There’s a common narrative that fee compression is the main problem that long only equity and fixed income active managers face. We disagree. This article explains that new forces of change, in combination with years of complacency during good times, has caused pressure on these traditional long only active manager business models. We explore the key internal and external drivers of this change and argue that these managers must act now. To bridge the gap between strategic thinking and execution to build an advantageous position in today’s asset management arena, managers must rethink the role that technology plays within their organization.

The focus of this article are the traditional long only equity and fixed income mid to large size active managers, i.e. managing more than 50bn USD in assets.

INTRODUCTION

INTRODUCTION

Over the past few decades, asset management has established itself as an attractive business. Rising free cashflows, huge operating leverage, sticky customers, and the growth in assets and valuations have led to increasing fees. However, this comfortable scenario gave way to complacency. Many traditional asset managers were either benchmark-huggers or factor funds – like quality or value funds – generating low idiosyncratic returns. Peer benchmarking provided these managers with comfort – but it wasn’t helpful. As per the latest S&P Dow Jones indices annual report, 64.5% of large cap mutual funds underperformed S&P 500 over 1 year, 85.1% underperformed over 10 years and 91.6% underperformed over 15 years (Pisani, 2019). At the same time, there are new entrants into the industry offering new strategies and asset classes which has led to an outflow of assets from the traditional active asset managers. Long-only traditional asset managers reported $22.8 billion in net outflows for the first quarter of 2019 and net outflows of $499 billion over the past four quarters, said eVestment’s Q1 2019 quarterly Traditional Asset Flows Report (Laurelli, 2019).

This articles describes the internal and external challenges facing the industry and proposes some ways in which asset managers can adapt to these challenges and thrive today’s business environment.

EXTERNAL CHALLENGES

This is a time of intense change driven by three main factors. The regulatory environment is becoming tougher as regulators begin harmonizing rules across the globe. Meeting these requirements takes considerable time away from already busy technology and business teams. In addition, regulators are asking for dumps of data – which can be a little frightening given that asset managers’ internal data is not typically in the best of shape (Statpro, 2016). Secondly, asset managers are now adding new strategies – particularly passives and alternatives – that put pressure on business models to support those requirements. And lastly, clients are demanding more from their managers to demonstrate the performance that they are paying for.

Clients are now much better informed. They want their managers to disaggregate returns into the drivers of these returns and they want access to granular portfolio data to validate their hypothesis. They need to be convinced that the process is repeatable and not down to luck, or a factor tilt which might only work in the short term. Unless asset managers can demonstrate this outperformance, clients will look elsewhere. Amongst other challengers, passive funds (ETFs), alternatives and hedge funds that leverage alternative datasets are three challengers to long only asset managers that have been growing assets and teams rapidly in the recent past.

GENERAL PASSIVE INVESTMENT STRATEGIES

There are three key factors responsible for the rise of passive products: the rise of the robo advisors that offer portfolios or strategies built off ETFs, the growing acceptance of ETFs by investment consultants, and the fee wars that have led to beta becoming almost free. In addition to cheap beta access, ETFs now offer desired factor returns – like quality, momentum, or value. Adoption of smart beta has now spread to over half of asset owners globally (White, 2019).This allows investors to create a portfolio which represents their view of the world, at relatively lost cost.

Liquidity is a prominent concern for investors in the ETF space during systemic crises – a liquid layer on underlying illiquid assets can create issues during times of high volatility and redemptions. It is not easy to run an ETF business, most funds have little liquidity and have struggled to gain assets (Kim, 2019). In addition, running these funds at single digit basis point fee structure requires a heavily automated and robust technology infrastructure.

ALTERNATIVES

Alternatives are in high demand, especially from asset owners with long-term cash flow needs like pension funds or insurance firms. Alternatives create value in multiple ways. Firstly, there is limited competition in private assets, and prices must account for their illiquid nature. Secondly, these managers have operational specialists that help improve processes and procedures. This helps boost ‘operational alpha’ by replacing less competent management teams with motivated professionals who are rewarded well for their efforts. Thirdly, these managers control the entry and exit of their positions and the 10-year structure of alternate funds provides manager with the flexibility to ride cycles. These funds also allow investors to access the illiquidity premium. According to a 2018 paper by KKR, Private Credit generally outperforms the liquid high yield market by about 200-300 basis points throughout the cycle, compared to 500 basis points or so for Private Equity relative to Public Equities (McVey, 2018). This is significant over long-time horizons due to compounding effects.

CHANGE IS THE ONLY CONSTANT, AND SUCCESS IS LARGELY DICTATED BY HOW WELL ORGANIZATIONS ADAPT, BUILD AND DEFEND THEIR COMPETITIVE POSITION

The main concerns revolve around the opaqueness of these funds and high fees (2:20 structure). It is not easy to run an alternatives platform either, incumbents get access to all the best deals, have the best operational talent, and have access to large funds – creating a performance differential between top quartile and bottom quartile funds.

HEDGE FUNDS LEVERAGING ALTERNATE DATASETS

The third threat are hedge funds that produce great performance and leverage a different kind of ‘alternate’ – alternative datasets. Credit card spending data, email receipts, parking lot records, satellite imagery, and commercial vehicles data – these datasets are fed into complex machine learning models that predict inflection points for better decision-making. In addition, these models are now analyzing large unstructured datasets like text to extract real-time information on investable companies, their competitors, and their suppliers – often understanding changes even before company management. This complements traditional sources of research, like financial statements and conference calls, which are less frequent. These funds employ an army of data scientists, data sources, and professionals with PhDs that leverage the latest technology to extract bits of idiosyncratic alpha from capital markets. So successful are these funds that the likes of Two Sigma, Millennium and Point72 are growing their teams by 10-20% over the last year. D.E. Shaw Group plans to raise the fees it charges for its $14 billion flagship D.E. Shaw Composite fund to a 3 percent management fee and 30 percent performance fee, effective January 1 (Segal, 2019). This gives us an insight into demand.

These funds can be good diversifiers in investment portfolios given the low correlation in returns that some funds are able to produce. It is extremely hard for traditional asset managers to replicate these strategies. Not only do you need access to the best quality talent but also a robust technology infrastructure that can extract, organize and process the huge volumes of alternative datasets.

INTERNAL CHALLENGES

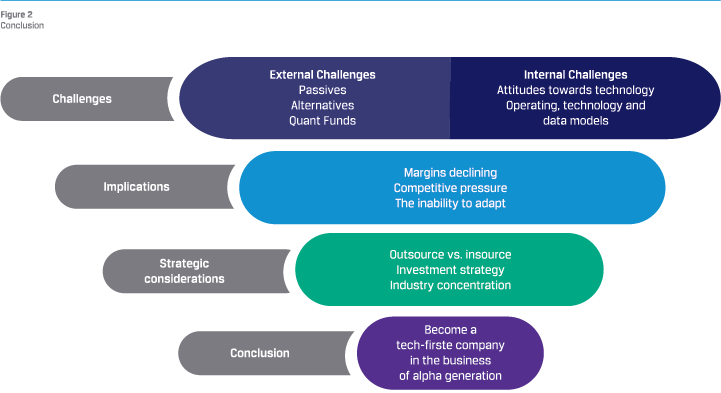

Change is the only constant, and success is largely dictated by how well organizations adapt, build and defend their competitive position. In the above sections, we described how threats from passive ETFs, alternatives and quant funds is leading to outflows from traditional asset managers. This will continue. Competition will further intensify and active managers that fail to adapt will experience more outflows and negative operating leverage which further erodes operating margins.

We now turn our attention to the internal challenges. Here we describe some of the causes of complacency and inabilities to adapt to changes in the business environment – causing weakness in competitive positions and limited ability to capitalize on new opportunities.

FRONT OFFICE AS A REVENUE CENTER. OPERATIONS AND TECHNOLOGY AS A COST CENTER

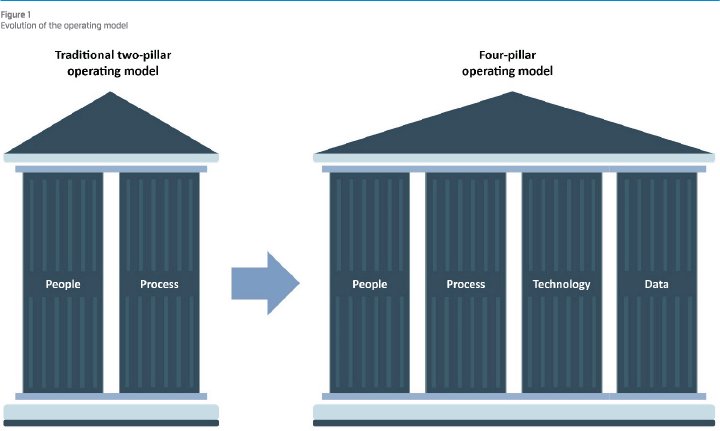

One of the fundamental weaknesses in long only active asset managers is the attitude towards operations and technology. My own experience consulting for buy side firms is that technology is often considered a burdensome cost center, rather than a source of strength to be nurtured. As asset manager operating models have evolved from a traditional two-pillar framework (people and processes) to a four-pillar framework (people, processes, technology and data) over many decades, this attitude must change. Due to weaknesses in the technology and data pillars, asset management operating models are struggling to support business growth. This creates a multitude of problems as business complexity steadily increases with the addition of new asset classes, expansion into new geographies and evolving pressure from clients and regulators.

One of the fundamental weaknesses in long only active asset managers is the attitude towards operations and technology. My own experience consulting for buy side firms is that technology is often considered a burdensome cost center, rather than a source of strength to be nurtured. As asset manager operating models have evolved from a traditional two-pillar framework (people and processes) to a four-pillar framework (people, processes, technology and data) over many decades, this attitude must change. Due to weaknesses in the technology and data pillars, asset management operating models are struggling to support business growth. This creates a multitude of problems as business complexity steadily increases with the addition of new asset classes, expansion into new geographies and evolving pressure from clients and regulators.

Another key issue is that as technology vendors build new solutions to meet these evolving requirements, in some cases the front office teams make those technology selection decisions. Internal technology teams are then tasked to integrate new applications into their existing technology stack. Over time, a spaghetti of technology systems leads to disparate operating, technology and data models. This creates challenges for current operational processes, but also hinders adaptation to new and evolving requirements.

DISPARATE OPERATING, TECHNOLOGY AND DATA MODELS

Asset managers tend to have disparate business models, systems and data structures across geographies. This is in large part due to the complexity in overcoming local regulatory, client and product needs in each territory. This disparity may accelerate time-to-market, but it impedes a global service model for its clients. This causes three big challenges. Firstly, clients don’t get a seamless experience. One single client request can often involve multiple teams across different geographies. Secondly, data governance and management can become very messy. Most asset managers place data among their top and most complex challenges. Asset managers need to create the right policies and address issues of data ownership, quality and integrity so that they can feed ‘clean’ data into their accounting and investment book of record data lakes. Thirdly, managing and maintaining disparate operating models and technology stacks can make an asset manager feel very fragmented.

IMPLICATIONS – EXTERNAL CHALLENGES WITHOUT THE ABILITY TO ADAPT

So, what does all this mean? A combination internal and external challenges have caused tangible issues for traditional asset managers. Rising markets are providing additional fee income, however there is secular pressure on fee levels (as a % of AUM) and costs are increasing. According to an analysis by strategy consultant Casey Quirk in 2019, the median spend for noncompensation costs – including regulatory expenses, technology, and office space – accounts for nearly one-third of a firm’s total budget in 2019, compared with 26 percent in 2014. (Segal, 2019).

As a result, there is a pressure on margins. Active asset managers must rethink their business models and build capabilities to adapt to the changing external environment and remain competitive.

OVERCOMING CHALLENGES – REDEFINE THE ROLE OF TECHNOLOGY AND BUILD CAPABILITY

The most important change that asset managers should make is to redefine which business are they in. As an example, Google, Facebook, Amazon, Uber and Airbnb are tech-first and search engines, social networks or marketplaces second. Similarly, what kind of capability can asset managers build, (by leveraging technology) that allows them to a) meet their client needs better b) generate alpha and c) cut costs? It is a change in mindset, it is thinking tech-first.

Citing another example, when ETF managers offers funds at single digit basis points, what kind of technology infrastructure is powering their business? The answer is likely a highly automated one. The competition in the industry has forced them to embrace technology. A similar fate awaits traditional active asset managers.

These asset managers need to move towards a tech supported alpha approach. Firms that acknowledge this shift earlier than other will be the ones that will not only survive but become leaders in the industry. Whether there is a need to streamline operations and reduce costs by leveraging technology, or it is to gain new investment research insights by leveraging big data or it is building new capabilities for meeting client specific needs, technology can transform the business model of traditional asset management firms.

CONSIDERATION: OUTSOURCE OR INSOURCE

It is widely accepted that external outsourced partners and software vendors are an important component of an asset manager’s technology architecture however, building internal technology team capability is often overlooked or underappreciated. Internal teams must become more sophisticated from two perspectives: building new differentiated capability, and to maximize value from new vendors and partners. These teams are also responsible for building the right technology infrastructure where manual tasks can be automated, data can be handled properly, and the needs of the various stakeholders can be met.

Outsourcing contracts need to be reviewed on the value added by outsourcing providers vs the ability to run them inhouse at a lower cost. Techno-functional teams – where technology and functional experts work as equals – need to drive business strategy forward. Each new capability needs to be understood from a holistic perspective that includes supportive data and technology requirements – not from a front-office-only perspective.

CONSIDERATION: INVESTMENT STRATEGY

Clients are now looking for asset managers to deliver ‘pure’ alpha (idiosyncratic), risk premia and diversification. Beta is now free, factor beta is close to free, and “after fee” performance is closely scrutinized. A sound investment and research process is key for managers to outperform their respective benchmarks, however this becomes harder when trading volumes and market capitalization of underlying securities increase. (Research Affiliates, 2015). Alternative data – information that falls outside of a traditional research process like aggregated consumer spending or product review data – are becoming more commercially available. According to alternativedata.org, the buy side spend on alternative data has increased from $260m in 2016, $400m in 2017 to $650m in 2018 and is projected to rise further to $1.08b in 2019 and $1.7bn in 2020 (AlternativeData.org, 2019). Insights generated from alternative datasets can add value to the research process.

Clients are now looking for asset managers to deliver ‘pure’ alpha (idiosyncratic), risk premia and diversification. Beta is now free, factor beta is close to free, and “after fee” performance is closely scrutinized. A sound investment and research process is key for managers to outperform their respective benchmarks, however this becomes harder when trading volumes and market capitalization of underlying securities increase. (Research Affiliates, 2015). Alternative data – information that falls outside of a traditional research process like aggregated consumer spending or product review data – are becoming more commercially available. According to alternativedata.org, the buy side spend on alternative data has increased from $260m in 2016, $400m in 2017 to $650m in 2018 and is projected to rise further to $1.08b in 2019 and $1.7bn in 2020 (AlternativeData.org, 2019). Insights generated from alternative datasets can add value to the research process.

REDEFINE THE BUSINESS THAT YOU ARE IN

Asset managers can leverage insights from these datasets to generate alpha on more liquid stocks to build a scalable approach. However, this requires huge commitment from managers to invest in data science professionals, the data itself, and a cutting-edge technology infrastructure. This isn’t a shortterm initiative. It may take years before managers can derive actionable signals from these datasets but when they start doing so, managers will begin building a source of competitive advantage. And when star managers leave, this moat will remain with the asset manager.

CONSIDERATION: INCREASING INDUSTRY CONCENTRATION

Technology, coupled with the moats that businesses develop around them, lead to industries that are far more concentrated than their non-tech counterparts. Case in point, Amazon, Alphabet (Google), Airbnb, Uber and the list goes on. However, in the asset management domain, ETF providers that have invested heavily in technology have created moats for themselves. The fee war in the passive space has forced managers to squeeze each ounce of efficiency out of their business model and the successful managers have been those that have leveraged technology to reduce cost. Blackrock for example had an in-house technology platform called Aladdin which they turned into an entirely new business. If you look at the ETF space, it is far more concentrated than the mutual fund industry (Kim, 2019). This gives us a glimpse into the future of active asset managers.

The industry will become densely bifurcated with a concentration of asset lying with a few mega managers, and a string of smaller fund managers with niche but unscalable strategies. Managers will either consolidate, disappear or specialize and build new capabilities that carry them into the future.

CONCLUSION: REDEFINE WHICH BUSINESS YOU ARE IN

Traditional long only active asset manager business models are facing new external forces of change. Due to disparate operating, technology and models – and years of viewing technology as a cost center, rather than an opportunity – managers are in a disadvantageous position to be proactive or even reactive to these external factors. This amplifies the threat from substitutes like passives, alternatives and hedge funds.

Asset managers have historically been ‘technology-last’ and preferred to throw people at problems rather than developing technology capability. The most important change that asset managers need to make is to redefine which business they are in. Asset managers are being transformed into tech companies that are in the business of alpha generation. The asset manager of tomorrow must follow the world’s most successful technology firms and build talented, cross-functional teams. These teams will drive the vertical integration of new capability to better execute an asset manager’s position and build a more sustainable competitive advantage in today’s business environment.

Disclaimer: The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official position of the Stradegi Consulting or its member firms.

Literature

- Alternative Data, 2019, What is Alternative Data?, Article on alternativedata.org https://alternativedata.org/ alternative-data/

- Kalensnik, V and N. Beck,2015, Reeling In Small-Cap Alpha, Research Affiliates Insight Article, Research Affiliates.

- Kim, C.,2019, The ETF Business Is Dominated by the Big Three. The SEC Is Suddenly Concerned, Article on Barron’s. https://www.barrons.com/articles/etfsare-dominated-by-blackrock-vanguard-and-state-street-thesec-is-concerned-51554512133, 5 April 2019

- Laurelli, P.,2019,.Traditional Asset Managers Start 2019 with Outflows After Tough 2018, Blog on evestment. https://www.evestment.com/traditionalasset-managers-start-2019-with-outflows-after-tough-2018/, 30 May 2019

- McVey, H.,2018,. Rethinking Asset Allocation, Whitepaper KKR, KKR

- Pastor, L, Stambaugh, R. and L. Taylor, 2015, Scale and Skill in Active Management, Journal of Financial Economics, Vol. 116 nr 1: 23-45.

- Pisani, B., 2019, Active fund managers trail the S&P 500 for the ninth year in a row in triumph for indexing, Article on CNBC. https://www.cnbc.com/2019/03/15/activefund-managers-trail-the-sp-500-for-the-ninth-year-in-a-rowin-triumph-for-indexing.html#, 15 March 2019

- Segal, J., 2019,. 3-and-30 Is Back for D.E. Shaw, Article Institutional Investor. https://www.institutionalinvestor. com/article/b1f172zs4089yq/3-and-30-Is-Back-for-D-E-Shaw, 19 April 2019

- Segal, J.,2019,.The Rising Expense That’s Pressuring Asset Managers, Article on Institutional Investor. https://www. institutionalinvestor.com/article/b1g08j2zdlg3s6/The-RisingExpense-That-s-Pressuring-Asset-Managers, 25 June 2019

- Statpro, 2016, Five Reasons Why Poor Data Control Is Holding Back Asset Managers, Blog on Statpro. https://blog.statpro.com/blog/five-reasonswhy-poor-data-control-is-holding-back-asset-managers, 8 December 2016

- White, A.,2019, Most Asset Owners Are Now Smart Beta Investors. Article on Institutional Investor https://www. institutionalinvestor.com/article/b1fsllwrf8fxs6/Most-AssetOwners-Are-Now-Smart-Beta-Investors, 10 June 2019

in VBA Journaal door Vivek Singh Jamwal