to another. Behavioral biases give rise to market momentum, drift and dislocations in value. Dislocations in valuations also arise from imbalances between market participants that have structural flows or investment mandates with diverging goals. Examples include strategic hedging programs, monthly rebalancing flows, structured products, and the rapidly growing interest in risk premia strategies.

As new information comes in, different market interpretations and views arise. For example, the surprise election of President Trump had at first a noisy reaction, next an anticipation of strong reflation potential and a shift in sector preferences. Within the first hundred days most of this got priced out, leaving analysts in the dark about the longer-term implications of the new US administration.

In the short-term, noise dominates the signal but from a longer-term perspective one may conclude that such events lead to extreme outcomes versus historic norms. As an example, following the Brexit vote, the British pound dropped strongly against most other currencies, thereby shielding the UK from an adverse shock to the economy and lower equity prices. However, as in the long term currencies represent a zero-sum game, trading partners will only accept a weak pound for a limited period of time. Based on a variety of fair-value analysis one may suggest a long-term mean to which sterling will eventually revert to. It is typically in these times of stress that assets quickly revert to their fair value. We have witnessed these rapid moves in 2008 with for example credit spreads or the Japanese Yen. Such positions can be defensive in nature to the rest of the asset mix. A contrarian mindset will help creating a portfolio that is robust to extreme events.

Second, timing is less of an essence if forward prices are significantly dislocated. However, as implied by Keynes famous remark that “markets can remain irrational longer than you can remain solvent”, a single event like the Brexit can potentially evolve into a long-lasting regime shift which ultimately forces one to capitulate and take a painful loss. This is why it is so important to not only build reliable valuation models with enough awareness of a potential regime shift, but also warehouse these in a broadly diversified portfolio. Over different cycles and asset classes, dislocations arise and proper portfolio and trade construction in combination with multi-layered risk management can create staying power for single positions. In addition, the return to normalcy for these long-term valuation-based themes may occur at different points in time. This creates various “vintage years” in the long-term portfolio. We believe that dislocations exist and can be used to generate contrarian returns. Exactly those aspects make market timing less dominant than in a classical TAA approach at the overall portfolio. TAA considerably restricts the opportunity set for market timing, while Global Macro exploits the breadth and diversification in various dimensions.

Third, Global Macro investors benefit from sentiment, cycle, shocks and policies. Typically towards the peak of a bull market, like for instance in 1999, exuberant investors like to proclaim the death of the business cycle. However, time and time again markets prove to be prone to cyclical behavior. The higher the recent market returns, the lower the risk aversion will be. Vice versa, the sharper the recent sell-off, the more reluctant people will be to take risk. Risk aversion is pro-cyclical and risk management in general fuels markets cyclicality. Risk aversion causes investors to buy high and sell low even though they are supposed to do the opposite. For a Global Macro investor these dynamics offer opportunities that represent value-added to a passive portfolio.

Again, such opportunities should be warehoused in a diversified risk-controlled portfolio as consistent market timing of a single asset or factor is a challenge. Market themes and conditions rotate and new trends tend to last. By constructing a broad portfolio of tactical opportunities that builds upon market correlations and offsets, a strategy can be constructed that can sustain temporary adverse events. For instance by labelling trades as either risk-on or risk-off, a balanced portfolio can be build that is robust for a turbulent risk-on risk-off environment. Contrarian rebalancing can further add returns to this. For a long time the negative correlation between bonds and equities consistently provided this balance, but ultra-low safe haven yields and the start of the recent monetary policy normalization is changing this correlation regime. Fundamental analysis of return drivers, market intelligence and the translation of opportunities to a robust portfolio are important ingredients to respond to changes in sentiment, fundamentals and policies.

Fourth, apart from restrictions of market neutrality, liquidity, regulation and risk, Global Macro investing has relatively few investment restrictions. This implies that macro themes can be constructed both long and short in a global context across all liquid assets. The portfolio construction also centers around risk allocation to macro themes and macro risks rather than capital allocation. A 10% underweight in equities is very different than a 10% underweight in bonds when measured in risk units, as equities are much more volatile than bonds.

Fifth, Macro dynamics are a rich source of returns that can be extracted both discretionary and systematically. Discretionary traders will typically focus on a limited universe of opportunities, but a quantitative or systematic approach can apply insights to a much broader universe. Cycles and changing fundamentals create return momentum, dislocations and other phenomena across global markets. Systematic techniques are able to monetize this in an efficient way. These systems are not just applicable to the major markets, but also to the wide universe of tradable instruments, cross-asset relations and curves. Rule-based dynamic exposure to market direction and asset rotation is another area that is able to generate diversifying returns.

Conclusion

What to do if anything happens that is currently “unthinkable”? The answer starts with awareness of the situation and knowledge about the sensitivity of your static strategic asset mix to different scenarios or regime shifts. This is basically what Global Macro investors have always been doing in their macro stress-test analyses. We think that by being active in Global Macro or GTAA strategies, one can better understand the dynamics of changing investment environments and the implication for future expected returns which are elements of such a macro stress test.

There are many ways to use insights from Global Macro: one can translate the manager’s macro insights to portfolio management at the top level. Dynamic strategic asset allocation can be improved by using rules that have proven themselves in systematic macro strategies. These rules can be modified in a way that can be applied in overlay management or rebalancing techniques. Also, currency management can act as a significant layer of risk mitigation and market intelligence can be used to improve the portfolio balance. In those ways, a Global Macro perspective towards portfolio construction and the exposure to Global Macro strategies can help building a more robust portfolio when thinking about the unthinkable and when other asset classes disappoint.

Noot

- De auteurs zijn allen werkzaam bij Capstone Investment Advisors. Dr. Roy Hoevenaars als Portfolio Manager, Dr. Pieter Jelle van der Sluis als CIO Quantitative Strategies en Gerlof de Vrij als CEO/CIO. Het artikel is op persoonlijke titel geschreven.

in VBA Journaal door Roy Hoevenaars (r) Pieter Jelle van der Sluis (l) Gerlof de Vrij (m)