From cryptocurrencies to pensions in the blockchain

Blockchain technology has become well-known through cryptocurrencies such as Bitcoin. In addition to these, there are many areas in which blockchain technology can change how we currently do business. In essence, a blockchain is a publicly visible ledger that stores transactions which cannot be tampered with. In the ledger, transactions are chained with a cryptographic seal so that any attempt to change one of them will break the chain. With Bitcoin, the cryptographic layer is imposed when transactions are processed in a process called “mining”. The blockchain database keeps track of who owns how many bitcoins without the need of a central party, i.e., it is autonomous. Consequently, there is no need to put your trust in a third party; within the blockchain community this is referred to as trustlessness.

Blockchain technology has become well-known through cryptocurrencies such as Bitcoin. In addition to these, there are many areas in which blockchain technology can change how we currently do business. In essence, a blockchain is a publicly visible ledger that stores transactions which cannot be tampered with. In the ledger, transactions are chained with a cryptographic seal so that any attempt to change one of them will break the chain. With Bitcoin, the cryptographic layer is imposed when transactions are processed in a process called “mining”. The blockchain database keeps track of who owns how many bitcoins without the need of a central party, i.e., it is autonomous. Consequently, there is no need to put your trust in a third party; within the blockchain community this is referred to as trustlessness.

Many people put their trust in pension funds to take care of their retirement savings. Although in many Western countries people are concerned that pension funds are insufficiently funded, there are many other places in the world where people have well-founded concerns about the sustainability and even the integrity of pension funds, see, e.g., the 2017 Melbourne Mercer Global Pension Index. Organizing pension plans in a blockchain can help solve this problem. As discussed in van Benthem et al. (2018), the technology can be used to set up an autonomous pension scheme in the blockchain in which people share longevity risk peer-to-peer.

Trustlessness is the most important aspect of blockchain technology with which it can disrupt traditional financial services. But even when trust is not the participant’s biggest concern, there is significant added value. Since pension providers have huge difficulties engaging their participants (Blakstad, Bruggen and Post, 2017), there are few participants that deviate from default choices (van Rooij and Teppa, 2008). Blockchain technology offers an opportunity to autonomously execute a pension fund where participants follow a personalized strategy tailored to their situation. Ideally, the strategy steers or “nudges” the participant to an allocation that helps him attain his goals with less risk and requires limited active involvement.

Although blockchain technology is certainly not the only way to automate the execution of pension funds, the technology is especially suited to efficiently aggregate the execution of personalized strategies. We will describe a set-up by connecting three pieces: an autonomous pension scheme in the blockchain, autonomous asset management in the blockchain and a personalized strategy tailored to the participant’s goal.

Asset management in the blockchain

Blockchain technology can efficiently execute a pension fund where every participant has a personalized investment strategy through smart contracts. Although a complete understanding of smart contracts requires an in-depth knowledge of blockchain technology, the concept can be explained by looking at how bitcoin transactions are processed, i.e., mining. The process consists of the execution of a piece of code that processes the transaction, the computation of the cryptographic seal, and the addition of the transaction together with its seal to the blockchain. Smart contracts generalize this process to execution of not only transactions but to execution of any set of rules. When requested, a smart contract can be executed and its results, namely the contract’s rules and state information, are then added to the blockchain. As a result, smart contracts allow counterparties without particular trust in each other to agree on business rules which, once set in motion, cannot be altered by either of them. Some contracts have already been used to run lotteries and crowd funding schemes in public blockchains.

Blockchain technology can autonomously execute a pension fund where participants follow a personalized strategy

To set up a pension fund in the blockchain where every participant has a personalized investment strategy, several components are needed. First, since pension savings are typically invested in traditional assets such as stocks, bonds, real estate and currency hedging contracts, these assets should be represented in the blockchain by digital tokens. Each token works like a bitcoin but is, similarly to a share of an exchange traded fund, backed up by collateral of the underlying assets. Instead of on a stock exchange, these assets can now be traded in the blockchain with minimal transaction costs.2 The custody of the token’s collateral, however, must be guaranteed by a traditional legal framework such as a stock exchange. For further details, we refer to the digital tokens that are already live: Tramonex’s GBP token on Ethereum, Decentralised Capital’s Euro token and several precious metal tokens such as Digix’s token representing gold.

Second, in the blockchain, smart contracts can be used, similarly to mutual funds, to aggregate digital tokens into a fund. These asset management contracts contain the fund’s strategy and can set limits, e.g., on the type of assets that can be invested in. The contracts can be created with the recently developed Melonport protocol (Trinkler and el Isa, 2017). Although asset management in the blockchain can potentially save costs due to automation, its main advantage over other forms of automation is that it makes the process autonomous so that no human interaction or intermediaries are needed.

Third, although individuals could, in principle, set up their own fund which follows their preferred dynamic strategy, it might be even more beneficial to aggregate dynamic strategies of say all participants in a pension fund and create a fund that executes the aggregated strategy. Pension fund participants can then subscribe to this collective smart contract with their personalized strategy tailored to their goals and preferences. Since the collective smart contract trades only on an aggregated level, transaction cost are kept to a minimum. Although ordinary mutual funds also aggregate transactions, the collective smart contract is peer-to-peer and provides aggregation to participants without the cost associated to the intermediary, i.e., a traditional mutual fund.

Blockchain technology for smart contracts and asset management in the blockchain are currently under active development. One of the big obstacles is that public blockchains do not yet scale well and, thus, it is often not possible to execute complex smart contracts on them, see Boon and Buterin (2017) for a discussion on scalability and one of its potential solutions. Complex smart contracts can, however, already run well on private blockchains, that is, blockchains managed by a central party. Another obstacle in public blockchains is security, e.g., the risk of someone losing their key with which they have access to their pension. Again, with private blockchains, the central party managing the chain can help to solve these problems by undoing damage and making changes to the blockchain. Regardless of current limitations, the huge interest in blockchain technology stimulates its development so that most issues might very well be overcome within the next few years.

Nudge: improving decisions about pensions

Most people only have a limited interest in their pensions and pension providers have huge difficulties engaging their participants (Blakstad, Bruggen and Post, 2017). Van Rooij and Teppa (2008), for example, show that most people who can deviate from the default lifecycle don’t do so. With pension providers moving towards individual DC schemes, this raises the question whether people will make decisions that are in their own interest. Through smart contracts, blockchain technology offers a perfect opportunity to apply a nudge. A nudge, as Thaler and Sunstein put it in their book Nudge: Improving Decisions About Health, Wealth, and Happiness, is “any aspect of the choice architecture that alters people’s behavior in a predictable way without forbidding any options or significantly changing their economic incentives.”

A commonly used example of a nudge is providing a good default choice. Traditional lifecycle investment strategies, e.g., Bogle’s rule that states that the fraction to be invested in risky assets equals 100 minus your age, can provide good defaults. But they are not tailored to the participant’s situation, as they do not account for the participant’s savings, house ownership and potential preferences for early retirement. In addition, traditional lifecycles only depend on the investor’s age and thereby do not adapt to changing circumstances.

With the current active development, many issues with blockchain technology might very well be overcome within the next few years

What could be a good default strategy? For most people, one might argue that pension savings need to provide a retirement income that replaces a significant part of their salary, say 70%. But for people with significant savings or for house owners, a lower target of say 50% might be sufficient. Taking on investment risk should contribute to achieving this replacement ratio goal. Ideally, a participant in a pension fund could follow a dynamic strategy which is tailored to his personal situation and which dynamically adjusts the amount of risk he takes. When all goes well, e.g., when there have been several good years on the stock market, the participant can take less risk in the following years and still achieve his goal.

In practice, it is often not possible for pension fund participants to follow a dynamic strategy tailored to their goals. Once a strategy is determined and tailored to the participant’s goals, blockchain technology can help with the execution of such strategies. As discussed, blockchain technology is certainly not the only way to execute such strategies, but smart contracts seem an ideal fit since they are made for execution based on rules that can differ between participants in the fund.

Tailored investment strategies

We give a simplified example of how a personalized strategy could work. Consider a pension fund participant in, say, South America who is concerned about corruption and mismanagement in the institutions that manage his pension money. Therefore, he decides to put his money in an autonomous blockchain pension scheme, see van Benthem et al. (2018) for a discussion. Also, he prefers to save in USD and accepts the associated currency risk. Currently, he owns 10.000 USD and hopes to obtain 55.000 USD in 40 years.

We give a simplified example of how a personalized strategy could work. Consider a pension fund participant in, say, South America who is concerned about corruption and mismanagement in the institutions that manage his pension money. Therefore, he decides to put his money in an autonomous blockchain pension scheme, see van Benthem et al. (2018) for a discussion. Also, he prefers to save in USD and accepts the associated currency risk. Currently, he owns 10.000 USD and hopes to obtain 55.000 USD in 40 years.

Smart contracts seem an ideal fit for execution based on rules that can differ between participants

For his situation, we created a personalized dynamic strategy that can invest in two asset classes: equity and bonds. The dynamic strategy makes investment decisions annually and lets, say at the end of each year, the fraction to be invested in equity depend linearly on the investor’s age and wealth at the end of that year. Using a proprietary scenario model (Steehouwer, 2016), we calibrated the strategy in such a way that it is most likely that the investor reaches his goal. Without a dependence on time and wealth, such a strategy is also dynamic and is called yearly rebalancing. With only a dependence on time, the strategy could be seen as a lifecycle where the fraction to be invested in risky assets only depends on the investor’s age, e.g., Bogle’s rule. This dynamic strategy extends traditional lifecycles in that sense that is tailored to his personal goal and in the sense that it adjusts the allocation to equity according to his wealth, or, in other words, how far he is from reaching his goal.

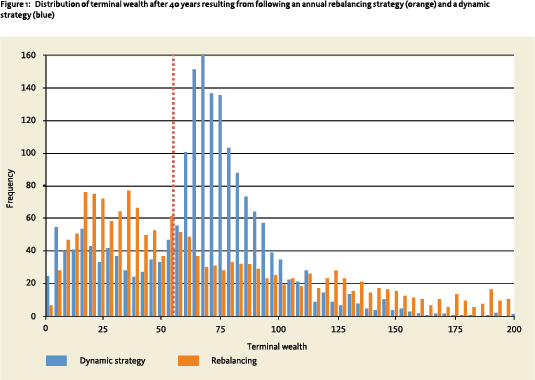

Figure 1 compares the annual rebalancing strategy with the dynamic strategy. Both strategies are calibrated so that they make it most likely for the investor to reach his goal. As indicated, the dynamic strategy significantly decreases the likelihood of outcomes below the investor’s target of 50.000 USD from 42% for the annual rebalancing strategy to 28% for the dynamic strategy.

By decreasing risk once the investor is close to his goal, the dynamic strategy prevents unnecessary risk taking

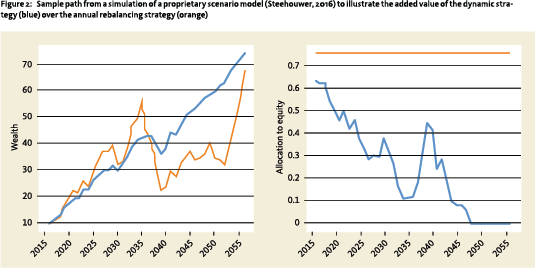

In addition, the dynamic strategy achieves the participant’s goal by taking less risk: the average allocation to equity decreases from 76% for the optimal rebalancing strategy to 53% for the optimal dynamic strategy. To further illustrate the workings of the dynamic strategy, Figure 2 shows a simulation path in which the dynamic strategy works well. After several good years on the stock market, the dynamic strategy decreases its allocation to equity (which can result in significantly higher, but also lower returns). Although in both cases the investor reaches his target terminal wealth of 55.000 USD, the dynamic strategy has a smoother sailing towards this goal. By decreasing risk once the investor is close to his goal, the dynamic strategy prevents unnecessary risk taking.

In addition, the dynamic strategy achieves the participant’s goal by taking less risk: the average allocation to equity decreases from 76% for the optimal rebalancing strategy to 53% for the optimal dynamic strategy. To further illustrate the workings of the dynamic strategy, Figure 2 shows a simulation path in which the dynamic strategy works well. After several good years on the stock market, the dynamic strategy decreases its allocation to equity (which can result in significantly higher, but also lower returns). Although in both cases the investor reaches his target terminal wealth of 55.000 USD, the dynamic strategy has a smoother sailing towards this goal. By decreasing risk once the investor is close to his goal, the dynamic strategy prevents unnecessary risk taking.

An often mentioned drawback of dynamic strategies, especially ones trading at high frequencies, is that their implementation requires additional trading and that the transaction cost involved does not outweigh the additional advantages. In the example discussed here, the annual turnover is roughly 6% for the rebalancing strategy and 10% for the dynamic strategy. As discussed, blockchain technology can help to lower cost, because pension schemes in the blockchain can efficiently aggregate transactions of the personalized dynamic strategies. Additionally, blockchain technology can make asset management in the blockchain autonomous, removing the need for intermediaries.

Know your customer!

When blockchain technology makes personalized dynamic strategies possible, there will be challenges for regulators. To what extent can we be sure that a dynamic strategy that automatically makes decisions, makes them in the client’s interest? And to what extend do people understand what they set in motion when they choose a dynamic strategy? Although these concerns also hold for personalized dynamic strategies facilitated without a blockchain, blockchain technology makes execution autonomous and, by construction, makes it harder to change smart contracts, containing for example a dynamic strategy, once set in motion. We believe that these are important concerns, but that eventually they can be addressed appropriately.

First, simple measures can limit the potential damage related to many risks. For example, one could limit the allocation to risky assets in a dynamic strategy to be, say, at most 10% more than in a corresponding static strategy. This should give sufficient comfort that the strategy will not do something unforeseen. Also, a smart contract in the blockchain could be given a kill-switch that disables the dynamic strategy and sets it back to a static strategy. This ensures that one can, for whatever reason, always go back to the current practice.

Second, although dynamic strategies can serve other purposes, we want to use the dynamic strategy as a nudge that steers people to making good decisions. When tailored to the individual and used properly, dynamic strategies can be better defaults than their static counterparts.

Conclusion

Blockchain technology can efficiently aggregate personalized strategies in an autonomous pension fund in the blockchain. Smart contracts offer an opportunity to implement strategies that steer or “nudge” participants to making good decisions and help them achieve their goals with less risk. Although blockchain technology is not yet sufficiently mature, we believe that with the current active developments pensions in the blockchain can be made possible in the near future.

References

- van Benthem, L.,L. Frehen, J. Cramwinckel, and R. de Kort, 2018, Tonchain: the future of pensions?, VBA Journaal, nr. 134.

- Blakstad, M., E. Bruggen, and T. Post, 2017, Life events and participant engagement in pension plans, Netspar design paper, nr. 93.

- Melbourne Mercer Global Pension Index, 2017. Online report available at: https://www.mercer.com.au/our-thinking/ mmgpi.html.

- Poon, V. and V. Buterin, 2017, Plasma: scalable autonomous smart contracts, working paper.

- van Rooij, M., and F. Teppa, 2008, Choice or no choice: What explains the attractiveness of Default options, Netspar discussion paper, nr. 32.

- Steehouwer, H., 2016, Relevance of scenario models, Ortec Finance white paper.

- Thaler, R.H. and C.R. Sunstein, 2008, Nudge: Improving Decisions about Health, Wealth, and Happiness. Yale University Press, ISBN 978-0-14-311526-7.

- Trinkler, R. and M. el Isa, 2017, Melon protocol: a blockchain protocol for digital asset management, white paper.

Notes

- Joris Cramwinckel, Stanimir Ivanov and Martin van der Schans, Ortec Finance.

- Although bitcoin transaction fees are currently ranging between 1$ – 4$, this need not be the case in specialized blockchains such as EOS where the mining process is delegated to a limited group of miners. This method significantly reduces the effort to process transactions and thereby the required energy consumption and cost associated to the transaction.

in VBA Journaal door Martin van der Schans (l), Joris Cramwinckel (m), Stanimir Ivanov (r)