The forces of disinflation

The forces of disinflation

The financial crisis has shaken the economic environment to its core, exposing the general population to the despair of confidence withdrawal brought on by large personal financial loss and loss of faith in the financial system. Economic loss was evident in the statistical observation of sharply negative GDP growth in most major economies. The resultant output gap, that is the difference between actual and potential GDP, widened to a multi-decade extreme. This represents a major disinflationary force which may well persist for some years.

Contributing to the economic loss was the private sector’s response to the crisis, which has been to engage in balance sheet repair by spending less, reducing debt and raising savings. The process of deleveraging in the household and corporate sectors is under way, however the scale of deleveraging is large and will likely persist for some years.

The public sector’s response has been to fill the void left by the private sector. Policymakers have pursued an extremely accommodative policy stance, utilising conventional and unconventional, old and new, policy initiatives aimed at stemming economic decline and restoring normalcy to the financial system and public confidence. This pursuit has already led to a rapid deterioration in public sector balance sheets. With the objective of rebuilding confidence and functioning in the financial sector still key, a generally more accommodative policy setting is likely in the years ahead. Ironically this could prove to be inflationary in the medium-to longer term.

What is clear is that the ups and downs of the economic cycle will persist as they have always done. Periods of disinflation will be followed by periods of inflation, as evidenced in history. The key however is to recognise when the economic environment is disinflationary, and for how long it will persist.

The theoretical logic underpinning recently observed and expected disinflationary forces is detailed below, its essence lying in the arguments evident in the output gap and private sector deleveraging. The upshot is that the current disinflationary environment may persist into the foreseeable medium-term environment, that is, the next few years. This is an environment in which economic growth expectations are likely to be downwardly revised and in which policy and market interest rates remain generally low by historical standards.

The logic of disinflation

The outlook for inflation has been hotly debated amongst economics, policymakers and financial market participants this year. On the one hand, there are those who believe that the combination of rapidly rising government deficits and sharp increases in sizes of central bank balance sheets will cause an inflation outburst. Others argue that the unprecedented amount of economic slack will sooner or later start to put downward pressure on wages and prices. As outlined above, these two perspectives can be reconciled by recognising that they pertain to a different time horizon.

Two widely used theories of inflation are examined, each of which assigns a central role to expectations and economic slack in the monetary transmission mechanism. The first theory centres around the money supply, which in modern society has become an unclear and somewhat elusive concept. It concludes that in the foreseeable future the vast increases in central bank money (from policy accommodation) will not lead to a surge in private sector money and credit growth. This is because the demand for central bank money exerted by financial institutions is likely to remain very high given their focus on balance sheet repair, that is deleveraging. The second theory emphasises the importance of slack in the economy. It concludes that an environment of deleveraging by households and financial institutions will keep economic growth below potential. The already-large degree of slack in many economies will grow larger thus further diminishing the degree of pricing power of workers and businesses. This will keep persistent downward pressure on domestically generated inflation which may well fall to levels close to zero over the medium term.

In this process the behaviour of the economy’s supply side and inflation expectations both remain a wild card. As to the former, some reduction in potential economic growth is anticipated, but this will not be sufficient to eliminate the magnitude of economic slack. As regards the latter, there is a risk that inflation expectations will adjust to the downside on the back of a potentially persistent inflation undershoot.

Ultimately however, inflation expectations may adjust upwards in line with policy measures aimed at economic normalisation – for example if central banks mis-time the “exit strategy” (the removal of extreme monetary accommodation) or if they bow to pressure to finance bloated budget deficits. But these are longer-term concerns and they have less relevance for the foreseeable medium-term future.

At this point it is instructive to have a closer look at two widely used theories of inflation, the Quantity Theory of Money and the Phillips Curve. It is noted that these two theories are often seen as mutually exclusive – either inflation is driven by the money supply or it is driven by the degree of slack in the economy. An eclectic view is taken here. In both cases the effect of monetary policy on nominal spending operates via two channels: changes in demand and changes in inflation expectations. This is now explored further.

The Quantity Theory of Money

The essence of the Quantity Theory can already be found in the writings of philosophers such as Hume and Locke in the 18th century. The theory holds that the supply of money, when multiplied by the number of times it changes hands in a certain period, must by definition be equal to the value of all transactions in that period. Assuming that the latter is equiproportionate to the level of GDP one obtains the well recognised equation

M V = P Y

where M represents the money stock, P the price level, Y real income (GDP) and V the (income) velocity of money.

The inverse of the latter (ie M/PY) can be interpreted as the demand for money. Many economic theories assume that this demand falls as the interest rate rises, since the latter will make it more attractive to hold wealth in the form of interest bearing assets. This equation is the theoretical basis for Milton Friedman’s famous statement that “inflation is always and everywhere a monetary phenomenon”. After all, in the long run Y will be determined by the economy’s supply side1 , so assuming a stable demand for money, a given percentage change in M will be reflected in a percentage change in P of similar magnitude.

Money demand is unusually high

While this theory appears straightforward, it is a lot less so in practice. First of all, there is the question of what exactly counts as money in our complex society. This question was a lot easier to answer in earlier times when money was simply gold or silver coins. Indeed there is evidence that in those times the rate of inflation varied with the rate of gold and silver discoveries. In our time the relationship is more complex. Determining which monetary aggregate (M) has a stable relation ship with nominal income (PY) is unclear because many assets have money-like properties. Added to this, the extent to which they possess these properties changes over time, for example due to changes in payment technology, financial innovations and changes in risk averion2.

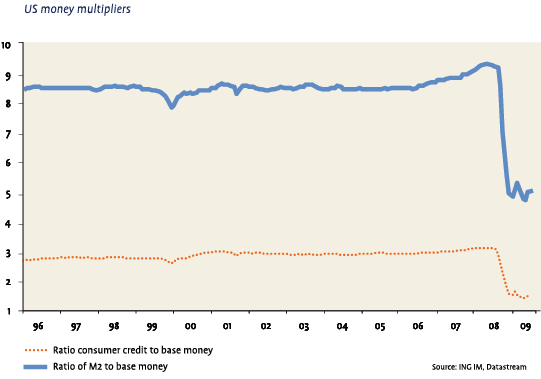

Despite this definitional difficulty, the Quantity Theory is explored for some insight into the current situation in which central banks have injected unprecedented amounts of liquidity into the financial system. Notably central banks have extended loans to the banking system and have engaged in the direct purchase of a wide range of assets, both of which were funded by the creation of base money (M0). M0 is in a sense the purest definition of money and is roughly equal to the liability side of the central bank’s balance sheet3. This monetary aggregate literally constitutes the basis for all broader definitions of liquidity. The reason is that banks only need to hold a fraction of their deposits in the form of reserves at the central bank. Hence, when the central bank increases the amount of reserves in the system, banks will be able to expand their loan base by a multiple of the initial liquidity injection.

On face value there is an argument that the doubling of the monetary base will at some point cause an explosion in broader money and credit growth – resulting in higher inflation. Nevertheless, this argument overlooks one important factor in the quantity equation. While it is true that the supply of M0 has increased very rapidly, it can be argued that the demand for base money by the banking system is currently at least as high (that is, V has fallen rapidly). This is because banks have engaged in, and are likely to persist with, the process of deleveraging and balance sheet restoration.

On face value there is an argument that the doubling of the monetary base will at some point cause an explosion in broader money and credit growth – resulting in higher inflation. Nevertheless, this argument overlooks one important factor in the quantity equation. While it is true that the supply of M0 has increased very rapidly, it can be argued that the demand for base money by the banking system is currently at least as high (that is, V has fallen rapidly). This is because banks have engaged in, and are likely to persist with, the process of deleveraging and balance sheet restoration.

One must bear in mind that the ability of banks to lend depends on the quality of their balance sheet. Banks have already taken substantial write downs on toxic assets. Even though a large part of the loss associated with these market traded assets may have been taken, the deterioration in economic fundamentals (such as rising unemployment, falling house prices and business profitability) may increase the share of non-performing loans in the foreseeable future. In such an environment banks will tend to focus on reducing the size of their balance sheets, showing a high preference towards holding safe and liquid assets. History teaches that this tends to be a drawn out process.

From this, it is unlikely that the vast amounts of recently created M0 will soon lead to a rapid acceleration in credit growth and broader money measures. On the contrary, the risk in the foreseeable future remains clearly on the side of a further decrease in these broader measures of liquidity which are representative of private sector behaviour.

The Transmission Mechanism is impaired

The Quantity Theory is limited in its ability to rationalise changes in underlying economic behaviour (the transmission mechanism) which ensure that the identity holds. This transmission mechanism has itself been the subject of heated debates between economists for decades. Two essential features stand out:

Firstly, changes in monetary policy will induce a change in (inflation) expectations held by the private sector. In the context of the Quantity equation, these inflation expectations mostly show up in changes in money demand. If vast increases in the money supply (e.g. to finance large budget deficits) cause people to believe that inflation will accelerate in the future, they will try to economise on their money holdings (i.e. V will increase)4. This will only reinforce the inflationary impulse exerted by the increase in the money supply and if left unchecked this could lead to hyperinflation in the loner term. Real world examples of the latter provide evidence of the power of these expectations. In many cases the announcement of credible fiscal consolidation and/or monetary reform caused V to fall because inflation stabilised well before actual money growth slowed down.

Secondly, when the money supply increases, people will not willingly hold on to this extra cash. Rather they will substitute it for assets, commodities or goods and or services. The reason is that the yield on money is near zero. Hence, people will not hold more money than deemed necessary for their immediate transaction and precautionary purposes. The increased demand for these categories will tend to raise their quantity supplied and/or their prices5. The extent of the price increase then depends on the supply characteristics of the market in question. For instance, if increased money supply raises the demand for housing in Manhattan (the supply of which is fixed) the effect will mostly be a rise in the price. On the other hand, if it raises the demand for steel in a situation where the capacity utilisation rate in that industry is well below average, the main effect will be an increase in the supply of steel.

Moreover, prices in different markets will react at different speeds to the demand supply imbalances. In the case of commodities, prices will adjust very quickly to clear the market. However, in many product markets, and especially in the labour market, prices will tend to adjust only slowly (downwards rigid) to a disparity between underlying demand and supply.

It is noted that rising asset prices will at some point stimulate demand for goods through positive wealth and cost of capital effects, while rising commodity prices directly feed into inflation. In this sense one can say that a large enough increase in the supply of money will eventually cause a sufficient number of bottlenecks to show up in the real economy which, in the longer term, will cause the overall price level to rise.

The Phillips Curve

The Phillips Curve theory is a cornerstone of modern macroeconomics and it features prominently in models used by central banks and others to forecast inflation. This model does not have a direct role for the money supply but it does shed more light on the transmission mechanism, in particular on the crucial role of expectations and the output gap.

Expectations

The essential idea is that wage and price setters (partly) base their decision on expected future price developments because it is costly or difficult to change prices and wages very frequently (think of wage contracts). In theory, these expectations are considered “rational”, which loosely means that people use all available information when formulating their assessment – including their knowledge of the economic environment and the policy and regulatory environment. As a result, it is held that people will not make systematic mistakes in their forecasts of inflation. The importance of expectations in this construct places a large premium on central bank credibility. Simply, if the central bank can convince the public that future inflation will be close to target, the public will act accordingly, in effect helping the central bank to achieve its target.

One implication of this theory is that past rates of inflation may not be very helpful in explaining the current inflation rate6. However many empirical tests which regress inflation on past inflation rates as well as other explanatory variables (such as the output gap) do find that the coefficients for these past inflation rates differ significantly from zero – that is, the past is a helpful guide to the future. One explanation for this is that there is some inherit persistence due to (for example) overlapping wage contracts, and the fact that wages may be formally or informally indexed to inflation or indeed set with reference to past real wage developments in competing sectors within the economy. Another explanation is that expectations are simply not rational; as people do not know the model of the economy and information gathering is costly, they use past inflation rates as their guide and rule of thumb for assessing and forecasting future inflation.

The output gap

This concept is loosely defined as the difference between supply and demand in the overall economy. Simply, if aggregate demands exceeds supply, the resultant inflationary force will persist until the gap is closed. Similarly, if aggregate supply exceeds demand, inflation will fall until equilibrium is restored. A gap can persist for a long time because in many markets prices do not always adjust instantaneously. This is why the output gap is to a large degree determined by what happens on the demand side of the economy. Nevertheless one should bear in mind that the supply side of the economy changes over time as well, impacting on the output gap albeit at a slower pace. Supply forces are essentially determined by changes in the quantity and the quality of the two factors of production, labour and capital.

The inflation outlook

The inflation outlook

The key contention of this paper is that risks to inflation reside firmly on the downside at this time and in the coming few years. This is premised on the belief that the recently unprecedented fall in demand has opened up a large output gap. With household and financial sectors remaining focussed on deleveraging, growth in the developed economies may remain below potential for some time yet. This means that the output gap will continue to widen in the foreseeable future. In this respect, it will continue to exert downward pressure on domestically generated inflation and wage growth for at least the next two to three years.

Some commentators argue that the financial crisis has reduced potential output to such an extent that the output gap could well be significantly smaller than many believe. One argument in this respect is that the credit boom led to a misallocation of resources. In the current account deficit countries (US, UK, Spain etc.) a decline in interest rates and risk premia led to a huge expansion of the construction and financial sectors relative to other sectors, a process which will now need to be reversed. Conversely in Germany and other current account surplus countries, strong domestic demand growth in their export markets led to a relative expansion of the tradeable goods sector which is no longer sustainable given the structural adjustments in these export markets. Effectively, some of the specialist capital and knowledge accumulated in those sectors which expanded rapidly during the boom years has become obsolete.

Another factor which exerts a negative effect on potential output is the increase in the cost of capital combined with the sharp drop in capacity utilization seen in many sectors. This has clearly depressed investment spending (the growth in the capital stock) in all sectors of the economy. Some international organizations such as the European Commission, the IMF and the OECD estimate that all this may result in a permanent decline of EMU potential output in the order of 4-5%. While this is very substantial, one must also bear in mind that this one-off loss would be absorbed over a number of years. Shifting resources between sectors takes time; the effect of the loss on the level and productivity of the capital stock will become gradually more visible as the existing capital stock depreciates7. As a case in point, the European Commission estimates that potential growth in the Euro area will fall from a little over 1.5% in 2008 to around 0.7% in 2009 and 2010.

A permanent decline in potential growth in developed economies is likely due to an ageing population, but also because risk premia are likely to remain structurally higher than they were during the leveraged boom years as people revise downwards their personal activities as they embark on the deleveraging process. Higher risk premia imply a higher cost of capital, which negatively affects the growth rate of the capital stock as well as innovation and R&D. Besides this, a structural rise in unemployment and the likelihood of a more regulated financial environment would also negatively affect potential growth.

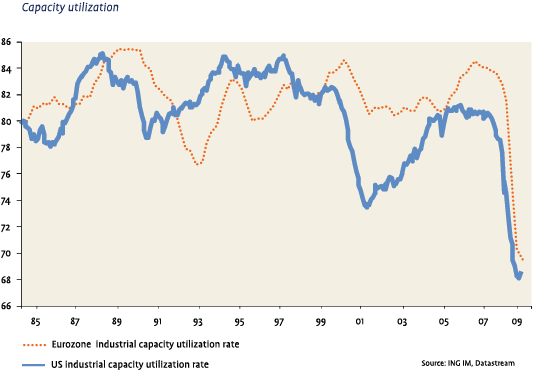

Uncertainties surrounding the supply side of the economy mean that estimating the exact value of the output gap will prove difficult. Nonetheless it does appear far-fetched to assume that the fall in supply has matched the largest decline in demand seen since WWII. The truth often lies between extremes, and there are a host of indirect indicators of the output gap which are influenced by demand and supply factors as well and which are observably at record lows right now. The manufacturing industry capacity utilisation rate is a case in point. Survey evidence also contains indirect information, for example by asking firms to what extent they perceive labour or capital to be a factor in constraining production or by asking consumers about their assessment of the labour market. Finally, it is hard to believe that the rise in unemployment rates (which in the US is already 5 pp above its low) will be entirely driven by a rise in structural unemployment.

The expectational challenge

The output gap is expected to place downward pressure on inflation but its ultimate effect will be very much governed by the evolution of inflation expectations. If the latter are firmly anchored to central bank targets, the output gap effect will be mitigated as wage and price setters continue incorporate the anticipation of future price stability into their decisions. If, on the other hand, inflation expectations are (partly) based on past rate of inflation, the disinflationary effects may be reinforced.

In this respect, many central banks currently take some comfort from the fact that longer term inflation expectations remain stable and close to their targets. It is indeed striking that both actual rates of inflation and inflation expectations (for example, as measured in the survey of forecasters) have been very stable over the past decade. One explanation for this phenomenon is that an increase in the degree of central bank credibility has caused the public’s inflation expectations to be more tightly anchored to the inflation target.

However, we should not be oblivious to the fact that this outcome may also have been produced by sheer luck; in particular the influence of China on defraying the pressures on local resource utilisation in the form of cheap imports. This allowed central banks to run a looser policy than would have otherwise been possible. In this respect, it is very noteworthy that domestically oriented service sector inflation tended to be high over the past decade while goods price inflation was negative in many countries. Hence, in a sense macroeconomic shocks were absorbed by rising asset prices and current account imbalances rather than by growth and inflation. Because of this, both past inflation rates as well as the inflation target were good predictors of future inflation. This makes it very difficult to test whether central bank skill or luck was the dominant factor.

While one could accept that central bank credibility has improved over the past two decades, it would be dangerous to discard the overwhelming evidence that past inflation rates also matter for current inflation (if only because of overlapping wage contracts and indexation to past inflation). Loosely speaking this means that once inflation becomes entrenched at below-target levels, it will have a tendency to stay there. In this respect, it is important to realise that central banks have earned their credibility by bringing down inflation from the high and variable levels in the early 1980’s to the low and stable levels seen during the past decade. This entailed decisive and sometimes painful policy actions which in the end delivered clear results. This gradually helped to convince the public that central banks were serious about their inflation target. Central bankers, as guardians of stability, have had credibility tarnished somewhat by recent events. Moreover their resolve against persistent inflation undershoots has not really been tested yet; central banks have now entered unchartered territory.

This uncertainty about how inflation expectations will react is aggravated by the fact that the monetary transmission mechanism is currently impaired and its effectiveness has become more uncertain in an environment where short-term interest rates are close to zero and central banks have had to resort to instruments with which they have had previously no or limited experience (quantitative easing).

On balance, there is a substantial risk that inflation expectations in the real economy, those embedded in the decisions of wage and price setters, will shift to the downside between now and the medium term. As a consequence, central banks will be motivated to keep policy interest rates relatively and generally lower than forecasters currently expect. The argument that a prolonged period of unprecedented low interest rates and liquidity injections will ultimately cause an increase in longer-term inflation expectations, while plausible, is a longer term issue and one which will clearly depend on the effectiveness and timeliness (or otherwise) of monetary and fiscal policy actions.

Conclusion

In this article we discussed the inflation outlook using two widely used theories of inflation both of which assign a central role to expectations and economic slack in the monetary transmission mechanism.

It is concluded that vast increases in central bank money will not lead to a surge in private sector money and credit growth because the demand for central bank money exerted by financial institutions is likely to remain very high while they are focussed on the medium-term focus of balance sheet repair.

It is also concluded that the next few years will be characterised by an environment of deleveraging by the private sector – households and corporates – which will keep growth below potential for some years. As a result, the already large degree of slack in many economies may well grow larger, further diminishing the degree of pricing power of workers and businesses and maintaining persistent downward pressure on domestically generated inflation. In practice, annual inflation may turn out to be lower (closer to zero percent!) over the next two to three years than forecasters currently believe.

In this process the behaviour of the economy’s supply side and inflation expectations both remain a wild card. As for the former, some reduction in potential growth is expected but not sufficient to eliminate the degree of slack. As far the latter, there is a risk that inflation expectations will adjust to the downside on the back of a persistent inflation undershoot.

Whatever view one takes on inflation, medium or longer term, the one certainty is that inflation uncertainty has increased. The view expressed here is that the current disinflationary environment may persist into the foreseeable medium-term environment, that is, the next few years, creating an environment in which economic growth is lower than expected and in which policy and market interest rates remain low by historical standards.

Notes

- The reason for this is that prices and wages are fully flexible in the long run. Because of this demand will always adjust to the potential level of production.

- An increase in risk aversion implies that agents will have a higher preference for holding safe and liquid assets.

- More precisely M0 consists of the central bank’s non interest bearing debt to the private sector which consists of currency in circulation plus the reserves held by the banking system. The liability side of the central bank balance sheet of course also contains non-money elements such equity (which is held by the ministry of finance), the account the ministry of finance holds at the central bank (which is not money since this is debt to the public sector) and, in some cases, interest bearing bills issued to the private sector. These items tend to be small relative M0. However, this may change once the economy normalises and the central banks seeks to decrease M0.

- In this respect, inflation expectations can even be a selffulfilling prophecy: If people believe inflation will rise then V will fall causing actual inflation to rise even if M remains constant!

- Since money demand is an increasing function of prices and incomes, this substitution process will eventually cause actors to willingly hold the new higher level of money.

- Here there is a clear analogy with the efficient market hypothesis in finance which implies that past stock prices have no predictive power for future price movements.

- A real world example of this is public infrastructure. Cutting investment in that sector will not materially alter the quality in the first few years but as time progresses more and more problems become visible. In other words, the productivity of public infrastructure gradually declines over time.

in VBA Journaal door Eric Siegloff (r), Willem Verhagen (l)