Real estate as an asset class has long been an essential component of the overall portfolio mix for institutional investors. Diversification features and favorable risk/return metrics in general have been the most important drivers for including this asset category in investment portfolios.. Institutional investors operating in large local markets have typically held property investments directly in their local markets, while investors with smaller local markets have a longer history of cross border real estate investing. As real estate investors are faced with a more efficient market due to capital overhang and a shift out of the current low yielding bonds, would this be the right time to further diversify the real estate allocation by including global unlisted opportunistic and value added real estate funds?

The starting point of this article is the debate whether to invest locally or internationally. Subsequently the different approaches to obtain international real estate exposure are described. In addition an overview will be given of the different investment styles within the unlisted real estate investment spectrum. As the last item we will address return/risk aspects which encompass more qualitative features rather than just financial viewpoints.

Cross-Border versus Local Real Estate Investing

Cross-Border versus Local Real Estate Investing

Historically, real estate portfolios of institutional investors were predominantly composed of domestic direct holdings. As a result of higher sophistication in other asset classes investors started increasingly to seek opportunities not only abroad but also through alternative approaches and structures to build their real estate allocations. Simultaneously, investors became aware of the fact that better geographical diversification within their real estate portfolio would lead to better risk/return characteristics. In addition, by broadening their horizon investors could access a larger pool of talented players in this segment of the market.

Extensive research has been published with respect to the diversification benefits of cross-border investing. Most of these studies conclude that cross-border real estate investing offers investors attractive diversification benefits. A global real estate portfolio has a low correlation to other traditional asset classes as well as among the individual regional real estate markets. Also, property offers a relatively high and stable income return, a low correlation with other asset classes and, last but not least, an effective inflation hedge1 .

While strategies employed by real estate investors are generally similar on a world-wide basis, global real estate investors benefit from the increased investment opportunity set to redevelop property which is still owned by companies and governments, particularly in Continental Europe and Asia. Also, markets function at different levels of maturity. For instance, established markets show stretched pricing which have been carried upwards by market momentum. At the same time new inefficient markets can offer tremendous opportunities for capable managers who take on risk while buying and developing property in these newer markets. Real estate is essentially a local business and a global universe allows investors to gain access to markets experiencing the best fundamentals at a specific point in time (see Hudson-Wilson, Fabozzi and Gordon).

Methods of Cross-Border Real Estate Investing

Once investors have made the decision to make cross-border real estate allocations, it should be determined whether an investment should be made in publicly listed real estate securities, or alternatively, in (“private equity”) real estate funds and other non-listed vehicles such as joint ventures. Some investors have chosen to organize listed and nonlisted forms of real estate investment activities in one single department.

The benefits of investing in indirect real estate companies compared to making investments in direct real estate are:

- Investors no longer needs internal resources to manage the in-house property portfolio;

- lower information and monitoring costs related to the inefficiency of real estate markets;

- the investor’s ability to focus on asset allocation and top-down strategies within his portfolio context;

- the investor gets access to specialist management (also in fields where indirect public equity is not present).

Private Real Estate Investing

Since 1996, when the second wave of private equity real estate funds emerged in the US that spread across Europe and Asia within a few years, the number of funds has gone through a dramatic growth phase. INREV, the European industry platform for non-listed real estate funds, manages a database which in its latest quarterly report in 2005 showed over 440 distinct vehicles, representing a gross asset value of €290 billion. In Asia growth is lagging behind Europe; however, it is catching up rapidly as managers in both Japan, China and India respond to the increasing cross-border real estate allocations to their countries. Already over 90 different real estate vehicles were counted in Asia by December 2005 (Source: Composition Capital Partners Database).

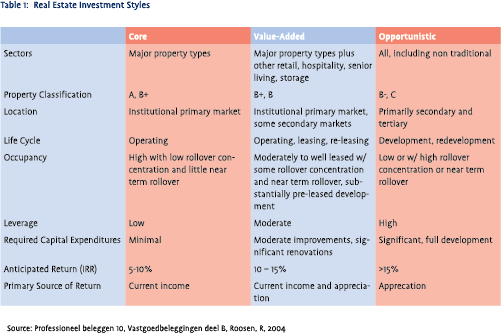

Investment Styles

Property markets in the U.S., Europe and Asia move within different stages in their respective real estate phases due to asynchronic economic cycles. Property managers with proprietary access to information can realize superior returns benefiting from inefficient information flows in the markets. In today’s environment a myriad of types of investors (typical institutional investors, family offices and high net worth individuals) employ capital globally through numerous publicly listed and non-listed vehicles.

Property markets in the U.S., Europe and Asia move within different stages in their respective real estate phases due to asynchronic economic cycles. Property managers with proprietary access to information can realize superior returns benefiting from inefficient information flows in the markets. In today’s environment a myriad of types of investors (typical institutional investors, family offices and high net worth individuals) employ capital globally through numerous publicly listed and non-listed vehicles.

Depending on their liability profile and risk appetite these investors adopt various investment styles ranging from Income-Driven (Core) to Value-Added and Opportunistic strategies (see Table 1). “Relative return” investors generally rely on a few markets where appropriate benchmarks are available (U.S., UK, Australia and some Continental European markets) while “absolute return” investors in the above mentioned markets focus on local managers executing more inventive transactions by repositioning or redevelopment of the property assets. They generally excel in deal sourcing and have a demonstrated background and distinct ability to add value. More methodical market research in less developed countries and emerging markets may be undertaken by absolute return investors to gauge local market sensitivities (country risk and liquidity risk). Obviously, risk and return go hand in hand with acquisition price levels generally being low, outlook for increasing rents, and high yields.

Value Added and Opportunistic Real Estate Risk Adjusted Returns

Measuring global real estate value added and opportunity funds’ true volatility is far from a science due to the asset class’ current limited liquidity and disclosure of returns. With no market valuation for specific funds during its lifetime, investors are left with internal rate of returns based on realized net cash flow throughout the closed end life of the fund. Data collected by Pension Consulting Alliance for the ten year period from 1991 to 2001 based on the performance of 43 managers and 110 funds suggests that opportunity funds as an asset class have produced an average gross annual return for the period of 20.66% (15.44% net of fees) with a low in 1999 of 10.45% and a high in 2001 of 30.95%.

In contrast core real estate, which has historically generated an average gross annual return of roughly between 8 and 10%. Furthermore, opportunistic real estate managers who attempt to add value to property assets, can document fairly consistent performance over subsequent funds launched by that same manager. This is a phenomenon that is well documented also in the private equity working field, an industry which shows similar characteristics. Hence, managers who have demonstrated the ability to add value to assets and buy and sell their properties in a disciplined way may generally be able to generate alpha to subsequent funds while acting with the necessary risk-consciousness. But there is no free lunch:, investors need to understand the history and the way managers produce their returns in context to the underlying real estate markets.

Measuring Market Risk

Constraints, opportunities, and risks associated with investing in foreign capital markets can be analyzed to assess the overall risk environment. We believe the following factors are important to evaluate risk with respect to value added and opportunistic international real estate investing:

- Political and fiscal stability –governmental stability, the quality of socio-economic conditions, an established and reliable legal and tax jurisdiction

- Market transparency – variables analyzed to assess the transparency of the local markets include the availability of data and benchmarks to conduct due diligence at fund level and property level.

- Liquidity and size – the overall market capitalization and the liquidity of the local markets is important to assess the overall local market volatility.

- Macro economic and real estate specific volatility – volatility in terms of the standard deviation of historical time series data can be calculated on variables such as realized returns, rental levels, local interest rates and foreign exchange rates.

Measuring Manager Risk

The manager’s investment strategy and ability to add value in order to generate excellent absolute (and relative) returns are generally measured by:

- Track record analysis – the consistency and quality of the manager’s track record with regard to the strategy and vintage year.

- Investment Strategy – value added and opportunity funds rely heavily on the expertise of the manager to generate returns by taking on prudent market risk or by taking on development, refurbishment and/or lease-up risk. The manager’s track record and return expectations have to be viewed in relation to their past and future investment strategy, management’s dedication, motivation, and investment process.

After adjusting for the risks addressed above it is fair to argue that global value added and opportunistic real estate strategies do indeed contribute measurable risk-adjusted return benefits to well diversified portfolios. However, opportunistic real estate returns should be adjusted for leverage, fees and strategy risk.

Conclusion

The rapid increasing depth of the global non-listed real estate industry allows investors to implement efficient value added and opportunistic strategies. With established property markets becoming more efficient while not delivering the required return for the level of risk it makes sense to explore alternative strategies for real estate investing. Supported by the emergence of strong industry platforms such as INREV in Europe, additional transparency and increased classification of the current and future investment universe will take place. Indirect real estate industry platform initiatives are also being established in the U.S. and Asia. Since its start INREV has been making great progress in working towards further professionalism of the non-listed industry and has installed several working committees that take on issues like corporate governance, best practices, liquidity and benchmarks. The design and implementation of benchmarks for stabilized core private funds will be useful for income producing investors. Value added and opportunistic investors, we believe, will benefit from an objective peer group benchmark. Following the trends in the private equity environment, in which peer group benchmarks have become well established, similar standards may also be initiated by the value added and opportunistic real estate investment industry.

To summarize, a more professionalized industry creates opportunities for sophisticated investors that want to build up, expand or restructure their real estate exposure. Alternative strategies such as opportunistic and value-added types of investments have delivered good returns when executed by skilled and experienced managers. A selective and in-depth analysis should ultimately contribute to top-tier risk adjusted returns.

Note

- Numerous studies and papers have been written on indirect international real estate investments. For a detailed review of literature see Sirmans and Worzela, Urban Studies, 2003.

References

- Hudson-Wilson, S, F. Fabozzi and J. Gordon, Why Real Estate?, Journal of Portfolio Management, Special Real Estate Issue 2003, pp. 12-25.

- Hahn, T., D. Geltner, and N. Gerardo Lietz, Real Estate Opportunity Funds, Journal of Portfolio Management, Special Real Estate Issue 2005, pp. 143-153.

in VBA Journaal door Børge Tangeraas and Mark Kouters,