In the past few years, executive compensation has been one of the most heated topics in the Dutch corporate world. The popular press in particular, has referred to the compensation of Dutch executive board members as ‘excessive’, and Dutch executives are being typified as greedy and solely focused on enriching themselves at the expense of the stakeholders of the company. The current discussion in the Netherlands is based on the recommendations made by the so-called ‘Commissie Tabaksblat’ (‘Corporate Governance code’) about executive remuneration1 . The levels of and increase in the base salaries and short-term bonus payments of Dutch board members has been the committee’s primary focus. So far the amount of scientific research conducted in the field of Dutch executive compensation, in particular the long-term incentive plans, (‘LTIPs’), has however, been limited, which is remarkable since LTIPs are increasingly forming part of Dutch executive compensation contracts. This article is based on a study on Dutch executive compensation, conducted by Hewitt Associates in collaboration with the Rijksuniversiteit Groningen2. It deals with the trends, the structure and the characteristics of the long-term incentive plans in major Dutch corporations. We will first give an outline of the theoretical concepts behind the use of equitybased incentive plans, and discuss the different types of plans. Then, we will present the preliminary findings of our research.

In the past few years, executive compensation has been one of the most heated topics in the Dutch corporate world. The popular press in particular, has referred to the compensation of Dutch executive board members as ‘excessive’, and Dutch executives are being typified as greedy and solely focused on enriching themselves at the expense of the stakeholders of the company. The current discussion in the Netherlands is based on the recommendations made by the so-called ‘Commissie Tabaksblat’ (‘Corporate Governance code’) about executive remuneration1 . The levels of and increase in the base salaries and short-term bonus payments of Dutch board members has been the committee’s primary focus. So far the amount of scientific research conducted in the field of Dutch executive compensation, in particular the long-term incentive plans, (‘LTIPs’), has however, been limited, which is remarkable since LTIPs are increasingly forming part of Dutch executive compensation contracts. This article is based on a study on Dutch executive compensation, conducted by Hewitt Associates in collaboration with the Rijksuniversiteit Groningen2. It deals with the trends, the structure and the characteristics of the long-term incentive plans in major Dutch corporations. We will first give an outline of the theoretical concepts behind the use of equitybased incentive plans, and discuss the different types of plans. Then, we will present the preliminary findings of our research.

Historical background

Executive stock option plans, for a long time the main component of the long-term incentive pay package, were introduced in the United States in the late seventies. The real explosion in option pay started, however, in the late eighties and begin nineties and was further fuelled by the nineties bull market (see Jensen et al (2004) for a detailed overview). In the late nineties stock options constituted the largest part of the US executive compensation package and also regularly formed part of the Dutch compensation package (however, to a smaller degree).

The popularity of stock options with executives can be explained by the fact that from the early eighties until the late nineties the bull market was constant, which led to frequent large option payouts. Since there was no accounting charge for stock options they were regarded by both executives and companies as practically free compensation. And since investor returns were large in this period, nobody really cared about the costs. However, with the collapse of the Internet bubble in the stock market and the corporate scandals in the US and the Ahold affair in the Netherlands, stock options were all of a sudden seen in a different light. They were partly held accountable for the fraud practices and the inflated stock prices, since executives had every interest to keep stock prices high at all costs to cash in on their options (the relation between corporate fraud and excessive option compensation has in fact been confirmed by several studies). Because the value of the executive’s stock option holdings massively decreased after the stock market crash, the popularity of stock options among executives also declined and new forms of long-term equity-based compensation were developed, with the performance share as prime example. In the US stock options retained their popularity, but in Europe, first in the UK and later also on the continent, performance shares slowly took over. We will look at the Dutch situation later on to discuss the latest trends.

The recommendations of the ‘Commissie Tabaksblat’ for executive compensation state that the principles should be clearly laid down in the annual report. Under the head ‘particulars to be added to the annual accounts and the annual report’, the annual accounts have to include the principal points of the remuneration report of the supervisory board concerning the company’s remuneration policy, as drawn up by the remuneration committee. The notes enclosed in the annual accounts have to contain complete and detailed information on the amount and structure of the remuneration of the individual members of the management board. The amount of compensation previously agreed upon concerning the termination of a management board member’s contract of employment should also be stated in the notes enclosed in the annual accounts. The principles of the management’s remuneration are based on several indicators. The amount and structure of the remuneration the management board members receive from the company for their work has to be such that qualified and expert managers can be recruited and retained. If the remuneration consists of a fixed and a variable part, the variable part should be linked to previously determined, measurable and controllable objectives, which have to be achieved, partly in the short term and partly in the long term, in order to strengthen the board members’ ties with the company. The remuneration structure should be such that it promotes the interests of the company in the medium and long term, and does not encourage board members to act in their own interests and neglect those of the company. The amount and structure of the remuneration should be based on the results, the company’s stock performance and internal developments. The shares held by board members in the company are long-term investments. The amount of compensation a board member may receive as a result of the termination of his employment may not exceed one year’s salary. Naturally, the company could adhere to the ‘explain or comply’ principle, if it wishes to apply different rules. The above-mentioned recommendations of the Dutch Corporate Governance code have set the scene for the current discussion in The Netherlands.

Theoretical background

So far, the academic literature on long-term incentives almost primarily focused on traditional stock option plans as the representative of equity-based plans. This is because in the United States these plans constitute the largest part of the long term incentive pay package.

The concept of long-term incentive plans is rooted in the agency theory, which is based on the separation of ownership and control and the conflicting interests between managers and shareholders (Jensen & Meckling, 1976). Managers have the incentive to expand their firms beyond the optimal size, because their compensation is naturally tied to firm size (sales growth), and their power and status increase by extending the resources under their control (Jensen, 1986; Murphy, 1985). Furthermore, since managers are naturally risk-averse they tend to invest in low-risk investments, whereas shareholders prefer high risk investments due to their diversified portfolios. By providing a direct link between realized compensation and company stock-price performance, equity-based compensation gives executives a greater incentive to act in the interests of the shareholders, although incentive effects differ depending on the kind of LTIP. In the next section we will discuss the various types of LTIPs and the (positive as well as negative) incentive effects associated with the specific plans.

Different types of long term incentive plans

In recent years, new types of long-term incentive plans have been developed alongside the traditional stock option plan. We characterize seven basic types of LTIPs, though note that definitions in the literature might differ from the ones we use:

- Stock option plans: the traditional and most frequently implemented long-term incentive plan in which stock options are awarded to executives. The vesting of these options can depend on the degree to which performance measures are met, or on the expiration of an initial vesting period.

- Restricted stock: grants of actual shares of stock that cannot be sold during an initial vesting period, which usually lasts two or three years.

- Performance shares: grants of actual shares of stock whose vesting depends on the degree to which certain performance standards are met during a performance period of usually three years. The typical Dutch performance share plan includes a performance period of three years over which the Total Shareholder Return relative to a peer group of competitors is measured. The final ranking after these years determines the payout, which can vary from 0% for lower quartile performance to 150-200% for top quartile performance, although payout schemes can differ significantly. In some cases the grant size rather than the vesting depends on performance measures and the stock granted thereafter qualifies as restricted stock. However, in this case we have classified these plans as performance share plans, since performance conditions are in some way tied to the shares.

- Performance units: the structure and characteristics of this plan resemble those of performance share plans; however, the payout is in the form of a combination of stock options, shares and, in some cases, cash. The payout is dependent on the performance of the underlying stock.

- Stock appreciation rights: these plans are similar to normal stock option plans; however the payout is in cash, and not in stock options.

- Deferred bonus / share investment plans: part of the yearly cash bonus is paid out in company shares and is retained (compulsory) for a specific period, usually three years, after which matching shares are awarded. In some cases the grant of matching shares depends on the degree to which performance measures are met.

- Phantom stock: commonly used in not-listed companies in which a share price performance movement is simulated and the payout depends on this performance.

Furthermore we define long-term cash bonus plans, which are not equity-based, but are focused on longterm company performance. This is usually a normal cash bonus plan with a (rolling) performance period of more than one year, usually three years. In most cases, payment is tied to accounting measures, like in short-term bonus plans.

Besides aligning the interests of management and shareholders these plans all have in common that they are designed to make the executive focus on both the long-term performance and the long-term financial health of the firm. Other general arguments that can be made in favour of equity-based compensation is that offering it in lieu of cash compensation allows companies to attract highly motivated and entrepreneurial employees, and obtain employment services without (directly) having to spend cash. In addition, equity-based compensation stimulates retention incentives because only employees who remain with the firm can benefit from them (Hall & Murphy, 2003).

A distinctive characteristic in favour of stock options is that they encourage executive risk taking, which can reduce problems of executive risk aversion as outlined above. However, Sanders (2001) shows that rather than reducing the problem, stock options seem to exacerbate it by allowing executives to pursue potentially large gains from acquisitions, even if such gains are not assured.

As regards executive stock options, there are several other concerns. First, there is the already mentioned “pump and dump” argument; the tendency of executives to inflate earnings in order to cash in on options. Second, payout is not so much dependent on performance relative to peers, but more on general market trends. Through his actions an executive only has a limited influence on the stock price, which makes stock option payouts (or forfeitures) largely dependent on general market fluctuations. Executives performing badly in a bull market can still make a great deal of money on their options. Furthermore, there is no real penalty for failure. The worst thing that could happen is that their options forfeit worthless.

Performance shares partly cover these limitations in the sense that they cannot forfeit and therefore do not stimulate the incentive to significantly raise the stock price before the end of the term. They can also make executive wealth more sensitive to price fluctuations on the downside. Of course the stock price remains sensitive to market trends, but by making the vesting dependent on relative performance, performance shares still lead to payment in a bear market, if the performance is relatively good (although one could question whether executives should be rewarded at all if they are not capable of increasing shareholder value). One should remember though, that rewarding an executive for relative stock price performance is, in fact, rewarding him/her for increased stock price volatility, which is not always in the interest of the stakeholders of the firm. In a bull market high volatility usually leads to high returns, placing one at a top spot in the payout scheme (vice versa in a bear market). This is in fact the same incentive an executive is offered when being granted a stock option.

Other arguments in favour of performance shares are that they stimulate the incentive to pursue an appropriate dividend policy (dividends reduce the stock price, thereby decreasing the value of stock options) and that the dilution of the shareholder’s equity is less severe.

However, evidence also suggests that executives value options only to a limited extent compared to the costs of granting them (e.g. Hall & Murphy (2002) and Meulbroeck (2000) value this at about 55% of the firm’s costs made by providing them). This suggests that, compared to normal cash compensation, equity based compensation is an expensive way of compensating executives. It would only make sense to grant options or shares to executives if the incentives could make up for this difference, of which there is still no clear evidence. Furthermore, Buck et al (2003) find that for the same cost, options bring about a much more favourable pay-performance relationship than performance shares do, which could be considered as a significant disadvantage of performance shares compared to traditional stock options.

Research findings & explanations

Our study covers the executive remuneration policies of 71 major Dutch companies, more specifically the companies, which are included in the AEX and AMX stock indices and the 25 largest listed companies (based on turnover) not included in one of these indices. It is based on the information available in the annual reports and other publicly available information concerning the remuneration policy of the companies.

Our study covers the executive remuneration policies of 71 major Dutch companies, more specifically the companies, which are included in the AEX and AMX stock indices and the 25 largest listed companies (based on turnover) not included in one of these indices. It is based on the information available in the annual reports and other publicly available information concerning the remuneration policy of the companies.

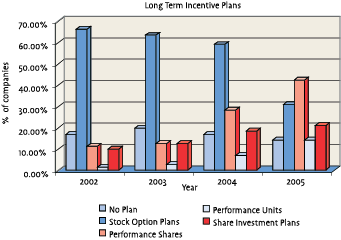

Our findings show some remarkable shifts in the types of plans used by companies. In 2002, the longterm incentive plans still largely consisted of traditional stock option plans. By 2004 the number of companies having implemented stock option plans had declined from more than 66% to 59%. How ever, the real decline took place in 2005 (based on the data available in the 2004 annual reports), namely to 31%. This decline was entirely due to the shift from stock option plans to performance share (and performance unit) plans. In 2002 only 13% of the companies offered a performance share or performance unit plan, where this number increased to 56% (shares: 42%, units: 14%) in 2005. Furthermore, in all cases newly implemented plans included performance shares.

Another remarkable trend is the rise in the use of deferred bonus / share investment plans (from almost 10% in 2002 to more than 20% in 2005). In addition, we see an increase in the use of so-called ‘shareholding obligations’ for executives. Here, the executive is obligated to use his/her own financial resources to invest in company stock. Core & Larcker (2001) find evidence that these latter plans have positive effects on incentives. However, granting 100% ‘matching shares’ on top of a deferred bonus for simply investing in company shares seems to be quite generous, and might qualify rather as a (restricted) stock grant.

In the light of pursuing adequate company governance, another trend can be observed in which the vesting (or grant) of options is increasingly tied to performance criteria, as recommended by the Dutch Corporate Governance code. This practice can be questioned somehow, however, since options as such already entail a performance standard (the exercise price). Against the background of good corporate governance policies, this policy is understandable though. One should take into account, however, that each performance condition lowers the value of the grant to the executive and takes away incentive effects.

What determines the size of the stock option grant? We see a mixed picture. 7% of the boards determine the grant value as a percentage of the base salary, whereas 27% grants a fixed number of options. This has important implications, since executives who receive a fixed grant are awarded for stock price increases with a higher grant value in the following year, whereas in case of a base salary percentage the executive is ‘punished’ for any occurring increase in share price (the value remains the same, but the new performance standard is being set high for the next term). On the other hand, granting a fixed number of options can increase the costs and compensation to unacceptable levels, while salary-based granting can ‘award’ executives for a bad performance by means of new options with low exercise prices. Further, in 15% of the companies the board awards the options discretionary, but in many cases (37%) it is not clear on what basis the grant is awarded. Another 22% bases the grant on firm performance (although a target grant has to be set independently).

In 40% of the companies the grant value of a performance share plan is based on a percentage of base salary (with the same limitations as described above). In 44% it is not clear what it is based on; in 16% the grant is based on firm performance and in some cases on the discretion of the board or on a competitive market analysis.

97% of the options is granted on the basis of a fixed exercise price at market value, hereby ignoring the benefits of indexed options (Rappaport, 1999), cost of capital options, adjusting the exercise price for paid dividends (Jensen et al, 2004) or granting at a discount (increased incentives, see Hall & Murphy, 2002). This can be explained by the Tabaksblat Code, which limits any adjustments based on a discount or on the decrease in value (and incentives), which executives encounter when options are being granted at a premium. The other 3% (slightly more in 2002 & 2003) is granted at a premium. By 2004, often mentioned concerns regarding stock options, such as reissuing (extending the exercise window), retesting (extending the performance period) and discounting the exercise price, were no longer really relevant.

The performance criterion for performance shares mostly used in 2004 was Relative Total Shareholder Return (TSR) (52%), followed by (absolute) earnings per share (16%). As regards upper quartile performance the target grant can on average be increased by 60%. When determining the vesting or grant of stock options, earnings per share is the most popular performance measure (37%), followed by TSR (33%). Other measures include the short-term incentive payment, sales growth, and some return measures. The popularity of earnings per share is somewhat surprising since it has been heavily criticized in academic papers. Because of its ratio-like character it is highly susceptible to executive ‘gaming’; both sides of the equation can be ‘influenced’ to create the desired outcome (see e.g. Jensen, 2001). We already expressed some concerns about the use of TSR. It should, however, be recognized that every performance measure has its limitations. The objective is to balance these limitations and to exert the necessary control.

The findings of our study can be explained as follows:

- An increased focus on good corporate governance. Options are considered a reflection of excessive compensation, whereas in the light of adequate company governance, performance shares (or performance measures tied to stock options) are viewed more positively. Moreover, corporate governance codes such as Tabaksblat seem to have a clear preference for performance shares and performance conditions tied to stock options.

- The awareness of the increase in costs of share option plans versus doubts about the effectiveness of these plans. This has partly been caused by the accounting charge that has to be recognised under IFRS. The economic costs of executive stock option plans might have turned out to be much higher than board members and investors had thought it to be, which explains the shift to the “cheaper” performance share plans. However, as mentioned before, evidence has shown that performance shares might not be a solution in the sense of a more cost effective pay-performance relationship.

- Shares offer a more stable and predictable income. They do not entail the downside risk inherent to stock options, especially when outside (economic) factors, which cannot be influenced by the executive, reduce the payout potential of the option and therefore the value to the executive.

- Due to dilution share awards have less impact on shareholder’s interests.

- There have been doubts on the incentive effects of stock options. Research has pointed out that large grants of stock options increase the chance of corporate fraud (e.g. the Enron affair) and since executives in general have low expectations regards their value, options might not stimulate incentives that would actually align the interests of shareholders and management.

- Westphal et al (2000) found evidence that stock option plans have a great symbolic value in the sense that they assume a more shareholder-oriented pay policy. We can also view the increase in performance share plans as a reflection of a more ‘adequate company governance’-oriented and socially acceptable pay policy.

- In this context we also observe the ‘confirmation to the standard’ trend. Long-term incentive plans (as well as STI plans) seem to resemble each other more and more. This might be the result of the general view that these plan variants are simply the best alternatives, but this might also be explained by a lack of time or knowledge of remuneration committee members to develop firm-specific alternatives, or by a dependency of the firm on one major remuneration consultant.

Should variable pay be offered anyway?

Based on social psychological empirical evidence, Frey & Osterloh (2005) argue that high-powered incentive compensation, even if it could be optimally designed, does not solve the problems in the corporate sector, such as the recent fraud scandals, but aggravate them. They show that there is a countervailing effect that causes a higher compensation to crowd out the intrinsic motivation for work, by shifting the executive’s interest from the activity itself to the reward. Furthermore, high-powered incentive compensation can also hinder crowding in or raising intrinsic motivation, for example because managers have the view that doing one’s duty without extra pay is socially inappropriate. Frey & Osterloh argue that a normal salary should be sufficient, since individuals find satisfaction in the activity itself, and their motives for adhering to given normative standards may not solely be based on financial goals. This raises the question whether the whole discussion about performance levels and the pressure to compete with competitive, market-based salaries is not merely a self-fulfilling prophecy. After all, convincing evidence that a high-powered incentive structure leads to more incentives (in the sense of higher firm performance) has still not been found (see e.g. Tosi et al, 2000, or Dalton et al, 2003). Jensen & Murphy (2004) argue, however, that the ill-suited design of the current compensation contracts and the ineffective corporate governance system prevent the executive compensation from working effectively.

Conclusion

We see that the structure and characteristics of Dutch executive pay contracts are evolving quickly. New forms of compensation are being implemented, by using instruments that have both advantages and disadvantages. Performance shares seem to have considerable advantages compared to stock options, however a shift toward performance shares may in the end be an expensive one (Buck et al, 2003). In any case, the perfect compensation contract does not exist. Contracts should be tailored to firm specific circumstances to provide optimal incentives against limited costs. In the years to come we can expect a continuing focus on long-term incentive plans as a result of new tax and accounting rules and the continuing debate on good corporate governance and socially acceptable compensation. Furthermore, it is to be expected that LTIPs will play an increasing role in the Dutch executive’s compensation package. It is therefore important to be aware of the advantages and limitations of the various forms and to explain the choices made in this context on the basis of the plans’ characteristics.

References

- Buck, T.L., Bruce, A., Main, B.G.M. & H. Udueni, Long term incentive plans, executive pay and UK company performance, Journal of Management Studies, 2003.

- Core, J.E. & D.F. Larcker, Performance consequences of mandatory increases in executive stock ownership, Journal of Financial Economics, 2001.

- Dalton, D.R., Trevis Certo, S. & R. Roengpitya, Meta-analysis of financial performance and equity: fusion or confusion, Academy of Management Journal, 2003.

- Frey, B.S. & M. Osterloh, Yes, managers should be paid like bureaucrats, Journal of Management Inquiry, 2005.

- Hall, B.J. & K.J. Murphy, Stock options for undiversified executives, Journal of Accounting and Economics, 2002.

- Hall, B.J. & K.J. Murphy, The trouble with stock options, Journal of Economic Perspective, 2003.

- Jensen, M.C. & W.H. Meckling, Theory of the firm: managerial behavior, agency costs and ownership structure, Journal of Financial Economics, 1976.

- Jensen, M.C., Agency costs of free cash flow, corporate finance and takeovers, The American Economic Review, 1986.

- Jensen, M.C., Corporate budgeting is broken – Let’s fix it, Harvard Business Review, 2001.

- Jensen, M.C., Murphy, K.J., & E.G. Wruck, Remuneration: where we’ve been, how we got to here, what are the problems, and how to fix them, Harvard Business School NOM Research Paper, 2004.

- Meulbroek, L.K., The efficiency of equity-linked compensation: understanding the full cost of awarding executive stock options, Harvard Business School Working Paper, 2000.

- Murphy, K.J., Corporate performance and managerial remuneration: an empirical analysis, Journal of Accounting and Economics, 1985.

- Rappaport, A., New thinking on how to link executive pay with performance, Harvard Business Review, 1999.

- Sanders, G., Behavioural responses of CEOs to stock ownership and stock option pay, Academy of Management Journal, 2001.

- Tosi, H.L., Werner, S., Katz, J.P. & L.R. Gomez-Meija, How much does performance matter? A meta-analysis of CEO pay studies, Journal of Management, 2000.

- Westphal, J.D. & E.J. Zajac, Substance and symbolism in CEOs’ long-term incentive plans, Administrative Science Quarterly, 1994.

Notes

- Zie http://www.commissiecorporategovernance.nl/page/ downloads/CODE%20DEF%20COMPLEETII.pdf

- Zie http://www.rug.nl/bdk/onderwijs/ postacademischonderwijs/PDCO/index

in VBA Journaal door Erik Terpstra (r), Dirk Swagerman (l)