This article gives an overview of developments in sustainability (also labelled corporate social responsibility) reporting, a topic that is of clear interest to investors. Retail social investors are looking for more information from companies through for example sustainability reports (Haigh, 2005). And a recent international survey showed that most investors and financial research and rating agencies found these reports useful for their professional work (Pleon, 2005); the overwhelming majority also thought that it would make sense to make such reporting mandatory, and favoured external verification and further standardisation through global guidelines. With growing attention to socially responsible investments, also on the part of institutional investors, and the emergence of a range of sustainable indices, the quest for information as contained inter alia in sustainability reports can only be expected to increase further.

This article gives an overview of developments in sustainability (also labelled corporate social responsibility) reporting, a topic that is of clear interest to investors. Retail social investors are looking for more information from companies through for example sustainability reports (Haigh, 2005). And a recent international survey showed that most investors and financial research and rating agencies found these reports useful for their professional work (Pleon, 2005); the overwhelming majority also thought that it would make sense to make such reporting mandatory, and favoured external verification and further standardisation through global guidelines. With growing attention to socially responsible investments, also on the part of institutional investors, and the emergence of a range of sustainable indices, the quest for information as contained inter alia in sustainability reports can only be expected to increase further.

The article will first briefly indicate how accountability on social and environmental issues started, already in the 1970s when social reports were published. Subsequently, more detailed trends and their peculiarities are given for the period from the early 1990s onwards, based on longitudinal research in which the author has been involved. In addition to data on the extent of sustainability reporting, some attention will also be paid to (regulatory) drivers and motivations for reporting as well as trends in report types and contents. The final section briefly discusses sustainability reporting in the financial sector where interesting developments have taken place in recent years.

Trends in reporting

Reporting related to the social and environmental aspects of business first received considerable academic and managerial interest in the 1970s. In this “first wave”, a number of companies in the US and Western Europe adopted practices of so-called social reporting and accounting, defined at the time as “the identification, measurement, monitoring and reporting of the social and economic effects of an institution on society”, “intended for both internal managerial and external accountability purposes” (Epstein et al. 1976, p. 24). In the US, Ernst & Ernst surveys tracked developments in the course of the decade, which showed that, by 1978, 90% of the Fortune 500 companies reported on social performance in their annual reports. The amount of social information they published was rather limited, however, frequently less a quarter of a page or less. In Europe, social reporting occurred most frequently in Germany, the Netherlands and France (US Department of Commerce 1979). Compared to the US, European reports focused more on employee matters and less on local community and environmental impacts, and contained more quantitative information.

Overall, however, this phenomenon lasted less than a decade; in the 1980s, social reporting lost momentum (Dierkes and Antal 1986). It turned out that social reporting was not institutionalized, with interest fading away both internally, within organizations, and externally, in the realm of wider societal attention and at the level of governments. As a result of recession and unemployment, attention shifted more to the economy, market-oriented policies emerged and accountability on social and environmental issues apparently became less important. Social reporting declined, and only a small number of companies continued to show activities. The 1970s movement for accountability, which was largely initiated by academics, quickly followed by a few accounting professionals, did lead to the emergence of several reporting/accounting models and standards (e.g. Epstein et al, 1976; Dierkes and Antal, 1986), but not many people currently interested in the topic seem to know about this all.

In the late 1980s, reporting on non-financial issues re-emerged, but this time with a particular focus on environmental issues and with most attention being paid to external, accountability dimensions, influenced by pressure from non-governmental organisations (NGOs). First-moving companies in this “second wave” included Eastman Kodak and Norsk Hydro, which both published an environmental report in 1989. Since then, this practice has grown substantially, particularly in the form of separate reports. Data on more than a decade of corporate reporting practices have been compiled by KPMG in surveys held every three years since 1993 (KPMG 1993, 1997, 1999, 2002, 2005).1 Figure 1 shows the percentages for the largest 100 companies in a considerable number of countries that were included several times. Not all countries were covered each year, but nevertheless the figure gives a good insight in overall tendencies plus the differences between countries.

In the late 1980s, reporting on non-financial issues re-emerged, but this time with a particular focus on environmental issues and with most attention being paid to external, accountability dimensions, influenced by pressure from non-governmental organisations (NGOs). First-moving companies in this “second wave” included Eastman Kodak and Norsk Hydro, which both published an environmental report in 1989. Since then, this practice has grown substantially, particularly in the form of separate reports. Data on more than a decade of corporate reporting practices have been compiled by KPMG in surveys held every three years since 1993 (KPMG 1993, 1997, 1999, 2002, 2005).1 Figure 1 shows the percentages for the largest 100 companies in a considerable number of countries that were included several times. Not all countries were covered each year, but nevertheless the figure gives a good insight in overall tendencies plus the differences between countries.

Overall, a steady increase in reporting can be observed, from 13% in 1993 to 41% in 2005. In 2002, the figures included, for the first time, a substantial number of sustainability reports, which refer to social responsibility as well (KPMG 2002). This tendency has further increased in 2005 (see below). Figure 1 (see page 35) demonstrates that, while sustainability reporting has increased overall in the past decade, there are also clear differences between the countries. Some early movers are lagging behind in more recent years (most notably Norway, Sweden, Denmark), while others have followed the general patterns, though sometimes with higher percentages and growth rates (Netherlands, Finland). In recent surveys, the UK has consistently been among the countries where a high percentage of non-financial reports has been published. The only country that has scored higher in 2002 and 2005 is Japan, where reporting has really taken off at a tremendous speed. Corporate reporting in Belgium has traditionally not been very common. This was the case in other countries as well, but there the past few years have seen a considerable increase. Notable in this respect are Southern European countries, Australia, and particularly Canada, France and South Africa.

Whereas the number of banks and insurance companies that publishes a sustainability report has increased significantly in recent years, traditionally the industrial, more ‘polluting’ sectors have been most active in this regard. Research on the largest 250 multinationals (the Global Fortune 250) shows that in the financial sector, 57% published a report in 2005 (this was 25% in 2002, and 17% in 1999). Overall percentages in these years were 64%, 50% and 37% (Kolk 2003, KPMG 2005). This shows not only the fact that the financial sector is almost catching up, but also that percentages for these Fortune Global 250 companies are higher than the figures reported above. Reporting is more common in the case of these large multinationals in view of their higher visibility and impact. Besides financial companies, other sectors which have traditionally reported less than average are trade and retail, services, and communications and media, but it must be noted that significant increases can be observed in recent years. This means that differences with (traditionally high reporting) sectors such as chemicals and pharmaceuticals, computers and electronics, autos, utilities, and oil and gas, are decreasing.

With regard to the developments at the country level, the Fortune Global 250 research confirms the tendencies noted in figure 1. The trends can be analysed more accurately, however, because of the availability of panel data. Compared to the sets of top 100 companies in the different countries, which change per survey, the largest multinationals of the Fortune list have been scrutinised for their reporting behaviour in 1999, 2002 and 2005. This showed that reporting increased significantly overall, but particularly in France (where 94% of the multinationals reported in 2005, while it was 39% in 2002 and 17% in 1999), the UK (100% in 2005, from 71% and 57% respectively), Germany (86% in 2005; previously 57% and 52%) and Japan (74%; from 65% and 43%). Although with a smaller number of companies in the Fortune Global 250, the Netherlands also scored high with 94% in 2005. Lagging behind were US (44%) and South Korean (17%) companies.

Drivers and motivations

Drivers and motivations

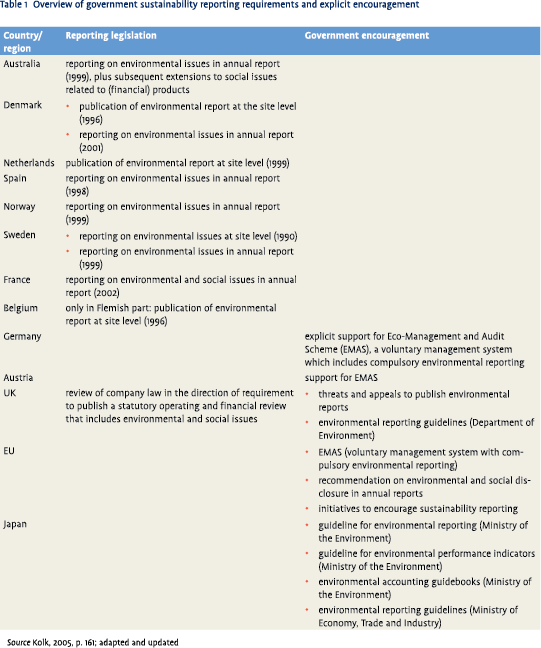

The situation in the different countries can be linked to the level of regulatory and societal attention. This involves legislation on environmental and social reporting, in force in a few countries, and more importantly, other forms of government encouragements of such types of disclosures, for example through the publication of official reporting guidelines (Kolk, 2003, 2005; KPMG, 2005). An overview for a range of countries can be found in table 1. It must be noted that regulation has merely been an indirect stimulus, however, because direct requirements to publish separate corporate reports have been lacking in many cases (both the Danish and the Dutch laws focus on the site level). Nevertheless, it is obvious that for example French legislation has been a direct driver for increased reporting: it raised companies’ awareness of the importance of accountability on environmental and social issues. Likewise, the publication of reporting and accounting guidelines in Japan has played a large role in stimulating the publication of such reports in this country.

Table 1 does not include a range of other voluntary guidelines that have emerged over the years in different countries, issued by other (‘non-government’) organisations at the national level. Examples include employers’ organisations’ standards for reporting in South Africa and Norway, guidelines for reporting and assurance as developed by a range of national accounting and standards boards (in the Netherlands by the Raad voor de Jaarverslaggeving and NIVRA). Securities and exchange commissions in some countries also set standards for disclosure, as do other bodies that implement international accounting standards. There is a movement towards stricter requirements in many areas following accounting scandals in the past few years (and Sarbanes-Oxley). Voluntary sustainability reporting and assurance guidelines are also being developed by a range of other organisations (for an overview, see KPMG, 2005), the most well-known is the Global Reporting Initiative (see below).

In addition to regulation and related incentives, companies can have a range of other reasons for publishing a sustainability report (or not). Table 2 lists various motivations, compiled from in a study by Sustainability and UNEP in which reporters and non-reporters were interviewed. Besides internal, sometimes company-specific, reasons, societal aspects, such as credibility and reputation play an important role. Apparently, for an increasing and substantial number of companies, the arguments in favour of reporting prevail over those against. This applies in particular to the largest, most visible multinational companies.

Obviously, since this list of reasons was compiled, around 1998, the situation has changed to some extent. The fact that competitors are neither publishing reports becomes, with increasing numbers, less relevant; in fact, it is the other way around: as more and more companies in certain sectors publish reports, a bandwagon effect further strengthens this tendency. Moreover, while it continues to be difficult to gather consistent data, selection of indicators has been facilitated by the publication of guidelines and formats. In addition to the ones mentioned in table 1, especially the international multistakeholder Global Reporting Initiative is notable with its extensive guidelines to improve the “quality, rigor, and utility of sustainability reporting” (GRI, 2002, p. 1).

Obviously, since this list of reasons was compiled, around 1998, the situation has changed to some extent. The fact that competitors are neither publishing reports becomes, with increasing numbers, less relevant; in fact, it is the other way around: as more and more companies in certain sectors publish reports, a bandwagon effect further strengthens this tendency. Moreover, while it continues to be difficult to gather consistent data, selection of indicators has been facilitated by the publication of guidelines and formats. In addition to the ones mentioned in table 1, especially the international multistakeholder Global Reporting Initiative is notable with its extensive guidelines to improve the “quality, rigor, and utility of sustainability reporting” (GRI, 2002, p. 1).

A growing number of companies refers to the GRI as having inspired their reporting. Slightly over half (52.5%) of the Fortune Global 250 in the 2005 survey mentioned GRI in the report. This does, however, not mean that companies follow the guidelines strictly, fully or consistently – they frequently take some components of the extensive set. In 2005, 29% of the reports was specific about what parts of GRI were used and 6% declared to be in accordance with GRI. Companies sometimes also use the GRI guidelines to select the issues they include in their reports; this applied to 40% of the Fortune Global 250, and it turned out to be the most frequently mentioned tool to do this (‘stakeholder consultation’ in general was second with a score of 20%). Another way is which GRI turns out to play some role is in external verification; 9% mentioned that the guidelines were part of this in one way or the other.

Report types and contents

In spite of growing attention to standardisation, a wide variety of reports can still be noted, with substantial differences in titles, length, approach, scope, depth and contents. Some straightforward developments are notable, however.

A clear tendency is that environmental reporting has broadened to an inclusion of social, and sometimes also financial, issues. This is a fairly recent development, since in 1999, such ‘broader’ reports were still rather exceptional. In 2002, the percentage of ‘pure’ environmental reports published by the largest 250 multinationals declined to 71% (from 98% in 1999); in 2005 it fell to 13%. Of the broader reports, the overwhelming majority currently combines environmental and social information with some data on economic aspects (although it must be noted that the amount of economic data is usually rather limited still). But companies are clearly moving in the direction of sustainability reporting (sometimes also called ‘triple bottom line’ reporting), about the social, environmental and financial situation. An interesting new phenomenon is that some companies integrate a sustainability section in their annual (financial) report. Of the 2005 Fortune Global 250, 20% followed this path, while another 54% published a separate sustainability report.

It must be noted, however, that ‘sustainability’ reporting (whether separate or included in annual reports) still tends to focus largely on the more ‘traditional’ reporting topics: those related to health and safety (usually included in environmental/HSE reports), employee relationships (which some companies address in internal social reports), and philanthropy and charitable contributions (frequently covered in community reports). The most common performance indicators included in reports also largely relate to environment, health and safety (accident/injury frequency), community spending and the composition of the workforce.

Especially Japanese companies stand out in this respect because they very frequently include environmental costs and benefits in their reports. A recent study showed that 75% of large Japanese multinationals mentioned explicit environmental accounting indicators in their report, while this was just below 30% for their US and European counterparts (Kolk, 2005). This reflects the Japanese traditional orientation on environment (and driven by government guidelines, also on the accounting of it), as well as the tendency for US and European companies to take a broader sustainability orientation in reporting.

As shown in table 3, there is – besides this distinction between Japan on the one hand, and US/Europe on the other – another aspect that characterises the European approach to reporting in particular: the external (voluntary) verification. European companies are relatively most active in requesting third parties to check the reliability of their reports (this applied to 45% in the 2005 Global Fortune 250). This type of external legitimacy is apparently seen as less necessary or appropriate in Japan (24%), and definitely least in the US (3%). On average, almost a third of the reports is verified.

As shown in table 3, there is – besides this distinction between Japan on the one hand, and US/Europe on the other – another aspect that characterises the European approach to reporting in particular: the external (voluntary) verification. European companies are relatively most active in requesting third parties to check the reliability of their reports (this applied to 45% in the 2005 Global Fortune 250). This type of external legitimacy is apparently seen as less necessary or appropriate in Japan (24%), and definitely least in the US (3%). On average, almost a third of the reports is verified.

Overall, there is a proliferation of types of reports, with companies using their websites more than before. An example of the latter is the inclusion of the summary of an assurance statement in the report, with reference to the company website for the full version. Some companies issue several reports, for example, a corporate social responsibility report plus an health, safety and the environment report; or information in their annual report plus a HSE report; or even an environmental and a sustainability report, sometimes added with information on their websites. A few companies (continue to) publish separate social and environmental reports.

This development shows that there are clearly different views on what the most appropriate way of communicating is, which is reflected in divergent forms, titles and contents of reports. This, however, also increases complexity for stakeholders since not all companies are clear about what kind of reports they have, and with which purpose. One might even suggest that some companies just ‘go with the flow’, and publish a particular type of report without having thought through what the exact purpose and target group would be, and how this fits into in a clear and easily understandable approach for (particular groups of) stakeholders. In their reports, companies pay much attention to stakeholders, mentioning their key stakeholders (which usually includes shareholders/investors), a stakeholder dialogue and getting feedback from them, also in the selection of reporting topics. This does not mean, however, that this is a structured or systematic approach to stakeholder engagement; the 2005 survey showed that this is much less common. It is also difficult for companies because of the diverse needs, expectations and interests of the whole range of stakeholder groups (including shareholders/investors).

A final interesting trend is increasing attention to governance and legal issues. The majority of the reports in the 2005 survey (61%) had a section on corporate governance (this obviously applies to the annual reports, but also to many separate sustainability reports). This is a large difference compared to 2002. It must be noted that many of the corporate governance sections just summarise the ‘regular’, general governance topics (i.e. not at all related to sustainability, or just very marginally in one sentence related to transparency and accountability). There are, however, also interesting examples where companies already link it to sustainability. How sustainability is structured and who is finally responsible for it is included in nearly a third of the reports. Interesting is that some companies have cautionary statements about the nature of the information in the sustainability report (for example, a note on forward-looking statements).

Attention to governance and legal aspects reflects the developments after the Enron, Ahold, Parmalat, WorldCom and other affairs, and the rules and regulations adopted subsequently. These scandals have also had an impact on the codes of ethics. Not only do most companies (67%) refer to (or include) their code of ethics (code of conduct, business principles), but many have also revised their code recently and explicitly mention this. Moreover, 29% of the reports include information on a whistleblower, ombudsman or other independent function.

It is interesting to note that a number of aspects related to corporate governance are mentioned as frequently by Japanese companies as by European and US companies, or even more. This applies to the inclusion of a corporate governance section in the sustainability report (Japan: 64%; Europe: 70%; US: 46%); reference to codes of ethics (73%, 71% and 63% respectively); and the existence of a whistleblower mechanism (52%, 20% and 31%). Ethics, accounting and internal control scandals in Japan in recent years have certainly played a role in this regard; some Japanese companies also refer to their own deficiencies in the past.

It can be expected that the topic of corporate governance in relation to sustainability will become more important, also in reporting, in coming years, in which investor pressure can be expected to play a role. In the financial sector itself, where sustainability reporting has taken off recently, there are interesting developments as well, as the final section will briefly indicate.

Developments in the financial sector

Behind the overall increase in sustainability reporting in the financial sector, as mentioned above, lies a strong difference per region. European financial companies (especially those from the UK, the Netherlands and Switzerland) are very active, their US and Japanese counterparts considerably less. Notable is also that among these large banks and insurance companies, verification is an exclusively European phenomenon (with percentages similar to the overall one); no financial companies from other regions have done the same so far.

What is interesting with regard to growing reporting in the financial sector, is that these companies have undergone a tremendous ‘mind shift’ in the past decade. They initially perceived the environment largely in a process-oriented manner, focusing on their own relatively small footprint in terms of energy, water, transport and material usage. Over time, however, pressurised by NGOs on international project finance in particular, they started to realise that more attention to their products was required, and to the environmental, social and also economic (poverty/development) implications of their core activities. Some banks and insurance companies also discovered, relatively early, the risks (and market opportunities) related to climate change.

This movement away from a more reactive process approach has been accompanied by increased transparency and accountability, and international cooperation, for example, through the UNEP Finance Initiative, and with the GRI to develop a financial services sector supplement to the guidelines. It has led to a substantial growth in the number of sustainability reports published by banks and, to a somewhat lesser extent, insurance companies. Reporting (and activities) have so far merely concentrated on the following elements of the financial sector’s portfolio.

Regarding project financing worldwide, this has involved the Equator Principles, an industry-wide initiative to determine and manage environmental and social risks (and level the playing field) in the case of larger projects. In credits, micro-credit lending, which used to be largely outside the scope of large banks, is currently receiving more attention. This is part of a broader movement which sees access to capital for small entrepreneurs as important for reducing poverty and furthering development. A third, and more well-known field is sustainable asset management, which has traditionally been most important in the US, but is increasing in Asia and Europe as well. Apart from these three areas, sustainability in relation to mainstream asset management, retail banking, credits and insurance has received far less attention. This means that, overall, sustainability will continue to present challenges for the financial sector, also because of ongoing stakeholder (NGO) pressure. The fact, however, that sustainability reporting by financial companies themselves is increasing may also stimulate further disclosure by companies in other sectors (expecially their clients) as the financial sector will start to perceive it as normal business practice and request such information.

Concluding remarks

In the period of almost a decade in which I have investigated environmental and, later, sustainability (also labelled corporate social responsibility) reporting, large changes have taken place. This includes the ongoing strong growth in the number of reports published (recently also in the form of sustainability sections in annual reports), especially by the largest multinational companies. The widened reporting scope and contents, from environmental (or HSE) to social and also some financial information can be seen throughout. It seems to be a considerable challenge still in Japan, where environmental reporting and accounting has rapidly taken root in the 21st century, but where a real broadening to include (international) social issues is much more in the initial stages than in Europe and the US. The environmental accounting approach, on the other hand, is less common in Europe and the US.

In addition to Japan, France has also seen considerable increases in reporting, stimulated by government legislation on the inclusion of environmental and social information in annual reports. While Scandinavian companies were amongst the first that adopted reporting to a considerable extent, this first-mover advantage in terms of numbers has disappeared. The Netherlands has been part of the overall movement towards increased reporting and verification, with some companies helping to set trends, while others merely follow. US companies were very active in the beginning, but this lead later declined due to fear of litigation and a cost-compliance orientation, which has reduced eagerness to report (and verify). In recent years, UK companies have consistently been in the front, also in terms in verification.

While industrial, more polluting companies have traditionally been most active in reporting, sustainability reporting in the financial sector has increased rapidly in the past few years. This has particularly been the case in Europe; much less in Japan and US. Sustainability reporting by banks, and to a lesser extent insurance companies, reflects their move away from their own internal ‘footprint’ to a first consideration of the environmental, social and economic dimensions of their core activities (risks and opportunities related to climate change, micro credits, project financing, sustainable asset management). In addition to financial and legal issues, corporate governance in relation to sustainability is a new phenomenon in reporting, in all sectors, and across all countries (although cultural perceptions of the meaning of governance and compliance differ considerably). This is likely to increase in the next few years, also under the influence from investors. Proliferation of reporting, in different formats and types, using a range of sources (paper and electronic), implies a multiplication of data available. While laudable in itself, it is not always certain that this also increases relevance and informativeness to readers; instead, in some cases, it may have become even more difficult. For companies, standardisation and the use of guidelines has worked to some extent, but it can also make it more complicated because of increasing requirements (lists of performance indicators and key aspects) and expectations, and the amount of work involved in collecting, compiling and communicating. How to make sense of it all is thus a key question, also for investors, in what no doubt will continue to be a dynamic field.

Notes

- The author has been involved in the 1999, 2002 and 2005 surveys, with special responsibility for the research on the Fortune Global 250 companies.

References

- Dierkes, M. and Antal, A.B. (1986). Whither corporate social reporting: is it time to legislate? California Management Review, XXVIII(3), 106-21.

- Epstein, M., Flamholtz, E. and McDonough, J.J. (1976). Corporate social accounting in the United States of America: state of the art and future prospects. Accounting, Organizations and Society, 1(1), 23-42.

- Global Reporting Initiative (2002). Sustainability reporting guidelines. Boston: GRI.

- Haigh, M. (2005). What counts in social investment: evidence from an international survey. Advances in Public Interest Accounting Journal, forthcoming.

- Kolk, A. (2003). Trends in sustainability reporting by the Fortune Global 250’. Business Strategy and the Environment, 12(5), 279-91.

- Kolk, A. (2005). Environmental reporting by multinationals from the Triad: convergence or divergence? Management International Review, 45, 2005/1, 145-166.

- KPMG (1993). KPMG International survey of environmental reporting, n.p. KPMG (1997), International survey of environmental reporting 1996. Stockholm

- KPMG (1999), KPMG International survey of environmental reporting 1999. The Hague

- KPMG (2002). KPMG International survey of corporate sustainability reporting 2002. De Meern.

- KPMG (2005). KPMG International survey of corporate responsibility reporting 2005. Amsterdam.

- Pleon (2005). Accounting for good: the global stakeholder report 2005. Amsterdam/Bonn.

- Sustainability/UNEP (1998). The non-reporting report. London.

- US Department of Commerce, 1979. Corporate social reporting in the United States and Western Europe. Washington: Task Force on Corporate Social Performance.

in VBA Journaal door Ans Kolk