INTRODUCTION

Value investing in equity is a popular way to gain outperformance. Once popularised by Benjamin Graham and currently a firm building block of smart beta strategies, the idea isto reap the Value factor premium by investing in cheap companies with low valuation ratios per share (Book Value, FreeCash Flow, Earnings, Sales). Academic research and asset managers have shown that this approach has historically led to better returns than Growth stocks and the Market index. But not for the last 13 years! (Figure 1).

Value investing in equity is a popular way to gain outperformance. Once popularised by Benjamin Graham and currently a firm building block of smart beta strategies, the idea isto reap the Value factor premium by investing in cheap companies with low valuation ratios per share (Book Value, FreeCash Flow, Earnings, Sales). Academic research and asset managers have shown that this approach has historically led to better returns than Growth stocks and the Market index. But not for the last 13 years! (Figure 1).

QUANT & FUNDAMENTAL ANALYSIS EXPLAIN THE OUTPERFORMANCE OF GROWTH

The 13 year underperformance of Value is troublesome for Value managers and painful for their clients. Equity managers emphasise how rare this streak of underperformance is. Based on historical data, the chance is less than 5% if you run a Monte Carlo simulation. Quant managers tend to offer no other explanation than ‘the market has become irrational’. That is unsatisfactory; this mystery requires a cross examination of both views.

The research starts with a description of the Value premium and the historical drivers of outperformance. The period of underperformance is subsequently examined. Quant analysis explains the outperformance of Growth stocks by their improved profitability over Value, whilst fundamental analysis explains that Growth stocks benefitted most from the declining interest rates due to their long duration cash flows.

THE VALUE PREMIUM

THE VALUE PREMIUM

The Fama & French (F&F) publication in 1992 provided global and long-term evidence for the Value and Size factors. They sorted equity universes on cheapness and ranked the 30% cheapest bucket Value, the 40% middle as Market and the 30% most expensive bucket Growth. Value did outperform Growth, on average by 4% annually. Thus, Value became a factor with a premium.

There are two valid academic interpretations for Value’s outperformance. The behavioural side says that investors as a group overestimate recent profitability. The financial market is too pessimistic for Value stocks and too optimistic for Growth stocks, whereas in reality their profitability reverts to the mean. The efficient market proponents point to a rationale in cheaper priced Value stocks. These stocks are riskier and should be compensated with higher return. Riskier with cyclical revenue, leverage, more fixed assets, more competition and a higher equity beta. Both explanations reason that Value is out of favour among investors.

F&F break down the 4% outperformance of Value versus Growth into a direct Dividend source and three indirect sources of Capital Gain. F&F updated their findings in 2006, with data starting from 1927. First, dividend was annually 1.3% higher for the Value bucket, contributing to 1/3 of the outperformance versus Growth stocks. The other 2/3 outperformance is in Capital Gain:

- Relative growth in book equity due to profitability (retained earnings). Growth stocks have on average 7% higher growth, a disadvantage for Value.

- Converging valuation ratios due to mean reverting profitability. This is also called migration, an average 11% benefit when Value stocks promote out of the low PE bucket to Market or Growth.

- Drift in valuation ratios, or revaluation of the whole style bucket. For the Value and Growth styles, the long term PE drift was the same. On average zero difference.

INVESTIGATING THE 2007 – 2020 UNDERPERFORMANCE

INVESTIGATING THE 2007 – 2020 UNDERPERFORMANCE

Performance attribution helps to empirically pinpoint the four F&F sources of return one by one. Ideally, combined with an economic explanation. The underperformance from 2007-2020 is the longest drawdown of the Value factor. For this investigation, these 13 years make a good long horizon, which minimises short-term noise. Copeland et al. (2000) says: ‘Over horizons of at least 15 years, total returns to shareholders will be linked to earnings because earnings growth will track cash flow and returns to capital.’

Asset managers deliver lots of data, but their results are not always comparable due to different benchmarks or portfolio construction models. Ultimately, some useful Value minus Growth historical information was distilled for the US market. F&F data are compared with findings of Research Affiliates, pre and post 2007:

The first three components are structural. They have a known sign, historically and by definition. 1. dividend (+) of the Value bucket will be larger than the dividend of the Growth bucket 2a. profitability (-) is much larger for Growth. 2b. migration (+) the converging PE ratios are always beneficial for the Value bucket. The cyclical component 2c. revaluation is long term zero but deviates in the short term.

The balance of these structural components was often in favour of Value stocks, but not during the last 13 years. Growth outperformance over 2007-2020 versus Value outperformance over 1963-2006 is explained by: improved Profitability of Growth over Value, less Migration of Value, and Revaluation in favour of Growth. More about these three effects below.

2A. PROFITABILITY

Quant research from Arnott et al. (p.26) brings additional data in scope regarding profitability.

Quant research from Arnott et al. (p.26) brings additional data in scope regarding profitability.

The economy over the period of 2007-2020 is characterised by secular stagnation, a lower GDP growth and lower interest rates than in the preceding decades. Regarding listed US companies, it translated into lower RoE and lower Sales Growth. For RoE, Growth stocks were 3 times more profitable pre-2007 than Value, rising to 4 times post-2007 (see bold in the table). For Sales Growth, the ratio has grown from 2.5 times pre-2007 to 4 times post-2007.

2B. MIGRATION

2B. MIGRATION

The largest component of Value’s outperformance has been migration. A promotion to the Market or Growth bucket is an indirect reward of improving profitability. However, in an environment of secular stagnation, Value stocks are more likely to remain in their bucket. Post-2007, many defaults were only averted because of ultra-low interest rates by the Central Bank. Creative destruction has been delayed, some Value companies have become eternal Value or Zombie companies. Another reason why migration is slowing is due to several Big Tech companies. These monopolistic Growth stocks have made it harder for new, smaller companies to gain market share. Finally, Asness et al. (2020) point to more stable valuations, partly driven by market participants’ increased sophistication, narrowing the relative valuations of most stocks. These three aspects make a smaller migration effect probable.

2C. REVALUATION

2C. REVALUATION

Over a short horizon, the PE drift of Growth and Value buckets is driven by investor trends or preferences. In particular, the multi-year Internet hype stands out. Eventually the market corrects and the revaluation effect is expected to be zero for the long term. However, over the past 13 years, this effect was annually -6.6%, leading to underperformance of Value.

Growth stocks benefitted from better profitability (and quality) by rising investor demand (rising PE ratio), an indirect positive revaluation, while the opposite applies to Value stocks. They are riskier in secular stagnation and faced falling demand (falling PE ratio).

GROWTH STOCKS HAD IMPROVED PROFITABILITY OVER VALUE

Revaluation is directly linked to interest rates. Growth has a higher interest rate sensitivity than Value, because of the longer duration cash flows of Growth stocks. Fundamental analysis uses Discounted Cash Flow (DCF) modelling in pursuit of the intrinsic value of securities. This is a strong theoretical and practical model. Copeland et al. say: ‘DCF valuations are highly sensitive to small changes in assumptions about the future. The sensitivity is also highest when interest rates are low’. Although interest rates are in decline for several decades, a DCF sensitivity is especially relevant with current record low interest rates.

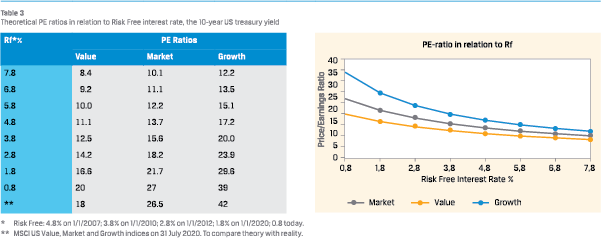

To learn about interest rate sensitivity and resulting changes in PE multiples, I made standard DCF calculations with three hypothetical stocks: Value, Market and Growth. They differ only in growth estimates of free cash flow, ranging between 0% and 6%. The Equity Risk Premium is 5%, the Credit Spread is 1%, the Tax Rate is 25%. The DCF results are an illustration of relative PE multiples given the interest rate (change). They are roughly in line with observed markets. See the current MSCI US indices and in the eighties when the market PE rose above 10 on the back of lower interest rates.

Interest rate sensitivity is clearly visible; higher PE multiples result from lower rates and the effect is accelerating. A new insight is how the PE sensitivities differ in Value, Market and Growth buckets. Price returns are deducted from these revaluation effects.

Interest rate sensitivity is visible again and naturally accelerating with lower rates. When risk-free rates decline from 7.8 to 6.8%, the price return ceteris paribus for Market is 10%. US risk free rate declined pre- and post-Corona from 1.8 to 0.8%, lifting the theoretical PE ratio of the Market by a whopping 25% to 27x.

For every interest rate, the revaluation effect is stronger for Growth than Market, and less for Value than Market. This is directly linked to cash flow duration. Growth stocks’ free cash flows are further in the future, implying they have higher duration. Thus, the Growth bucket benefits (much) more than the Value bucket from falling risk free interest rates. Over the period 2007 to March 2020, the risk free interest rate declined from 4.8 to 0.8%. This 4% fall has attributed annually 3.8% to Growth outperformance versus Value. And more recently, more impressive: the revaluation effect pre- and post-coronavirus of 1% interest rate decline is a 12% return advantage for Growth versus Value stocks in just a few months!

The long-term causality between interest rates and equity valuation is generally known. Since 1960, lower bond yields explain lower earnings yields. Because earnings yield is the inverse of a PE≈ratio, we can also say that lower bond yields explain higher PE ratios. Never before was the sensitivity to interest rates so high, because interest rates are so low. Recently, more than a dozen well-known asset managers have pointed at the lower interest rate in a DCF context for Value’s underperformance.

GROWTH STOCKS BENEFITTED MOST FROM DECLINING INTEREST RATES

AQR’s Maloney and Moskowitz (M&M) performed statistical analysis on US equity returns and 10-year yield changes. When the interest rate is low, there is a significant and economically meaningful correlation in a change of interest rate. Especially over the horizon 2017-2020, t-statistics jump significantly. They confirm strong causality on Value-minusGrowth buckets. When interest rates declined to the lowest level ever, Growth did outperform meaningful.

One could argue that the risk-free interest rate is artificially low, caused by Central Bank intervention and not determined by a free market. Is it fair to calculate with such a low rate then? Yes, currently it is the observed and traded interest rate. The reality is that Central Banks will keep rates lower for longer. It is the new normal, it is part of secular stagnation. Central Banks will help their hefty indebted US and European governments with low risk free interest rates and buying government debt with freshly printed money. When inflation rises, debt becomes more sustainable. Thus, Central Banks will not suppress inflation immediately. On 27 August, Jerome Powell confirmed this with a new inflation target of symmetric bandwidths around 2%.

ATTRIBUTION

The findings of quant information and the additional DCFinsights explain the Value-minus-Growth performance. Within the framework of Fama & French, both point to an average annual 11.6% difference in return, when comparing the period before 2007 and the period thereafter. In column two and three, Research Affiliates (RA) measured the Value-minusGrowth performance. In column four and five, DCF attributes the changes in a direct and indirect effect.

The findings of quant information and the additional DCFinsights explain the Value-minus-Growth performance. Within the framework of Fama & French, both point to an average annual 11.6% difference in return, when comparing the period before 2007 and the period thereafter. In column two and three, Research Affiliates (RA) measured the Value-minusGrowth performance. In column four and five, DCF attributes the changes in a direct and indirect effect.

The total outperformance of Value vs Growth is 7.3% pre-2007, turning into 4.3% underperformance post-2007. This negative difference in return of 11.6% annually is exactly explained in the ‘Change’ columns. The direct effect of improved Profitability is –3%, while the indirect effects are –2% on Migration and –2.8% on Revaluation. The direct effect of interest rate decline is –3.8% on Revaluation, again in favour of Growth (this was earlier explained via table 4).

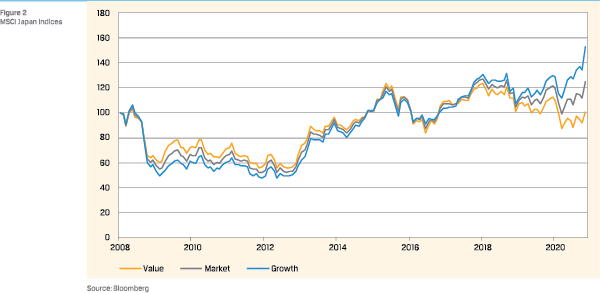

VALUE IN JAPAN

In Japan, the equity performance is less (distinct) than in the US. But the striking rise of equity in general, and Growth stocks specifically, since 2019 is visible. At that time, the 10-year Japanese government bond yield became more negative than ever before.

OUTLOOK FOR VALUE

OUTLOOK FOR VALUE

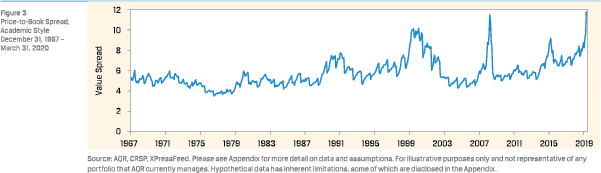

The difference in Price/Book of US Growth versus Value is on average 5.4. In the eighties, with high interest rates, high inflation, weak economic growth, the spread was lowest at 4. Remarkably, the figure was also low at the end of 2006. Value seemed expensive and/or Growth cheap. Ironically, the publication of the Value factor by F&F in 2006 coincidences with the start of Value’s underperformance versus Growth stocks.

Today, with a low interest rate, low inflation and decent profit growth, the Price/Book spread is highest at 10. The spread will probably come down automatically when new estimates are fed into the consensus figures. ‘Price’ has immediately adapted in the COVID-19 crisis, whereas ‘Book Value’ is a lagging indicator. On average, Growth stocks will increase their Book Value, Sales and Earnings. In particular, tech is Labor Light and Asset Light without machinery, factories or inventories. So, they are very flexible in terms of adapting, which is a great advantage, particularly in a crisis. The Value stocks will on average report declines, driven by the sectors Energy, Financials, Real Estate and by industries like Airline, Entertainment and Hotels. However, the spread probably remains elevated, pointing to an attractive entry point for Value.

That is even after correcting for incomplete treatment of ‘intangibles’, assets that are not physical in nature and that are hard to define or measure. The traditional Price/Book ratio has difficulties capturing real asset growth because intangibles become much more important in an increasingly service-based economy. In a few decades, intangibles have evolved from a supporting asset into a major consideration for investors. Last year, they made up the majority of all enterprise value on the S&P 500. The FAMAG shares particularly stand out: Facebook, Amazon, Microsoft, Apple and Google.

That is even after correcting for incomplete treatment of ‘intangibles’, assets that are not physical in nature and that are hard to define or measure. The traditional Price/Book ratio has difficulties capturing real asset growth because intangibles become much more important in an increasingly service-based economy. In a few decades, intangibles have evolved from a supporting asset into a major consideration for investors. Last year, they made up the majority of all enterprise value on the S&P 500. The FAMAG shares particularly stand out: Facebook, Amazon, Microsoft, Apple and Google.

Investors agree that more transparency would be beneficial to their assessment of intangible assets. In the absence of robust reporting, fundamental analysts are well equipped to understand intangible asset values due to their access to management, relationships with key opinion leaders and deep industry expertise. Quant managers had to redesign Price/Book value metrics to capture intangibles as part of a company’s capital.

CONCLUSIONS

Quant and fundamental research are complementary and this combination leads to new insights. The outperformance of Growth versus Value over the last 13+ years is exceptional. Firstly, quant data showed the improved profitability of Growth over Value stocks. Secondly, DCF-analysis explains that Growth stocks benefitted most from the decline in riskfree interest rates.

On Price/Book and other Value Factors, Growth is expensive versus long-term averages. The idea of mean reversion is attractive. However, Price/Book and other quant measures can be improved to approximate the value of equity, especially of Growth stocks. The migration effect will probably be smaller going forward. Besides, for Value to outperform Growth it is important that risk-free interest rates do not decline further.

Longer term we can restrain COVID-19 and will develop our economies in a sustainable way. Say 2% GDP growth and 2% inflation. A risk free debtor like the US government has to compensate investors only for inflation. Consequently, US 10-year interest rates will slowly rise to 2%. Combined with decent company profits, there is upside in Value stocks and the Value Factor.

References

- Arnott, R.C., 2020, Reports of value’s death may be greatly exaggerated. Research Affiliates

- Asness. C., May 2020, Is (Systematic) Value Investing Dead? AQR

- Copeland, T., et al., 2000, Measuring and managing the value of companies. Wiley

- Fama, E.F. & K.R. French, 2007, The Anatomy of Value and Growth Stock Returns. Financial Analysts Journal, Volume 63, Issue 6, p. 44-54.

- Ilmanen, A., 2011, Expected returns. An investor’s guide to harvesting market rewards. Wiley

- Maloney T. and T. J. Moskowitz, May 2020, Value and Interest Rates: Are Rates to Blame for Value’s Torments? AQR

Note

- The views expressed in this paper are his own. The author thanks Kiemthin Tjong Tjin Joe for his valuable ideas and the VBA Journaal for useful remarks.

in VBA Journaal door Jeroen Kakebeeke