Introduction

Catastrophe bonds (cat bonds) are a relatively new but fast growing and attractive investment opportunity. Cat bonds are designed to transfer insurance risk resulting from extremely large and costly natural catastrophes from (re)insurance companies to the capital markets in return for a risk premium. In addition to the attractive expected return, another main benefit of cat bonds is the lack of correlation with other asset classes. The unique source and characteristics of this risk premium make cat bonds a prime example of an alternative risk premium or bèta.

Catastrophe bonds (cat bonds) are a relatively new but fast growing and attractive investment opportunity. Cat bonds are designed to transfer insurance risk resulting from extremely large and costly natural catastrophes from (re)insurance companies to the capital markets in return for a risk premium. In addition to the attractive expected return, another main benefit of cat bonds is the lack of correlation with other asset classes. The unique source and characteristics of this risk premium make cat bonds a prime example of an alternative risk premium or bèta.

This article provides an introduction to cat bonds and describes the advantages and challenges for an investor. The article is divided into two sections. The first part contains an overview of catastrophe insurance and cat bonds. The second section analyses cat bonds as an investment and an attractive asset class for a well diversified investor.

The authors are investment managers for PGGM Investments which is the asset manager for Pensioenfonds Zorg en Welzijn (PFZW). PGGM Investments manages #90 bln and started investing in cat bonds in 2006.

Insurance Markets and Cat Bonds

Insurance

The basic principle behind traditional insurance is that idiosyncratic risks can be spread over many premium paying participants. This allows the insurer to diversify his risks and enables insurance purchasers to buy relatively large amounts of coverage for relatively low premiums1 . In some cases, however, the accumulated risks for the insurance writer become so large and concentrated, that it results in a systemic risk to the insurer or the industry. These large and concentrated risks are so called peak perils.

An example of a Dutch peak peril is hailstorm coverage. Although every individual insurance policy is largely idiosyncratic, the aggregate exposure of greenhouses insured may become correlated and therefore systemic during a single large storm or series of hailstorms. Hailstorm coverage therefore poses a large and systemic risk (peak peril) to a Dutch insurance company. As hailstorm coverage is largely unique to the Dutch West coast given the local greenhouse-based agriculture, this concentration quickly becomes an unattractive peak peril to the whole Dutch insurance industry which can not easily diversify this risk internally. However, Dutch hailstorm risk can be attractive to a global reinsurance company that might diversify the hailstorm risk with other perils risks such as the forest fire exposure of a Spanish based insurance company. This transfer of risk allows the Dutch insurer to fulfill his commercial ambitions in terms of growth, market share, customer relationships etc. while reducing his peak peril risk to an acceptable level.

This transfer of risk enables insurance companies to purchase coverage for their own idiosyncratic risks in the reinsurance market2. Some risks, however, become so outsized that the (re)insurance industry as a whole accumulates too much of it and needs alternative ways to lay off excess risk. This is especially the case for natural disaster insurance where the potential damage is not only extremely large but also very concentrated. As this limits the scope for diversification, (re)insurers have turned to the financial markets for diversification and capital. This has led to the development of different types of insurance-linked securities (ILS). One version of insurance-linked securities – and the topic of this article– is a cat bond that provides excess coverage against large natural catastrophes: super cats.

Super cats and financial markets

Super cat risk describes catastrophe risk that is very rare but potentially extremely costly to the insurance industry. It is primarily caused by extreme natural disasters in areas with a high concentration of residential and/or commercial property that is insured. The main categories are US hurricanes, Japanese typhoons, European winter storms, and earthquakes where the financial losses are a function of many variables including the type and severity of the event, the location and property involved, and the insurance coverage. Insurance coverage is a crucial but widely misunderstood factor. Most developing nations simply do not have any meaningful insurance coverage at all therefore also no ‘demand’ for laying off excessive cat risk. Even in developed countries, insurance coverage may exclude certain major risks. Hurricane Katrina caused massive losses through flooding which was not covered by standard homeowners insurance.

Cat bonds are developed to provide coverage against these extremely large but rare insurance industry losses and not just physical or economic losses. Cat bonds typically provide coverage against events with insurance industry losses larger than USD 10 bln to USD 100 bln and an expected occurrence of once every fifty to one hundred years or more. Although these events are impossible to predict, large scale disasters have such a significant impact that historical events can be traced back hundreds of years through the physical “scars” left behind and/or through historical accounts and provide some statistical probability on a long term basis.

Although super cat events are very rare and can theoretically be absorbed by the insurance industry by raising fresh capital and/or premiums, they are unattractive for insurance companies. Given the scale of the losses, the insurance industry tends to be ‘long’ this risk which becomes a systemic risk to the industry and its participants, impacting their cost of capital. In addition, insurance companies have to hold relatively large and expensive reserves for the very small probability of a large catastrophe. This inefficient use of the balance sheet may negatively impact the credit rating, equity valuation and premium writing ability in a competitive and market share driven industry. Changes in regulation and the enormous losses in 2004 and 2005 put many (re)insurance companies under pressure to find alternative sources of capital outside the traditional insurance markets.

Financial markets are large enough to absorb these risks since these risks are largely uncorrelated to traditional asset classes. A major catalyst to the search for alternative sources of capital was provided by the 2005 hurricane season in the US. Hurricane Katrina was the unfortunate ‘perfect storm’ as the combined damages of the 2004 and 2005 seasons reinforced the need for the insurance industry to find alternative sources of risk capital via insurance-linked securities (ILS) like cat bonds.

Cat bonds

Insurance-linked securities include many different instruments of which the premium and risk is linked to insured risks. Typical instruments include side cars, industry loss warranties (ILW’s) and cat bonds. Although they fall outside the scope of this article, side cars can be seen as private deals where an investor takes on a pro-rata share of the insurance portfolio of an insurer in exchange for a portion of the profitability of the portfolio. ILW’s are OTC contracts linked to total industry losses caused by an event. Other examples of risk sharing instruments are swaps and options, contingent capital, and CDO’s. In our opinion, cat bonds are the most liquid and transparent instruments which makes them attractive to investors such as PGGM.

Insurance-linked securities include many different instruments of which the premium and risk is linked to insured risks. Typical instruments include side cars, industry loss warranties (ILW’s) and cat bonds. Although they fall outside the scope of this article, side cars can be seen as private deals where an investor takes on a pro-rata share of the insurance portfolio of an insurer in exchange for a portion of the profitability of the portfolio. ILW’s are OTC contracts linked to total industry losses caused by an event. Other examples of risk sharing instruments are swaps and options, contingent capital, and CDO’s. In our opinion, cat bonds are the most liquid and transparent instruments which makes them attractive to investors such as PGGM.

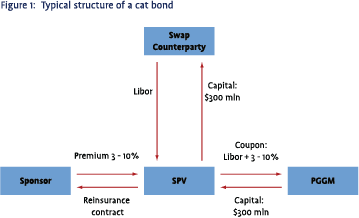

Cat bonds are floating rate bonds whose coupon and return of principal depend on the non-occurrence of a single or a combination of multiple natural catastrophes. Cat bonds are used by issuers (sponsors or cedants) to protect the upper layers of their risk profile where the frequency of an event is lowest but the impact the largest. Therefore, several other layers of coverage need to be exhausted before the cat bond exposure gets triggered (attachment point). Smaller scale risks for the global reinsurance market, or risks that can be diversified like Dutch hailstorms, will be absorbed by the lower layers. Cat bonds tend to focus on the upper layers of super cats: the very rare but extremely costly perils.

Most cat bonds have an initial maturity of between 2 to 5 years, an issuance size between $100 and $500 mln, and have an average rating of BB. The risk for the investor is that the losses associated with a predefined catastrophe are larger than the predefined attachment point. This attachment point is clearly specified in the offering documents in terms of level and estimated probability and is crucial in determining the bond’s rating. Although there are various trigger mechanisms and other nuances which are beyond the scope of this article, the structure of a cat bond is relatively standardized. The standardization and collateral mechanisms provide both the cedant and the investor with advantages over other forms of risk transfer.

Most cat bonds have an initial maturity of between 2 to 5 years, an issuance size between $100 and $500 mln, and have an average rating of BB. The risk for the investor is that the losses associated with a predefined catastrophe are larger than the predefined attachment point. This attachment point is clearly specified in the offering documents in terms of level and estimated probability and is crucial in determining the bond’s rating. Although there are various trigger mechanisms and other nuances which are beyond the scope of this article, the structure of a cat bond is relatively standardized. The standardization and collateral mechanisms provide both the cedant and the investor with advantages over other forms of risk transfer.

Cat bonds typically pay a spread over Libor of between 3 and 10% depending on the type of risk and expected loss (EL). The expected return on a cat bond is Libor + spread – EL. The expected loss can be compared to credit losses on a corporate bond. Attachment probability can be compared with the default probability with the expected loss being a function of the attachment probability and the financial impact. The probabilities and expected losses are calculated by independent modeling firms and are based on long term event scenarios and loss models. These estimates are driven by the probability of a super catastrophic event, the resulting financial losses and the insurance exposure to these losses. The output is not only uncertain in itself, but is also a statistical average over the long term. A 2% annual probability of losing 50% results in an annual expected loss of only 1% which in first instance seems low. The problem is that the probability is based on the long term estimate of a large earthquake happening once every 50 years. This may be true over the long term, but does not provide much comfort to investors if the loss distribution is uncertain and the loss event happens twice in a row or 3 times in 15 years. The expected loss is relatively reliable over the long term; the distribution of these losses in the short term is very unpredictable and creates a large and uncertain left tail in the risk-return profile.

Another important consideration is the model risk associated with the expected loss estimates. An important benefit of cat bonds over other types of insurance-linked securities is that the expected loss is independently calculated or vetted by modeling firms like EQECAT, AIR and RMS. Although these estimates are model based and are therefore subject to input and model errors, these models have been refined over the years and have a short but so far impressive track record of predicting and estimating losses when an event has happened. Much academic work has been done on earthquakes and research on tropical storms has made enormous progress over the past few years. Although this is no guarantee for success, the financial markets can price in new information very efficiently as witnessed post Katrina. The model risk in these estimates is no worse than with estimating expected default and recovery rates in corporate bonds which have much less history, are more cyclical and potentially harder to predict.

Cat bond market

Cat bond market

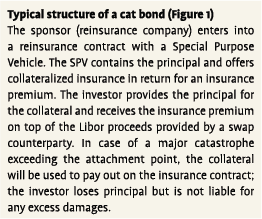

The current cat bond market consists of over 100 bonds with a total market capitalization of around US$ 14 billion. The market has seen solid growth in recent years as illustrated in Figure 2. 2006 saw an explosive growth after Hurricane Katrina raised the risk coverage demand from sponsors.

Risks in the cat bond market are concentrated by design: around 70% of the cat bond risk is concentrated within three peak perils; US wind, US earthquake and Japan earthquake. This concentration and its implications will be described later in the section on risk management. The growth of the cat bond market has been accompanied by diversification among new perils like Mexican earthquake and Australian windstorm and earthquake. Apart from these natural catastrophe exposures, other insurance bonds linked to automobile insurance, terrorism, extreme mortality, etc., have been developed which fall outside the scope of this article.

Traditional fixed income investors and specialty cat bond investors like PGGM provide roughly 2/3rd of the cat bond market capacity. Banks, hedge funds, and (re)insurance companies make up most of the balance. Hedge funds have been involved in cat bonds but play a relatively minor role as they tend to focus on higher risk/return insurance-linked securities like side cars.

Investing in Cat Bonds

Cat bonds within PGGM

Cat Bonds are part of the Portfolio of Strategies (PoS). Within PGGM the allocation to PoS is dedicated to investing in alternative risk premiums. The objective of the portfolio is to generate an attractive return of Libor +3.7% with targeted volatility of 7.5% and low correlation with existing asset classes. These strategies should have a structural and long term source of return and ideally benefit from PGGM’s strength as a large and innovative investor with a long investment horizon. Current strategies include investments in hedge funds, timber, farmland, asset based lending, volatility, carbon credits and cat bonds. Each of these strategies has its own idiosyncratic risk and return profile including potential fat tails. PGGM aims to manage the risk profile and limit exposure to traditional investment categories by appropriate sizing of the strategies and avoiding correlations between strategies.

Cat bonds as an investment

For a well diversified investor with a long term horizon, cat bonds offer many advantages.

Risk Return profile

As illustrated before, cat bonds offer an attractive spread over Libor of between 3 and 10% to compensate for the expected loss of between 1 and 3%. This spread is a function of many factors such as expected loss and peril/region involved as well as loss dynamics, technical aspects, reputation of the issuer, and traditional demand supply dynamics. These spreads fluctuate over the years and even move seasonally within a year. The high spreads post Katrina have been reduced to more normal levels in 2008 as a result of new insurance capital, increased cat bond demand and a few quiet super cat seasons.

Although these spreads look attractive, there is obvious model risk in the loss estimates and the return profile is far from normal. This strategy has a large left tail which can only be accepted with proper diversification. As standard deviation is a meaningless concept for insurance-linked investments, traditional financial tools like VaR or Sharpe ratio can not be applied. These uncertainties combined with the non-traditional nature, novelty, and niche character of cat bonds potentially explain the attractive returns4 for a large and innovative investor like PGGM.

Correlation

The unique advantage of cat bonds is the lack of correlation with other asset classes. Although the track record of cat bonds is not long enough to provide statistically significant empirical evidence, the reaction of financial markets to natural catastrophes in the past has been relatively muted and short dated. Recent examples are the 1989 San Francisco and 1995 Kobe earthquakes, and the devastating 2004 and 2005 Hurricane seasons. Even if there is a short-term negative effect on investor sentiment, damage is local and markets quickly start to factor in future recovery spending and a so called ‘demand surge’. The biggest – and yet untested risk – is a major natural catastrophe hitting a financial centre like New York, London or Tokyo. These risks can not be completely avoided in a natural cat-bond portfolio as these are obvious peak perils for the insurance industry. The impact of such a major natural catastrophes on financial markets is hard to predict. However it is expected to be different from terrorism where the direct financial losses may be relatively limited but correlation with global markets can be much more significant because of public anxiety and its consequences.

This lack of correlation also works the other way around. As of May 2008, the cat bond market has not suffered from the credit crisis and widening of spreads. Although it is too early to speculate, the fact that cat bonds are risky in itself and are held by dedicated investors with little to no leverage, may have resulted in less forced selling and pricing pressure than was seen in other ‘safer’ products.

Market growth and standardization

As illustrated in Figure 2, the cat bond market has been growing very fast with a major boost after the 2005 season. Despite the growth, cat bonds only represent a small fraction of the total reinsurance market with many more (re)insurance companies looking to diversify their risk sharing and funding. Increased use and issuance will create a more efficient and liquid market for all participants. This development, however, could also cause spreads to decline in the future.

Liquidity

Given the growth in the market and the number of institutional participants, there is reasonable liquidity and marking-to-market under normal circumstances. For example, PGGM estimates that it could liquidate its entire #450 mln portfolio within a month under normal circumstances. PGGM uses the average of three cat bond dealers bid prices to value the portfolio on a monthly basis. In our experience, prices are subject to seasonality, new supply, and natural catastrophes. However, as markets have demonstrated recently, liquidity and reliable pricing tends to disappear when most needed like when a financial or natural storm is developing or a catastrophe has just happened. In many of these circumstances, no market participant knows the value of the bonds and will conservatively mark bonds down. Cat bonds are therefore not suited for active trading around catastrophes, but offer reasonable liquidity and pricing outside of “live cat” situations.

Advantages for issuers

Cat bonds are attractive for issuers as well. In addition to the large pool of fresh capital, cat bonds offer multi-year protection with full collateralization. Although traditional reinsurance can be cheaper and easier to execute, pricing and capital tends to be very cyclical and least attractive when most needed. Reinsurance also creates counterparty (credit) risk which becomes more relevant as the aggregate risk grows and becomes systemic in nature. The growth of the cat bond market with established programs further increases standardization and lowers barriers to entry and costs for both issuers and investors.

Risk management of cat bonds

Portfolio management

Unlike traditional insurance contracts and certain derivatives, cat bonds do have a clearly defined maximum loss under specified circumstances. The exposure of a cat bond portfolio to certain catastrophes and/or regions can be accurately measured and managed5. This allows the investor to analyze and manage the risk exposure on both an expected and maximum loss basis. For example, as per the end of 2007, PGGM’s cat bond portfolio had a yield spread of 4.55% over US 3M Libor, a weighted average expected annual loss of 1.13%, an expected loss on a 1-in100 year basis of 22%, and a maximum principal loss exposure to a single event of 30%.

A potential problem is that these numbers do not fit into traditional risk models and VaR estimates, as these assume a normal distribution. Cat bonds returns are definitely not normally distributed but almost binary. For a single cat bond, a 2% expected loss almost never generates a 2% loss per year; a more likely distribution is a 50% loss every 25 years or a full write off once every 50 years.

For the portfolio of alternative strategies, PGGM uses 95% VaR, based on monthly returns, to manage and allocate risk capital. The models suggest that for cat bonds this once-every-20 month loss is close to zero, but this would massively understate the size of the left tail of the distribution. The conservative but practical solution PGGM has chosen is to look at the 1-in-100 year loss (currently 22%) as a proxy for the 99% VaR and scale this back to a monthly VaR of 6.4%. Although this looks overly conservative, it may compensate for the model risk, input risk, and extreme loss distribution.

Lack of peril diversification

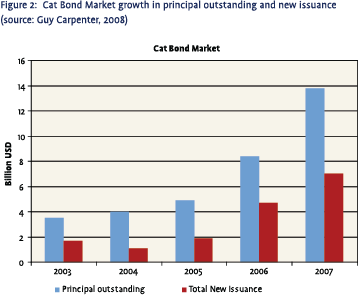

As described before, the risks in a cat bond portfolio are very concentrated in a few peak perils implying a large exposure to a single event. The obvious remedy is to diversify over more perils. However, this peril concentration is the exact reason that the insurance industry is overexposed and needs to use the financial markets. This risk concentration explains why the peak exposures pay the highest premium per unit of risk and form such a large part of the cat bonds market. Figure 3 illustrates the risk concentration of PGGM’s cat bond portfolio.

As described before, the risks in a cat bond portfolio are very concentrated in a few peak perils implying a large exposure to a single event. The obvious remedy is to diversify over more perils. However, this peril concentration is the exact reason that the insurance industry is overexposed and needs to use the financial markets. This risk concentration explains why the peak exposures pay the highest premium per unit of risk and form such a large part of the cat bonds market. Figure 3 illustrates the risk concentration of PGGM’s cat bond portfolio.

Although this risk concentration is a big problem for the insurance industry and a potential issue for a cat bond portfolio, it is less problematic for diversified investors like PGGM that can diversify these risks internally. Although PGGM’s intention is to have exposure to the broad cat bond market in order to ‘harvest’ this alternative market premium, PGGM puts two restrictions on the cat bond portfolio:

- The maximum exposure to a single event is limited to 50%; this is intended to avoid too much concentration in a single peak peril.

- Expected loss on a 1-in-100 year basis is limited to 33%: this enforces a relatively conservative portfolio as it focuses the portfolio on the lower frequency part of the cat bond market.

In addition to risk limits within the portfolio, PGGM limits the total size of the total cat bond portfolio. The current portfolio of around #450 mln is only 0.5% of PGGM’s total assets. The probability that all will be lost due to an exceptional combination of global natural catastrophes is less than once in 100,000 years.

Understanding cat risk

The obvious risk is the occurrence of a rare but large natural catastrophe. Since the attachment points of cat bonds are remote, these catastrophes need to be extremely large and at an adverse location from a financial standpoint. There are on average about 15,000 magnitude 4 (Richter scale) or greater earthquakes a year but only a large earthquake with certain characteristics can do significant damage to a large urban population. Cat bonds are most vulnerable to damaging earthquakes in California and Japan and wind damage in Japan, US and Europe. For the Redwood bond described above to be wiped out, one would essentially need a specifically placed magnitude 7.0+ California Earthquake that would likely cause economic damages in excess of $100 billion and $50 billion in insured losses.

Although some significant hurricanes have striked the US during the last few years and one of the largest European storms to hit Europe in 2007 (Kyrill), the damage to outstanding cat bonds has been minor. Only one bond was hit by the extraordinary active and damaging 2005 season for a total loss of less than 4% to total outstanding cat bonds. All other events have had no significant impact on the market. Although cat bonds focus on the rare and extremely costly incidents, other instruments like ILW’s and side car contracts or traditional reinsurance contracts typically provide protection against less remote and less costly events. These other instruments focus on lower layer risks and typically pay a higher premium for higher expected losses.

Global warming

Most people assume that global warming automatically leads to higher sea surface temperatures and to more tropical storms. This is a complicated and controversial topic of active debate, which is also beyond the scope of this article. PGGM’s judgment is that there may be evidence of more powerful storms as a result of global warming, but that this is adequately reflected in the expected losses and risk premiums. In addition, global warming and associated effects may happen over many decades whereas cat bonds cover risk over a much shorter time span. The systemic risk of underestimating these effects may be one of the model risks highlighted previously.

Conclusion

Cat bonds offer investors the opportunity to invest in insurance risk in a relatively easy to understand and implement fashion. Cat bonds offer an attractive risk return profile with low correlation to traditional asset classes which has been demonstrated by recent events in the credit market. Due to increasing standardization and acceptance by both issuers and investors, this market is expected to continue to grow and develop. The main challenge with a cat bond portfolio is the interpretation and management of the risk profile given the extreme distribution and size of losses. In addition to the tail risk caused by natural catastrophes, cat bonds are subject to model risk in the expected loss calculations.

Notes

- The same principle applies to homeowners insurance. As the risk of many properties being destroyed simultaneously is very small, annual premium rates are only a small fraction of the value of the property.

- Reinsurance companies were first started in 1842 in response to the Great Fire of Hamburg which ended the 160 year prosperous operation of the Hamburg Fire Fund.

- The bond and some details can be found on Bloomberg by using 75778F306

- A recent innovation that may help investors track the cat bond market are the Swiss Re Cat Bond indices that can be found on Bloomberg (SRCATTR and SRBBTRR ).

- Although the expected losses are an estimate and may be prone to model and/or input errors and or timing/bad luck, these effects diminish as the portfolio grows and no systemic errors are made

in VBA Journaal door Peter-Jan de Koning (l) en Rogier Leeuwenburgh (r)