Introduction

The main goal of this research paper is to investigate whether investing in cryptoassets may be attractive for institutional investors. Institutional investors, such as pension funds and endowments, typically have long investment horizons and a high tolerance to risk, making a non-negligible allocation to alternative investments appropriate. Cryptoassets are a new and emerging type of alternative investment, thus it is appropriate for innovative and forward-looking institutional investors to evaluate their merits and to assess their expected return, volatility, and correlation with other assets.

The main goal of this research paper is to investigate whether investing in cryptoassets may be attractive for institutional investors. Institutional investors, such as pension funds and endowments, typically have long investment horizons and a high tolerance to risk, making a non-negligible allocation to alternative investments appropriate. Cryptoassets are a new and emerging type of alternative investment, thus it is appropriate for innovative and forward-looking institutional investors to evaluate their merits and to assess their expected return, volatility, and correlation with other assets.

When estimating forward-looking expected returns, investors must first understand the fundamentals of the asset(s) in question. Section 2 of this paper explores this aspect with respect to cryptoassets. Section 3 attempts to formulate reasonable scenarios for the potential future development of cryptoassets and what the expected returns might be. Lastly, Section 4 builds on Aegon Asset Management’s expertise in asset allocation and utilizes the company`s proprietary asset allocation framework to evaluate the risk-return impact of including cryptoassets in institutional investors’ portfolios.

Based on a range of scenarios the conclusion reached is that the inclusion of cryptoassets in institutional investors` portfolios is not recommended. This outcome is driven by the view that expected returns for cryptoassets are negative in most cases, despite the small probability of making very high returns.

Cryptoassets overview

What cryptoassets are

In order to be able to value an asset, one should understand the fundamentals of the asset in question, i.e. what it is and how it works. For example, the typical investor knows that a bond is a security whose holder is entitled to receive money from its issuer and an equity share represents certain ownership of a company. However, given that cryptoassets are a relatively new asset class, there is little general consensus on what exactly cryptoassets are.

A useful separation of cryptoassets is provided by Burniske et al. (2017). The authors propose the word cryptoasset as the general term for a digital asset which predominantly uses blockchain technology as means to achieve decentralized trust. Within this catch-all term, there are several subvariants.

The first specific type of cryptoassets is cryptocurrencies. Cryptocurrencies are basically digital cash built with open-source technology and decentralized nature. Such cryptocurrencies can conceptually fulfil several functions, namely serving as a unit of exchange, store of value and unit of account. An important point is that cryptocurrencies are not (yet) embraced by nation states or supported by central banks, although this might change in the future.

The second type of cryptoassets is cryptocommodities. These are assets which provision raw digital resources such as compute power, storage capacity, and network bandwidth. A useful analogy is to compare cryptocommodities to actual commodities, such as oil, wheat and copper, which are essentially used as inputs into other products.

Investors in cryptoassets must understand the fundamentals of the asset class

The third type of cryptoassets is cryptotokens. This “sub-asset class” is aimed at provisioning finished digital goods and services (e.g. media, social networks, games etc.) and can be likened to tokens which one can purchase to play billiards at the local pub.

Examples of cryptoassets

Before delving into specific examples of cryptoasset types, it is helpful to make the distinction between the technology infrastructure of a cryptoasset and the native asset used within that infrastructure. For example, Ethereum is the protocol in which ethers can be used as means for payment. Similarly, on the Bitcoin protocol one can make payments using bitcoins. To simplify the notation in this research paper, the name of the blockchain\infrastructure will be used interchangeably with the name of its native cryptoasset.

Cryptocurrencies

The best-known example of a cryptocurrency is, of course, Bitcoin. In order to better understand Bitcoin, it is useful to revisit the general characteristics of money. According to Botev (2018), money (as exemplified by currencies, e.g. coins and banknotes, and electronic money, e.g. deposits in banks) is commonly characterized by at least three functions. These are acting as a medium of exchange (for buying), unit of account (for pricing) and store of value (for saving). Given these characteristics, one can assess how well Bitcoin has managed to fulfil them during its brief history. Chart 1 in Section 4.2 illustrates that over its relatively limited history Bitcoin has been very volatile, arguably weakening a potential claim that it is a stable store of value. In addition, in comparison to what can be purchased with fiat money, people cannot buy many things with Bitcoins. Furthermore, what few things that can be purchased with Bitcoin sometimes incur a hefty transaction (network) fee. For these reasons, Bitcoin do not serve as a very useful as a unit of exchange.

It is possible that Bitcoin might obtain the characteristics of money over time if it becomes more widely accepted and less volatile. Even Christine Lagarde, the IMF Managing Director, acknowledges that cryptocurrencies can be quite useful for countries with weak institutions and unstable national currencies (Lagarde, 2017).

Cryptocommodities

Arguably the second most popular cryptoasset is Ethereum, which is an example of a cryptocommodity. Ethereum is a decentralized world computer upon which globally accessible and uncensored applications can be built. The native asset in the Ethereum network is called Ether and it is used to pay for use of the Ethereum Virtual Machine (EVM). On EVM developers can run smart contracts. These “contracts” are not legal documents, but rather they are software logic written in code similar to “if this-then that”. Developers can then build on the Ethereum network protocols for executing various functions, such as decentralized storage sharing, decentralized prediction markets, and decentralized insurance. Thus, Ethereum enables the building of such projects and from that perspective provides a digital commodity which developers can decide to pay for if they think it is useful.

Cryptotokens

The cryptotokens sub-division is probably the most fluid and underdeveloped. One of the first and very recent examples of a cryptotoken is CryptoKitties, which debuted at the end of 2017. CryptoKitties is a game, running on a blockchain, which allows players to purchase, collect, breed, and sell virtual cats. Each CryptoKitty is supposed to be unique and owned by the user. The value of each CryptoKitty can go up and down depending on the market. As CryptoKitties “live” on the blockchain, they cannot be replicated, taken away, or destroyed. CryptoKitties runs on Ethereum's underlying blockchain network.

Expected return scenarios for cryptoassets

Given the fundamental differences between the general types of cryptoassets as described in Section 2, it makes sense to apply specialized methods for valuing them. In this section examples of two out of the three types, namely Bitcoin (cryptocurrency) and Ethereum (cryptocommodity), are valued. No valuation is undertaken for an example of cryptotokens as their underlying value appears too subjective and speculative for institutional investors at present.

Bitcoin expected return scenarios

One possible way to value Bitcoin would be to look at its market capitalization and compare it to the market sizes of other “things” in the world. For instance, one might compare Bitcoin to gold as both might be considered “store of value” assets in which investors can park their wealth. According to the World Gold Council, the world`s total aboveground gold is approximately 190,000 tones and each year around 3,000 tones are mined. The stock of Bitcoins increases at a rate of approximately 4% per annum and is engineered to slowly decline to zero growth around the year 2140. Assuming Bitcoin takes 10% of the current market value of gold (also keeping in mind that approximately half of the current above-ground gold is in jewellery and Bitcoin cannot serve as jewellery), then the market value of Bitcoin could reach 10% * (190,000 tonnes) * (32,000 oz/ton) * ~ 1,300 $/oz = ~ $800 bn. The current market value of bitcoin is 17 mn Bitcoins * 8,000 $/BTC = ~ $170 bn. Thus, in a very optimistic scenario, Bitcoin could return approximately 500% from its current price.

Another method for valuing Bitcoin is to recognize the principle that a network becomes more valuable as more participants are using it, which is based on Metcalfe's law. Approximating the number of Bitcoin users by the number of active addresses (which is probably a significant overestimation of the number of Bitcoin users), Wheatley et al. (2018) show that a plausible Bitcoin market capitalization at the end of 2018 is in the range between $39-77 bn, which is less than half of its current market value. This points to an overvaluation of Bitcoin and to a potential negative return of up to approximately –80%.

Yet another valuation method is to suggest a price for Bitcoin based on its speculative value. If one postulates that in the future investors would be willing to pay a higher price for Bitcoins, then it might be sensible to buy Bitcoins now expecting future appreciation. However, there would be limits to how much the Bitcoin price can appreciate as the cryptocurrency becomes more and more well known. Lam (2018) quotes research from Barclays bank which likens the popularization of Bitcoin worldwide to a virus: “As more of the population become asset holders, the share of the population available to become new buyers – the potential ‘host’ population – falls, while the share of the population that are potential sellers (‘recoveries’) increases. Eventually, this leads to a plateauing of prices, and progressively, as random shocks to the larger supply population push up the ratio of sellers to buyers, prices begin to fall. That induces speculative selling pressure as price declines are projected forward exponentially.” The conclusion is that the speculative phase of the price of bitcoin is likely in the past, making it unlikely that there would be large positive gains in the future from a speculative point of view.

The methods detailed above for valuing Bitcoins provide an illustration of what the upside and downside risks could be. Estimating expected returns based on these methods is more art than science, and coming up directly with a single pointestimate for an expected return is too simplistic. It is for this reason why we detail three different potential scenarios below.

The inclusion of cryptoassets in institutional investors’ portfolios is not recommended

In the Negative scenario continuous struggles between different Bitcoin stakeholders and frequent forks erode the confidence of Bitcoin investors. Next to that, the general public comes to the realization that Bitcoin cannot be easily used as a means of payment and dump the cryptocurrency in favor of other payment solutions. Given that Bitcoin is considered version 1.0 of cryptocurrencies, it is very likely that cryptocurrencies 2.0, which represent an upgrade from version 1.0, are better and thus will overtake Bitcoin. Thus it is possible that Bitcoin could lose almost all its value if another cryptocurrency becomes the de-facto cryptocurrency payment solution. The probability associated with this scenario is 30% and the expected return consistent with this storyline is similar to Wheatley et al. (2018) at –80%.

In the Neutral scenario Bitcoin continues to function as an alternative, albeit seldom used, means of payment by the average person. As its actual use does not live up to expectations, the value of Bitcoin falls. The speculative bubble seen in 2017 has moderated for the reasons pointed out by Lam (2018). The scope for further price appreciation driven by speculative demand is limited as global awareness of Bitcoin has plateaued. The probability associated with this scenario is 60% and the expected return consistent with this storyline is –30%, reflecting the view of the authors that Bitcoin generally does not justify its current high market capitalization on the basis of its fundamental usefulness.

In the Neutral scenario Bitcoin continues to function as an alternative, albeit seldom used, means of payment by the average person. As its actual use does not live up to expectations, the value of Bitcoin falls. The speculative bubble seen in 2017 has moderated for the reasons pointed out by Lam (2018). The scope for further price appreciation driven by speculative demand is limited as global awareness of Bitcoin has plateaued. The probability associated with this scenario is 60% and the expected return consistent with this storyline is –30%, reflecting the view of the authors that Bitcoin generally does not justify its current high market capitalization on the basis of its fundamental usefulness.

In the Positive scenario Bitcoin gains broad acceptance as a store of value and manages to take a substantial share of the market value of gold. The probability associated with this scenario is 10% and the expected return consistent with this storyline is 500% which implies the low probability that Bitcoin gains wide-spread global usage via, for instance, partially replacing gold.

Ethereum expected return scenarios

Valuing Ethereum is even harder than valuing Bitcoin as Ethereum is a more complicated system than Bitcoin. In Ethereum there are different prices – there is Gas, which is aimed to be the constant cost of network resources, and there is Ether, which is the publically traded token used to pay for computing power on the network. Gas is a unit of account and Ether is the actual token on the Ethereum network. The Gas Price is set by the market equilibrium between users (developers) and network maintainers.

Pfeffer (2017) provides an interesting analysis on the valuation of Ethereum and his logic is mirrored here. In the first quarter of 2018 the approximate amount of Gas used on average per day was approximately 35 bn. Taking an average Gas price of 0.00000004 Ethers, a total amount of 35 bn * 0.00000004 = 1,400 Ethers were spent on calculations daily. Assuming an Ether price of $800, the average daily amount spent is 1,400 * $800 = $1.1 mn, which translates to approximately $400 mn to be spent on calculations in 2018. The current market value of Ethereum is approximately $50 bn (10,000,000 Ethers supply in circulation * $500 per Ether). Thus, there exists a computational resource which users pay $400 mn per year to use and the value of the tokens used to pay for this service is $50 bn. According to Evans (2018), the yearly revenues from cloud computing for the three largest providers (IBM, Amazon and Microsoft) is $60 bn. The market capitalization of the three firms, which very much overestimates the value of the standalone cloud computing businesses, is approximately $1.5 tn in total. Thus, if ones considers the market capitalization to revenue ratio for Ethereum (125 = $50 bn / $400 mn) and for the three tech companies (25 = $1.5 tn / $60 bn), the conclusions is that the Ethereum network is at least 5 times overvalued.

Based on the observations above, and in a similar way as for Bitcoin, possible scenarios and expected returns for Ethereum are given below.

In the Negative scenario the Ethereum network loses its current status as the main smart contracts network and is abandoned by developers, or alternatively there is a fork from the existing Ethereum network to which the current network stakeholders migrate to. The probability associated with this scenario is 30% and the expected return is –95%.

In the Neutral scenario the Ethereum network becomes one of the major networks where decentralized applications are run, but forks, competitor networks, and the already very high Ethereum network value lead to investors selling Ethereum. The probability associated with this scenario is 50% and the expected return consistent with this storyline is –40%.

In the Neutral scenario the Ethereum network becomes one of the major networks where decentralized applications are run, but forks, competitor networks, and the already very high Ethereum network value lead to investors selling Ethereum. The probability associated with this scenario is 50% and the expected return consistent with this storyline is –40%.

In the Positive scenario the Ethereum network becomes one of the major networks on which new, and hitherto unconceived, decentralized applications are run. The probability associated with this scenario is 20% and the expected return consistent with this storyline is 400%.

Expected returns discussion

It is important to stress that the scenarios and returns are very subjective, particularly the Positive scenarios. Nevertheless, they are consistent with the examples and reasoning provided. A number of observations can be made based on the expected returns. First, the returns distributions are positively skewed, i.e. there is a small probability of large positive returns, which is likely what motivates less risk-averse investors to allocate capital to cryptoassets. Also, it is expected that cryptoassets will lose money more than 50% of the time, which might be a reason for risk-averse investors to avoid them. Furthermore, when comparing Ethereum to Bitcoin, Ethereum seems to have better prospects, i.e. a higher weighted-average expected return, which is mostly driven by Ethereum`s potential to become a platform to create new and useful applications on.

Adding cryptocurrencies to institutional investors` portfolios

In this section a study is performed on the effects of adding cryptocurrencies to institutional investors` portfolios.

In this section a study is performed on the effects of adding cryptocurrencies to institutional investors` portfolios.

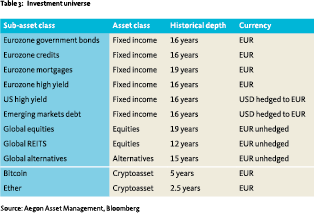

Investment universe

The investment universe for a typical European institutional portfolio – to which cryptoassets will be added – is shown in Table 3:

Volatilities and correlations

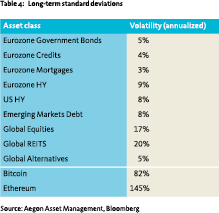

When assessing the attractiveness of an asset class, risk and correlation measures are necessary in addition to expected returns. Using weekly data with the historical depth shown in Table 3, one can compute the realized volatilities (standard deviations) and linear correlations of the asset classes. Tables 4 and 5 show the results:

Several observations can be drawn from Tables 4 and 5:

Several observations can be drawn from Tables 4 and 5:

- The volatility of cryptoassets (82% for Bitcoin and 145% for Ethereum) is significantly higher than the volatility of traditional asset classes.

- Cryptoassets seem to be uncorrelated to traditional asset classes with an average correlation of 5% (the correlation coefficients to most subasset classes are not statistically significantly different from 0).

- The correlation between Bitcoin and Ethereum implies significant co-dependency in their price movements.

- Bitcoin is slightly more correlated – albeit with low significance – to traditional asset classes (7% on average) than Ethereum (5% on average).

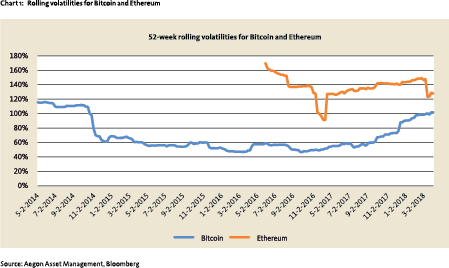

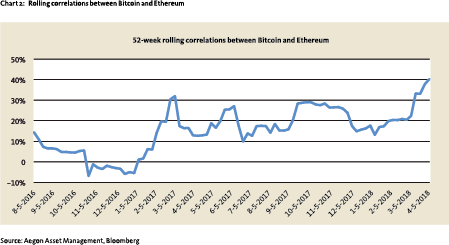

In order to test the stability of the volatility and correlation estimates of the prices of both cryptoassets, these are shown on a historical rolling window basis in Charts 1 and 2:

Chart 1 shows that the volatility of Ethereum has been higher than the volatility of Bitcoin over the historical time period analyzed. Moreover, the volatility of Bitcoin has been steadily increasing since 2015, and especially since the sell-off in February 2018, while the volatility of Ethereum has decreased significantly from 170% to approximately 125%.

Looking at Chart 2, the cryptoassets correlate significantly. The increase in the correlation seen since the beginning of 2017 is likely the result of a growing interest of the general public in Ethereum and hence an inflow of new investors to the crypto space.

Black-Litterman asset allocation framework

Initial set-up

Initial set-up

Aegon Asset Management`s asset allocation engine utilizes a Black-Litterman approach to build optimal portfolios. This framework is used to study the inclusion of cryptoassets in traditional portfolios.

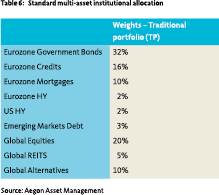

As a first step in the process a balanced portfolio composed of 65% bonds and 35% risky assets is considered. The allocation shown in Table 6 is representative of Aegon Asset Management’s standard multi-asset offering and is used as a proxy for a typical European institutional investor`s portfolio.

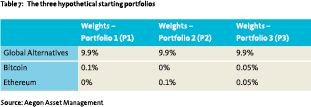

Cryptoassets are considered alternative investments. Assuming that their market capitalization is approximately 1% of the market capitalization of alternatives (BNY Melon 2017), their total neutral weight in an institutional portfolio is kept at 1% of alternatives, which is 0.1% of the total portfolio. Table 7 shows three portfolios representing three different starting points to be used to investigate the relative importance of allocating to cryptoassets in comparison to selecting specific cryptoassets.

Other inputs into the framework, in addition to the information in Tables 7 and 8, are forecasted volatilities (using GARCH models) and historical correlations between the asset classes.

Black-Litterman model: Step 1 – Implied returns

Black-Litterman model: Step 1 – Implied returns

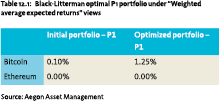

The first step of the Black-Litterman framework provides market–implied returns for a given portfolio. Implied returns represent the implicit market expectations of the performance of different asset classes. These expectations are derived under the assumption that the asset allocation of the initial portfolios (P1, P2 and P3 – as specified in Table 7) is optimal. The implied returns for the cryptoassets are given in Table 8.

For the same amount invested in each cryptoasset (P3), the implied return on Bitcoin is higher than the implied return on Ethereum. This is driven by the small weights of cryptoassets (as shown in Table 7) and the higher correlation of Bitcoin to the traditional asset classes. Given that Ethereum is more volatile than Bitcoin, one might have expected a higher implied return for Ethereum in order to compensate for this higher volatility, but this is not what the model suggests. Another interesting finding is that the implied returns of the traditional asset classes (not shown) are only marginally impacted by the inclusion of cryptoassets due to the low correlation between the cryptos and the rest of the investment universe.

For the same amount invested in each cryptoasset (P3), the implied return on Bitcoin is higher than the implied return on Ethereum. This is driven by the small weights of cryptoassets (as shown in Table 7) and the higher correlation of Bitcoin to the traditional asset classes. Given that Ethereum is more volatile than Bitcoin, one might have expected a higher implied return for Ethereum in order to compensate for this higher volatility, but this is not what the model suggests. Another interesting finding is that the implied returns of the traditional asset classes (not shown) are only marginally impacted by the inclusion of cryptoassets due to the low correlation between the cryptos and the rest of the investment universe.

Most expected returns scenarios forecast negative returns

Black-Litterman model: Step 2 – Including views

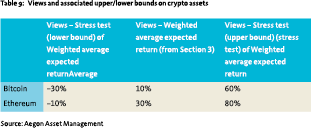

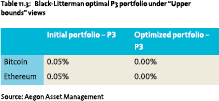

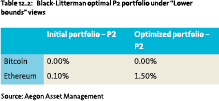

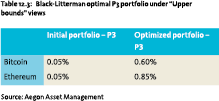

The first step of the Black-Litterman model analyzes a given portfolio from a risk/return perspective and its output is a set of optimal returns. The second step allows investors to blend the implied market returns from the first step with custom expected return views. As such views the long-term expected returns of Aegon Asset Management for the traditional asset classes (Botev 2017) and the weighted average expected returns for the cryptoassets from Section 3 are used. The weighted average expected return estimates for cryptoassets are uncertain, and henceforth lower and upper bound stress test values are used to take account of this uncertainty (Table 9). These stress test values are also used to study what the resulting optimal portfolios (shown in Tables 10, 11 and 12) might look like.

The first step of the Black-Litterman model analyzes a given portfolio from a risk/return perspective and its output is a set of optimal returns. The second step allows investors to blend the implied market returns from the first step with custom expected return views. As such views the long-term expected returns of Aegon Asset Management for the traditional asset classes (Botev 2017) and the weighted average expected returns for the cryptoassets from Section 3 are used. The weighted average expected return estimates for cryptoassets are uncertain, and henceforth lower and upper bound stress test values are used to take account of this uncertainty (Table 9). These stress test values are also used to study what the resulting optimal portfolios (shown in Tables 10, 11 and 12) might look like.

Black-Litterman model: Step 3 – Optimal portfolios

For each view in Table 9, the third and final step of the Black-Litterman framework blends all the inputs (risk, implied returns and views) together and specifies a portfolio that maximizes the expected Sharpe Ratio. The framework is applied to portfolios P1, P2 and P3 as specified in Table 7.

Cryptoassets offer a small possibility of very high returns

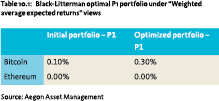

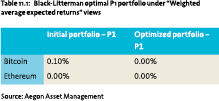

When the weighted average expected returns from Section 3 are used, the optimal portfolios include an allocation to cryptoassets. This allocation results in a higher expected return for the overall optimized portfolio (driven by the positive expected return of cryptoassets) and in a lower volatility (driven by the diversification benefits of cryptoassets) than those of the initial portfolios. Tables 10.1, 10.2 and 10.3 show the results:

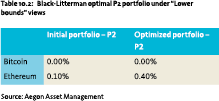

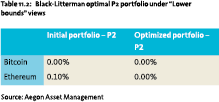

When the lower bounds assumptions are used, the optimal P1, P2 and P3 portfolios would not contain any allocation to cryptoassets. This implies that the negative return expectations in the lower bound stress test overwhelm any positive diversification benefits to the portfolio from including cryptoassets in them. Tables 11.1, 11.2 and 11.3 show the results.

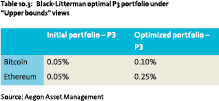

When the upper bounds assumptions are used, the allocation to cryptoassets in the optimal portfolios is relatively high, which can be explained by their high expected return relative to those of the traditional asset classes. This leads to a higher expected return on average for the optimized overall portfolio (up by 0.8% to 2.4%) while maintaining the same level of risk, which significantly improves the expected Sharpe Ratio. Tables 12.1, 12.2 and 12.3 show the results.

A potential allocation to Ethereum should be at least as much as an allocation to Bitcoin

Summary

In conclusion, the low correlation of cryptoassets to traditional asset classes does not compensate enough for negative expected returns of cryptoassets and the Black-Litterman framework would then suggest that they should not be included in institutional portfolios. However, if the expected returns are even marginally positive, then BlackLitterman would suggest a decent allocation to cryptoassets. A strong indirect driver for this conclusion is the low or negative expected returns for traditional asset classes. It is interesting to note that future expected returns for cryptoassets are projected to be negative in the majority of cases. It should also be pointed out that the positive weighted average expected returns from Section 3 are driven by the large (over 400%) returns in the Positive scenarios in Section 3. Given that the returns in the Positive scenario are very difficult to estimate, a cautious institutional investor ought to shun investing in cryptoassets. Lastly, the potential allocation to Ethereum should in all cases be at least as much as the allocation to Bitcoin, driven by the more positive expectations on Ethereum on a relative basis in comparison to Bitcoin.

Note

- Fares Ben Ghachem and Iavor Botev, CFA are both Portfolio Manager multi-asset at Aegon Asset Management.

Literature

- BNY Melon, 2017, Alternatives, https://www.bnymellonim.com/ ie/en/intermediary/wp-content/ uploads/2017/06/BNY-MellonAlternatives-Special-Report-2017-printonly-version.pdf

- Burniske, C., 2017, Cryptoasset Valuations, https://medium.com/@cburniske/ cryptoasset-valuations-ac83479ffca7

- Burniske, C. and J. Tatar, 2017, Cryptoassets: The Innovative Investor's Guide to Bitcoin and Beyond, McGraw-Hill Education

- Botev, I., F. B. Ghachem, O. vd Heuvel, J. Hermanns, R.J. vd Mark, R. Ramaekers, B. Schoon,

- P. Schotanus, T. Sterk, J. Verwerft, J. Vijverberg, 2017, The Tide is High – But for How Long?, https://www. aegonassetmanagement.com/globalassets/ asset-management/netherlands/newsinsights/documents/2017/long-termscenarios-2018---2021.pdf

- Botev, I., Assessing cryptocurrencies, 2018, https://www.aegonassetmanagement. com/netherlands/news-and-insights/ assessing-cryptocurrencies/

- Evans, B., 2018, Microsoft, Amazon And IBM: Which Cloud Powerhouse Will Top Q1 Revenue Charts?, https://www.forbes. com/sites/bobevans1/2018/04/09/ microsoft-amazon-and-ibm-whichcloud-powerhouse-will-top-q1-revenuecharts/#5203469014dc

- Lam, E., 2018, Why Bitcoin Behaves Like the Flu, Why Bitcoin Behaves Like the Flu, https://www.bloomberg.com/news/ articles/2018-04-10/bitcoin-is-a-disease-inbarclays-model-that-says-prices-peaked

- Lagarde, C., 2017, Central Banking and Fintech—A Brave New World? http://www. imf.org/en/News/Articles/2017/09/28/ sp092917-central-banking-and-fintech-abrave-new-world

- Pfeffer, J., 2017, An (Institutional) Investor’s Take on Cryptoassets, https://s3.eu-west-2.amazonaws.com/johnpfeffer/An+Investor%27s+Take+on+ Cryptoassets+v6.pdf

- Wheatley, S., D. Sornette, H. Tobiasm, M. Reppen, and R. Gantner, 2018, Are Bitcoin Bubbles Predictable? Combining a Generalized Metcalfe’s Law and the LPPLS Model

Disclaimer

The views expressed are the authors’ alone and do not necessarily reflect the views of their employer.

in VBA Journaal door Fares Ben Ghachem (r), Iavor Botev (l)