OVERVIEW OF KEY CHANGES IMPACTING INVESTORS’ BEHAVIOUR TOWARDS 2020

In recent years the question of benchmark selection is receiving more and more attention from various groups of stakeholders. Almost 10 years ago regulators within and beyond European Union started to conduct investigations on manipulations with LIBOR and other benchmarks. Jurisdictions from around the world have concluded that benchmarks directly affect the value of the financial instruments and other contracts which are referenced to them.

Similarly, European regulators have been concerned about securing market confidence and since March 2011 took steps to strictly regulate the benchmarks industry in the Union. As a result, by January 2018 (with some transitional provisions valid until 2020) the European Benchmark Regulation EU 2016/1011, also commonly known as BMR, has started to be generally applied and changed the rules of the game for benchmark administrators. As a result, various groups of investors will find themselves affected as their financial contracts may continue to have references to benchmarks, use of which may become illegal from 2020 and result in potential financial penalties for its contractual parties. EU Member States are gradually going to see the impact of BMR in effect. The transitional period of 2 years expiring in 2020 is nearing to its end and from 2020 onwards it will be no longer legal to continue use of unregistered or third country benchmarks in contracts.

Similarly, European regulators have been concerned about securing market confidence and since March 2011 took steps to strictly regulate the benchmarks industry in the Union. As a result, by January 2018 (with some transitional provisions valid until 2020) the European Benchmark Regulation EU 2016/1011, also commonly known as BMR, has started to be generally applied and changed the rules of the game for benchmark administrators. As a result, various groups of investors will find themselves affected as their financial contracts may continue to have references to benchmarks, use of which may become illegal from 2020 and result in potential financial penalties for its contractual parties. EU Member States are gradually going to see the impact of BMR in effect. The transitional period of 2 years expiring in 2020 is nearing to its end and from 2020 onwards it will be no longer legal to continue use of unregistered or third country benchmarks in contracts.

This Article aims to spread awareness to various profiles of investors, informing them about the current benchmark industry market and preparing these investor groups for changes stipulated by BMR. This article emphasises on current market position of benchmark providers and translates which actions or possible cost allocations may be anticipated by 2020. This should prepare investors, banks and other relevant financial institutions to diminish the degree of uncertainty, allowing to take timely action by parties to either timely divest, or seek to amend financial contracts, especially those containing references to potentially unauthorized benchmarks.

DEFINITION OF BENCHMARK

There are several contexts within which the definition of benchmark may be understood. This article focuses on definitions of index and benchmark as contained in Article 3 of the BMR, where an index is defined as any figure, on the basis of the value of one or more underlying assets or prices. In cases when an index is used as a reference price for a financial instrument or contracts it becomes a benchmark, which is why benchmark can be any index by reference to which the amount payable under a financial instrument or a financial contract is determined. Underlying assets or prices referenced in benchmarks can include equities (e.g. the FTSE 100 index), bonds (e.g. NASDAQ OMX fixed income), interest rates (e.g. EONIA, EURIBOR or LIBOR), or commodities such as agricultural products (e.g. cocoa LIFFE London), metals (e.g. Gold COMEX) or oil (e.g.Brent oil ICE).

TYPES OF BENCHMARKS

New regime of BMR covers its different types from interest rate to commodity and regulated data benchmarks. Also it distinguishes between critical, significant and non-significant benchmarks. EONIA, EURIBOR and LIBOR have been deemed critical.

REGULATORY PURPOSE

Benchmark methodologies used by administrators differ greatly. European Securities and Market Authority, known as ESMA, has been assigned to coordinate the supervision of benchmark administrators. The primary purpose of this new regime is believed to improve governance and controls over the benchmark process, as well as improve quality of input data and methodologies used by benchmark administrators. Last but not least regulatory changes are introduced under the motto of protection of consumers and investors through delivering greater transparency. Will this transparency endanger the freedom of choice of benchmarks under contract and remain as beneficial to investors in the same way as to the regulators?

FEASIBILITY OF REGULATION REQUIREMENTS IMPLEMENTATION BY THE ADMINISTRATORS

Administrators might not have access to all the data that they are required to provide from 2020 by the BMR. One of the problematic examples refers to provision of records of substantial exposures of individual traders or trading desks to benchmark related instruments. This is not something administrators would generally know. Those benchmarks would either struggle to comply with the regulation or significantly increase internal costs to comply. In any case, it is almost a certainty that the returns for benchmark administrators would become much lower, where forthcoming costs might consume a large portion of their anticipated revenues.

Depending on national jurisdictions benchmark administrators may be unaware that their index is being used as a reference for a financial instrument. This may happen in situations where the users and benchmark administrator are located in different Member States. The regime imposed by BMR, will make sure that parties are informed pertaining to use of a benchmark in a financial instrument, and central coordinating authority (ESMA) will from now on notify its registered benchmark administrators. This regime has however its challenges as imposed limitations on benchmark selection will limit the freedom of investors to use any benchmark they deem fit for their financial contracts. Are there any alternatives for investors to consider?

BENCHMARK INDUSTRY MARKET

To understand the alternatives and competition within industry one would have to have a clear picture of the benchmark industry market. The total size of the benchmark industry remains rather mysterious. Even ESMA is not disclosing its exact size as there are no data sources that would sufficiently report on benchmark universe to make an exact statement. Despite it being hard to estimate an exact size of the industry and exact amount of benchmark administrators, with the introduction of the new BMR regime ESMA will know exactly what the size of the authorised market is and will control its usage. Authorised benchmarks represent only a fraction of the total market industry available at the moment for investors’ choice, where an approximate value of the current benchmark industry market size can be ascertained based on 3 examples discussed below.

To understand the alternatives and competition within industry one would have to have a clear picture of the benchmark industry market. The total size of the benchmark industry remains rather mysterious. Even ESMA is not disclosing its exact size as there are no data sources that would sufficiently report on benchmark universe to make an exact statement. Despite it being hard to estimate an exact size of the industry and exact amount of benchmark administrators, with the introduction of the new BMR regime ESMA will know exactly what the size of the authorised market is and will control its usage. Authorised benchmarks represent only a fraction of the total market industry available at the moment for investors’ choice, where an approximate value of the current benchmark industry market size can be ascertained based on 3 examples discussed below.

EXPENSES LINKED WITH THE IMPLEMENTATION OF NEW REGIME CAN BE SIGNIFICANT

First of all, European Commission via its impact assessment report has managed to obtain an estimate of not only the size of the benchmark industry but also its total revenues, where in their opinion they claim that benchmark administrators from all over the world are generating around EUR 2 billion in revenues. The amount of such revenues fades in comparison with Commission’s overall perception of the size of the market industry to be impacted by regulatory changes, which they believe to be at more than EUR 1,000 trillion. This is huge.

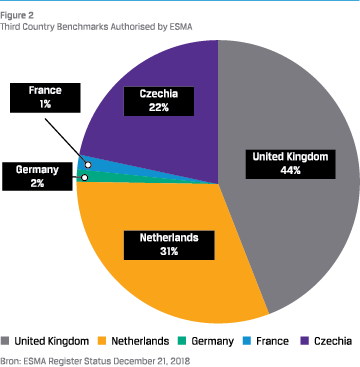

Second, various sources suggest that there are around 170,000 benchmarks that are currently being deployed in EU and not less than 100 administrators, where their claims are that 50% of those are regulated markets and several others are stock exchanges based outside the EU. This is an important indicator which should be compared with the current total of authorised (21) benchmark administrators with its 462 third country benchmarks in order to get a clearer picture of how restricted the benchmark selection is becoming for European financial institutions, banks and investors, wishing to have freedom of choice in selecting benchmarks to their financial contracts after 2018-2020.

Second, various sources suggest that there are around 170,000 benchmarks that are currently being deployed in EU and not less than 100 administrators, where their claims are that 50% of those are regulated markets and several others are stock exchanges based outside the EU. This is an important indicator which should be compared with the current total of authorised (21) benchmark administrators with its 462 third country benchmarks in order to get a clearer picture of how restricted the benchmark selection is becoming for European financial institutions, banks and investors, wishing to have freedom of choice in selecting benchmarks to their financial contracts after 2018-2020.

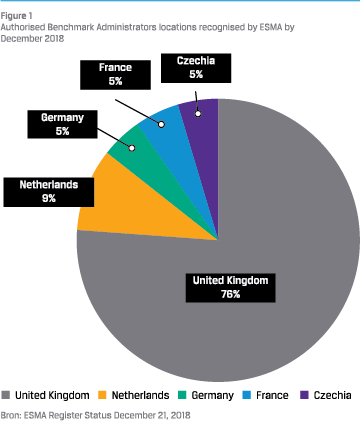

Third, ESMA based on its database register status as of December 2018, has registered a total of 21 authorised benchmark administrators which are predominantly from United Kingdom. Dutch benchmark administrators are on a second place; however, the difference is considerable with Netherlands holding only 9% by amount of authorised administrators, where Germany, France and Czechia conclude the list, each having only one authorised benchmark administrator to date.

However, such a low amount of administrator registrations is largely due to barriers to obtain first registration. Nevertheless, it is not a reason to consider low amount of administrators as a weakness in general. Dutch benchmark market is a leader in its consolidation efforts and has highest amount of registered benchmarks per single administrator by the end of 2018.

AUTHORISED BENCHMARK INDUSTRY PROVIDERS IN THE NETHERLANDS

The Netherlands is represented by 2 authorised benchmark administrators, which are Robeco Indices B.V. and S&P DJI Netherlands B.V. S&P is an absolute leader in the register list by amount of authorised third country benchmarks (102).

Despite having only 2 authorised administrators it is obvious that Dutch benchmark industry market is becoming the most consolidated in terms of acquired authorizations for provision of related third country benchmarks.

The Netherlands is definitely well positioned, since out of a total of 462 authorised related third country benchmarks, The Netherlands alone has already accounted for an authorised amount of 143, representing almost 1/3 or 31% of all third country benchmark registrations within ESMA register by the end of 2018.

VARIOUS GROUPS OF INVESTORS WILL FIND THEMSELVES AFFECTED

Together with uncertainties related to Brexit, as well as significantly lower number of registered benchmarks per each of other 16 UK administrators in ESMA register, it is arguable whether administrators from United Kingdom would be able to apply economies of scale approach to be able to compensate for rising compliance and administration costs. The Dutch benchmark industry market is simply better prepared and has well founded basis to propagate the costs more efficiently. The reasonable question arises on which costs can be expected as a result of this new regime?

COST IMPACT FOR INVESTORS & BENCHMARK ADMINISTRATORS

Expenses linked with the implementation of new regime can be significant. ESMA draft regulatory technical standards provide an indication of which changes new regime will emphasize on. The bearer of such expenses will be primarily benchmark administrators, whereas national authorities, banks and other financial institutions will be feeling the rest of the cost burden.

Initial set up costs will from now on consume largest portion of organization’s expenses, as such will be necessary to establish oversight committees or implement changes to existing committees to stay in conformity with this new legislation.

Overall costs will be increased due to the need to hire experts who will advise and provide expertise to draft new internal procedures required for internal translation and implementation of new rules within your organization. Such costs may vary depending on the status and operational mode of your organization, but in a base case scenario for smaller administrators may be from almost half a million to around EUR 1.3 Million. Ongoing yearly costs are generally not expected to be higher than EUR 0,5 Million. Nevertheless, initial costs for entities administering more than 100 benchmarks will be more significant. They can expect to record their first one off expense in a range from EUR 1,2 Million to EUR 6,4 Million. This amount is likely to represent a fraction of potential future expenses as further regulatory impact on organizations may come from indirect and additional compliance costs.

Implementation of regulatory technical standards will among other things require proper reporting on all the actions of the internal oversight committee and will therefore further lead to organization’s ongoing filing, reporting and monitoring costs as amount of staff hours for this administrative work will have to be increased.

These are already strong reasons that will drive consolidation of the market further as small benchmark administrators may not be in position to sustain committee set ups and ongoing costs if their revenue streams are only from 1 or several insignificant benchmarks that they administer for specific client. What can your institution expect to happen with your financial instrument referring to non-conforming benchmark?

FUTURE OF NON-CONFORMING BENCHMARKS

If your financial instrument is not bound to expire by 2020, without timely actions from benchmark administrators, investors may find themselves left with a contract containing prohibited benchmark as part of its reference. Those entities that will have in-house or external expertise will be able to tackle these changes accordingly and on time, however all investors from now on will have to pay close attention to benchmarks offered under financial instruments. In a situation of pre-selected benchmark before 2018, where an EU registered entity wants to continue use of benchmarks produced by third country administrators such as those from United States, China, Japan, Australia, New Zealand etc., those administrators must apply to be added to the ESMA list of benchmarks and get listed there by the year 2020. There are 3 ways foreseen to legalize benchmark existence beyond year 2020. The allowed procedures are either through Recognition, Equivalence or Endorsement as stipulated by Articles 30-34 of the BMR.

CONCLUSIONS AND OUTLOOK TO 2020

The barriers for entry as authorised benchmark administrator are very high. Obtaining a first time registration becomes a very cumbersome and more importantly costly business endeavour. It may discourage overseas administrators to apply for registration, unless they are dealing with registration of batches of benchmarks.

Regulatory changes which require significant degree of resources to be allocated to implementation within your own organization should generally be perceived rather sceptically. Only larger entities will be able to mitigate the effect of regulatory changes by applying economies of scale approach when registering whole batches of benchmarks. This will allow to propagate the costs over various income streams of the benchmarks and thus resulting in cost savings. Only benchmarks or indices provided by an approved administrator or by a central bank will from now on onwards and no later than by 2020 be allowed to be used within the EU.

Despite its noble objectives BMR is perceived to pose a lot of uncertainties, extra costs and complications for not only benchmark administrators, but also financial institutions, banks and investors who are already having “exotic” or third country benchmarks as part of their portfolio of contractual agreements. Smaller investors and risk averse institutions would simply avoid any non-vanilla contract arrangements and proceed to divest if they cannot agree on a substitute reference for any financial instrument with unauthorised benchmark. Such response triggered by the BMR will be understandable as parties would want to avoid any potential fines to be imposed on their organizations. This regime will also limit the investment flows and revenues to third country benchmark administrators. Remaining authorised benchmarks will be thoroughly monitored. Some benchmarks may become unsustainable due to cost burden, where parties will have to renegotiate terms of their financial instrument to figure out a proper substitute reference.

CONTRACTUAL PARTIES WITHIN EUROPEAN UNION MAY FIND THEIR FREEDOM… RESTRICTED

As well as the impacts on administrators, detrimental impacts will be conveyed to benchmark users. If the compliance costs incurred by administrators are largely passed through to end users in the form of higher fees, users may look at alternate measures. If costs are greater for smaller administrators, then this is likely to lead to further sector consolidation, where smaller market participants will have no other choice but to exit benchmark administration. The only outcome of this will be fewer administrators with more benchmarks approved per administrator. This is already happening, since by the end of 2018 ESMA has already approved more than 100 benchmarks per administrator as the case is for The Netherlands and Czechia. It is arguable whether the new regime is going to benefit investors in the short term as it is likely to force administrators to either exit or deviate from established benchmark products considering an alternative of less well-formulated versions in order for benchmark users to reduce costs to be conveyed by benchmark administrators.

As a result, contractual parties within European Union may find their freedom of benchmark specific selection highly restricted, as it is no longer legal to select any benchmark they wish with transitional provisions on unregistered benchmarks bound to expire by the end of 2019. Their only choice would be either to amend or set up an alternative financial instrument by selecting the reference from authorised list of benchmarks.

The European end user of these benchmarks will therefore be the one who will pay for these changes as benchmark administrators will gradually pass over these compliance costs to benchmark users. This regulation will inevitably further limit the conventional ways of benchmark choice for investors and gradually result in an increase of the price proposition for its end users. Desired transparency is becoming a luxury, which will sooner or later trigger higher fees for every European institution directly or indirectly dealing with benchmarks.

References

- Official Journal of the European Union, 2016, REGULATION (EU) 2016/1011

- Proposal for a REGULATION OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL on indices used as benchmarks in financial instruments and financial contracts, COM/2013/0641 final – 2013/0314 COD

- GRSS Article, Benchmark Administrators running out of time to meet BMR, July 2018

- Commission Staff Working Document Executive Summary of the Impact Assessment Accompanying the Document Proposal for a Regulation of the European Parliament and of the Council on Indices Used as Benchmarks in Financial Instruments and Financial Contracts, SWD/2013/0337

- European Commission Memo, Libor scandal: Amendments to proposed Market Abuselegislation to fight rate-fixing, July 2012

- BlackRock ViewPoint, Best Practices for Better Benchmarks: Recommendations for Financial Benchmark Reform, April. 2018

- Europe Economics Research, Cost-benefit Analysis on Draft Technical Standards relating to the Benchmarks Regulation: Final Report, February 2017

- FCA Financial Conduct Authority, Article, EU Benchmarks Regulation, April 2016, latest version updated September 2018

- Barclays Article, Benchmark reform: transition from IBORs to risk-free rates in euro area, Lundstrom, February 2018

- Financier Worldwide Journal, Reform of Interest Rate Benchmarks, July 2018 Issue

in VBA Journaal door Ernest Hryhoryev