The design of the financial set-up of a pension fund relies heavily on the financial parameters, most notably the discount rate for pension liabilities and the expected return on assets. It is therefore important to all stakeholders that the parameters are chosen in the best possible way. For Dutch pension funds, these parameters are bounded by legal guidelines. Minister Donner of Social Affairs appointed a commission to evaluate the original parameters.2 The commission, led by former CPB president Henk Don, has failed to come up with a uniform advice, with the main dispute being the equity risk premium.3

This article discusses the estimation of the equity risk premium and advices pension funds on how to deal with uncertainty in financial parameters, making the pension fund policy less dependent on the financial parameters.

This article discusses the estimation of the equity risk premium and advices pension funds on how to deal with uncertainty in financial parameters, making the pension fund policy less dependent on the financial parameters.

Setting the scene: Definition and prudence

In academic literature and in practice, we find various approaches of how to define the equity risk premium. We define the equity risk premium (ERP) as the total cumulative annualised return on equity minus the total cumulative annualised return on government bonds (proxy for risk free rate of return). As follows from this definition, we consider the geometric mean of the return on equity (and not so much the arithmetic mean).

Of course, any estimation of the future geometric mean return goes hand in hand with a great deal of uncertainty. We believe that we need to address this uncertainty from an integral risk perspective. By this, we mean that all uncertainties in the (pension fund) system should be considered in relation to each other. If we need to make a careful decision, it should be based on the outcomes of our analysis, for instance the probability of underfunding, or the likelihood of not granting full indexation. If the stakeholders feel prudence is required, it should be made visible by the output variables, rather than on the input parameters. If done, the other way round, we are at risk of stacking various prudence measures, distorting the final vision.

Equity risk premium

Equity risk premium

We will start the discussion on the equity risk premium with a look at historical data. In this context, the study of Dimson et al.4 is commonly referred to. Dimson estimates the equity risk premium on a diversified portfolio of mature market economies (like the MSCI World index) equal to 4.0% when measured over the period 1900-2005. If we incorporate the more recent period, the ERP is 3.4% over 1900-2008.5 If we incorporate the bigger part of 2009 in the data, the ERP comes back up to 3.9%.

It should be stressed that in his research Dimson uses a market cap weighted worldwide equity portfolio as a base. The results of the study depend on the index that is used, and results will differ if a different index, e.g. a GDP weighted world index, is used. We have left this matter for future research.

On a side note, the ERP is by no means a stable variable, with significant variation over time. Furthermore, it displays significant differences over various regions.

On a side note, the ERP is by no means a stable variable, with significant variation over time. Furthermore, it displays significant differences over various regions.

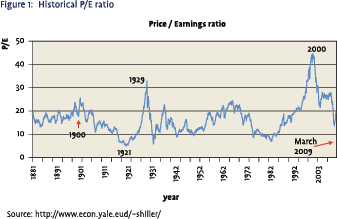

Using historical data for use of future prognosis is something that should be done with great care. In general, historical data is prone to several data biases, like survivorship bias, easy data bias and the peso problem (see frame). Also, during the last century we experienced an increase in the efficiency of the financial markets, allowing for greater financial diversification. Furthermore, we should take a close look at what causes the return. Academic literature6 points out that a significant part of the total return in the period 1900-2005 is caused by revaluation, i.e. an increase of the price/earnings ratio of equities, as illustrated in figure 1. In an arbitrage free world, such a revaluation is not to be expected to happen again, ex ante.

If we consider the revaluation effect over the longer period (1900-2008) we note that the P/E ratio at the end of 2008 is 4 points lower than primo 1900. This shows that the revaluation effect is less significant for this time period.7

If we consider the revaluation effect over the longer period (1900-2008) we note that the P/E ratio at the end of 2008 is 4 points lower than primo 1900. This shows that the revaluation effect is less significant for this time period.7

Let’s take a closer look at the causes of the historical returns. Academic literature8 has investigated the building blocks of historical equity returns, as illustrated in the figure below. As this analysis shows, the total equity return over the period 1926-2000 is 10.7%, which can be broken down to a bond yield of 5.2% and an effective risk premium of 5.2% (first bar in figure 2). Please note that the decomposition does include a statistical error term of 0.3% (a.o. due to correlation effects).

Financial Economics teaches us to explain the equity return through the framework of the dividend discount model.9 In the second bar of figure 2, the total return of 10.7% is broken down to the components of the dividend discount model, where its parameters are equal to the average realisations of the in-sample period. Given an average inflation of 3.1%, a dividend/ price ratio of 4.3% and a real earnings growth of 1.8%, we deduct that of the total return (almost) 1.5% is attributable to historically experienced revaluation effect.

This brings us to a framework for estimating a forward looking ERP (actually, it gives a framework for estimating equity returns, but the ERP can be deducted by subtracting the current bond yield for the relevant maturity). This involves an estimation of the dividend yield, the real earnings growth, the expected inflation and the expected revaluation effect.

Unfortunately this gives us only limited information to go with, given the extraordinary current economic circumstances. However, we have effectively reformulated the original estimation of the equity the risk premium to a series of estimations of economic parameters. Just like estimating the equity risk premium, estimating these parameters also requires skill and in depth economic insight, but at least we can base them on observable market data or economic reasoning. In the next section we will estimate these parameters to build an estimate of the equity risk premium. We will aim for a long term estimation (10-15 years), which can be used in long term analyses of pension funds. Estimations for shorter term (say 1 year) are are not discussed in this paper, which is not to say that this is not an important task for a pension fund, since it can be used to assist in the annual asset allocation decision.

Unfortunately this gives us only limited information to go with, given the extraordinary current economic circumstances. However, we have effectively reformulated the original estimation of the equity the risk premium to a series of estimations of economic parameters. Just like estimating the equity risk premium, estimating these parameters also requires skill and in depth economic insight, but at least we can base them on observable market data or economic reasoning. In the next section we will estimate these parameters to build an estimate of the equity risk premium. We will aim for a long term estimation (10-15 years), which can be used in long term analyses of pension funds. Estimations for shorter term (say 1 year) are are not discussed in this paper, which is not to say that this is not an important task for a pension fund, since it can be used to assist in the annual asset allocation decision.

Revaluation effect

If we take the position that we have no view on future development of equity valuation and thereby assume that the current valuation is our best guess of future valuation, then we cannot ex ante expect a revaluation effect. So a neutral expectation is a revaluation effect of 0%.

Of course, if an investor has a view on valuation and the time period in which he expects some revaluation will occur within the considered time period, then the investor should incorporate this view in his expected equity risk premium.

Expected price inflation

Expected price inflation

There are two basic ways to estimate the CPI, either through surveys with market analysts, or through the financial markets.

The first method lead to a long term expected inflation of 2%. The latter method involves distilling the market expectations from the (break even) inflation from the market for inflation linked bonds and inflation swaps. Primo 2010 the break even inflation rate as distilled from euro inflation swap was 2.553 for a 15 years maturity. Assuming that the break even inflation rate incorporates a mark-up to the actual expected inflation, and assuming that this mark up is 20 base points (and note, this is an assumption) this leads to a ‘market based’ expected inflation of approximately 2.3%

Note that we haven’t mentioned historical data. With the introduction of the ECB, the CPI in the EURO region is controlled in a different way. ECB has an explicit task to keep the price inflation under or close to 2%.10 Since this is a trend breach, historical data cannot be used.

Which method leads to the best expectations can be debated. For a long term estimation, my best guess would be to follow the market surveys11 and align with ECB targets, and use 2% as an estimate of expected inflation. The estimation of the financial market expectation is clouded with supply and demand powers, and uncertainty on the mark-up.

Dividend yield

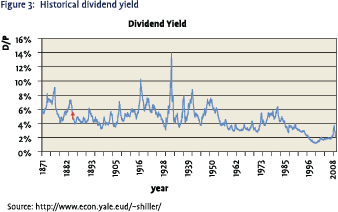

An estimation of the dividend yield depends on the investor’s view of the future. If we take the position that we do not have a view on the future, our best estimate is to consider the current, observed dividend yield as the most accurate representation of the future. Robert Shiller12 calculated the dividend yield per primo 2010, at 2.02%. However, one single market data point might be distorted by a disbalance of some kind on the financial markets. To see this, we plot monthly historical data in figure 3. We see that 2.02% is on the lower spectrum of historical results. 90% of the observations over the period 1871-2009 fall in the range 1.73%- 7.22%. For the more recent (yet arbitrary) period 1950-2009 this range is 1.38%-5.92%.

An estimation of the dividend yield depends on the investor’s view of the future. If we take the position that we do not have a view on the future, our best estimate is to consider the current, observed dividend yield as the most accurate representation of the future. Robert Shiller12 calculated the dividend yield per primo 2010, at 2.02%. However, one single market data point might be distorted by a disbalance of some kind on the financial markets. To see this, we plot monthly historical data in figure 3. We see that 2.02% is on the lower spectrum of historical results. 90% of the observations over the period 1871-2009 fall in the range 1.73%- 7.22%. For the more recent (yet arbitrary) period 1950-2009 this range is 1.38%-5.92%.

Real Earnings Growth

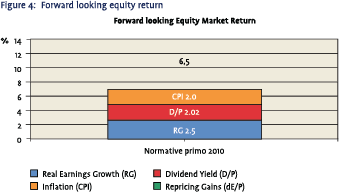

The real earnings growth shows little predictability,13 and can be debated the most heavily. My best estimate is relies on historical data. Ilmanen14 came up with an approach where he used a weighted average of the geometric average growth of the past 10, 20, 30, 40 and 50 years. This approach leads to a real earnings growth of approximately 2.5% Adding up, this leads to an expected equity return of 0% + 2% + 2.0%+2.5% is 6.5%. To get to the ERP, we need the long term (15 years) bond yield. Given that we have no specific view on future interest rate  developments we use the current (per primo 2010) 15 years bond yield as approximation. The yield on euro sovereign bonds per primo 2010 was 4.0%. This leaves us with an expected long term equity risk premium for worldwide mature market equity equal to 2.5%.

developments we use the current (per primo 2010) 15 years bond yield as approximation. The yield on euro sovereign bonds per primo 2010 was 4.0%. This leaves us with an expected long term equity risk premium for worldwide mature market equity equal to 2.5%.

The estimates for the three factors leads tot an aggregate estimate of the forward looking equity return of 6.5% as can be seen from figure 4. In this estimation process, we abstracted from regional and currency differences.

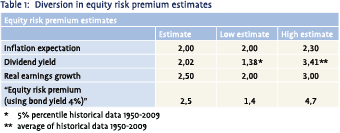

The argumentation above shows that estimating the ERP involves several choices and depends on the current economic environment. Using the same approach, with (slightly) different choice can lead to different outcomes as is shown in table 1.

How to deal with parameter uncertainty? Does it really matter?

How to deal with parameter uncertainty? Does it really matter?

Leaving the academic discussion behind us, let’s take a closer look at the meaning of the equity risk premium for a pension fund.

For many pension funds, the size of the equity risk premium is – combined with the expectations on other parts of the pension fund investments – used to determine the level of the cash contribution. This is done by setting a forward looking fixed contribution that is expected to be sufficient to attain the strategic goals, or this is done by mitigating the actuarial cost with the expected future returns. In both cases, the higher the risk premium, the lower the contribution can be set; the more the financing of the pensions depends on the future investment returns.

Furthermore, many pension funds are executing a recovery plan in order to improve the financial position. A higher expected equity return implies a more swift recovery and postpones the need for additional cash contribution from the sponsor or a discount of the pensions. A higher risk premium implies that the financing of the pension fund depends on future returns.

Many decisions – including these contribution decisions – are supported by traditional ALM studies. These studies help to gain insight in the reasonably expected range of outcomes for all stakeholders and are key in planning for the future and in risk management. These studies depend on the estimation of the equity risk premium. In using these studies, it is important to understand that the current expectation might be wrong in hindsight. The more the financial set-up depends on equity returns the higher the costs are of ex post deviations from the expected returns.15

To control the cost of faulty parameters and thereby constructing a solid and robust financial set up requires specific stress testing for a lower return (what if one of our estimates is wrong?) or an economic regime switch (e.g. deflation or stagflation). This way, the pension funds strategy can be determined taking into account what risks are bearable and which aren’t and at what costs these risks can or need to be hedged. In this way, the dependence on an undeniably uncertain parameter can be diminished and the policy can be made more robust.

Conclusion

It is important to make an accurate estimation of future expected returns. Using historical data leaves us with much uncertainty, Using a forward looking approach helps us with data issues and leaves us with a more objective debate, but in fairness we must agree that it does not help us much in giving us more certainty. In this view it is not surprising that the commission Don failed to form a unanimous view on the equity risk premium parameter. More important than the academic debate on the correct equity risk premium is the way the stakeholders of a pension fund decide on the financial set-up.

Given that we don’t know the future equity risk premium for certain, pension funds still need to make a decision under uncertainty. Given this uncertainty it is important to supplement the traditional decision support models with specific stress testing to provide insight in the costs and risks of faulty parameters. This will help decision makers make a solid and robust system.

Noten

- The author would like to thank Gaston Siegelaer and Jan Bertus Molenkamp for their comments on this article

- The parameters are established in “Regeling parameters pensioenfondsen”, dd December 19, 2006 nr. AV/PB/2006/ 102565b

- The commission made no statement regarding the discount rate. This topic was discussed in VBA journaal nr. 2, Summer 2009 by Tjitsger Hulshoff.

- Dimson, Marsh, Staunton. “101 years of investment returns”. London Business School and ABN Amro. 2006

- Dimson, Marsh, Staunton. “Keeping faith with stocks”. Credit Suisse Global Investment Returns Yearbook 2009. 2009

- Ilmanen. “Expected Returns on Stocks and Bonds”. The Journal of Porfolio Management. 2002 Robert Shiller. “Irrational Excuberance”. Princeton University Press. 2000

- Exact calculation is required to quantify this statement.

- Ibottson, Roger and Peng Chen. “Stock Market Returns in the Long Run: Participating in the Real Economy”. Working paper. Yale ICF/ 2002

- Gordon, Myron J. (1959). “Dividends, Earnings and Stock Prices”. Review of Economics and Statistics 41: 99–105.

- The main question here is whether we trust the capability of the ECB to control the inflation for the time period for which we estimate the inflation. Galati et al [Galati, Poelhekke, Zhou. 2009. “Did the Crisis Affect Inflation Expectations?”, DNB Working Paper No.222/2009. August 2009] show that market participants have increasingly diverged it’s estimations from the central bank target during the crisis. This can be due to a decline in confidence or supply and demand reasons. The study does not make a statement for the future. Surveys on inflation expectations with analysts and economist consistently show that the expectations average towards the ECB target.

- see ECB website

- See his website: http://www.econ.yale.edu/~shiller/

- See Ilmanen, 2002

- See Ilmanen, 2002

- Hoevenaars. (2008). “Strategic Asset Allocation & Asset Liability Management”. Thesis. University of Maastricht

in VBA Journaal door Tjitsger Hulshoff